Theory

This section develops the theoretical foundations of panel data econometrics, focusing on the fixed effects estimator and its properties.

The Panel Data Model

Setup

We observe \(N\) units (countries) over \(T\) time periods (quarters). The data generating process (DGP) is:

\[

y_{it} = \mathbf{x}_{it}'\boldsymbol{\beta} + \alpha_i + \varepsilon_{it}, \quad i = 1, \ldots, N, \quad t = 1, \ldots, T

\]

where:

- \(y_{it}\): outcome (e.g., policy rate for country \(i\) at time \(t\))

- \(\mathbf{x}_{it}\): \(K \times 1\) vector of observable regressors (e.g., bank holdings, inflation)

- \(\boldsymbol{\beta}\): \(K \times 1\) parameter vector of interest

- \(\alpha_i\): unobserved time-invariant individual effect (institutions, geography, political culture)

- \(\varepsilon_{it}\): idiosyncratic error

The key question: what happens to \(\hat{\boldsymbol{\beta}}\) when we ignore \(\alpha_i\)?

Pooled OLS: The Naive Approach

If we ignore the panel structure and estimate by OLS:

\[

y_{it} = \mathbf{x}_{it}'\boldsymbol{\beta} + u_{it}, \quad \text{where } u_{it} = \alpha_i + \varepsilon_{it}

\]

The OLS estimator is:

\[

\hat{\boldsymbol{\beta}}_{\text{OLS}} = \left(\sum_{i=1}^{N}\sum_{t=1}^{T} \mathbf{x}_{it}\mathbf{x}_{it}'\right)^{-1} \left(\sum_{i=1}^{N}\sum_{t=1}^{T} \mathbf{x}_{it} y_{it}\right)

\]

Consistency requires \(\text{plim} \left(\frac{1}{NT}\sum_{i,t} \mathbf{x}_{it} u_{it}\right) = \mathbf{0}\).

Expanding: \[

\frac{1}{NT}\sum_{i,t} \mathbf{x}_{it} u_{it} = \frac{1}{NT}\sum_{i,t} \mathbf{x}_{it} \alpha_i + \frac{1}{NT}\sum_{i,t} \mathbf{x}_{it} \varepsilon_{it}

\]

The second term vanishes under standard exogeneity (\(E[\varepsilon_{it}|\mathbf{x}_{it}] = 0\)). But the first term:

\[

\frac{1}{NT}\sum_{i,t} \mathbf{x}_{it} \alpha_i \xrightarrow{p} E[\mathbf{x}_{it} \alpha_i] = \text{Cov}(\mathbf{x}_{it}, \alpha_i) + E[\mathbf{x}_{it}]E[\alpha_i]

\]

If \(\text{Cov}(\mathbf{x}_{it}, \alpha_i) \neq 0\), pooled OLS is inconsistent.

In macroeconomic panels, countries with high bank holdings of sovereign debt (\(\mathbf{x}\)) likely have different institutional quality (\(\alpha\)) than countries with low holdings. A banking system may hold lots of government bonds because of institutional features (regulatory requirements, underdeveloped capital markets) that also independently affect monetary policy. Pooled OLS conflates the causal effect of bank holdings with these institutional differences.

The Fixed Effects Estimator

What FE Uses and What It Discards

FE uses only within-unit variation: deviations of \(x_{it}\) from its country mean \(\bar{x}_i\).

- If a country always has bank holdings of 30%, it contributes zero identifying variation to \(\hat{\beta}_{\text{FE}}\)

- The identifying variation comes from changes in bank holdings within a country over time

- A country that goes from 20% to 35% holdings contributes a lot; a country stuck at 25% contributes little

FE discards between-unit variation: differences in average \(\bar{x}_i\) across countries.

This is both the strength (eliminates \(\alpha_i\) bias) and the weakness (throws away cross-sectional information, reduces efficiency).

Consistency

\(\hat{\boldsymbol{\beta}}_{\text{FE}}\) is consistent under:

Assumption (Strict Exogeneity): \[

E[\varepsilon_{it} | \mathbf{x}_{i1}, \ldots, \mathbf{x}_{iT}, \alpha_i] = 0 \quad \forall \, t

\]

This means:

- Current errors are uncorrelated with past, present, AND future regressors

- This rules out feedback effects: if past \(y\) affects current \(x\), strict exogeneity fails

- This also rules out lagged dependent variables as regressors (Nickell bias)

The Frisch-Waugh-Lovell Theorem

The FE estimator is numerically identical to OLS with \(N\) country dummies.

Theorem (Frisch-Waugh-Lovell): In the regression \(y = X_1\beta_1 + X_2\beta_2 + \varepsilon\), the OLS estimate of \(\beta_1\) is identical to the OLS estimate from regressing \(M_2 y\) on \(M_2 X_1\), where \(M_2 = I - X_2(X_2'X_2)^{-1}X_2'\) is the annihilator matrix for \(X_2\).

Application to FE: Let \(X_1 = \mathbf{X}\) (regressors of interest) and \(X_2 = D\) (matrix of country dummies). Then:

- \(M_D \mathbf{x}_{it} = \mathbf{x}_{it} - \bar{\mathbf{x}}_i = \ddot{\mathbf{x}}_{it}\) (the within transformation!)

- \(M_D y_{it} = y_{it} - \bar{y}_i = \ddot{y}_{it}\)

So FE = OLS with dummies = OLS on demeaned data. These are algebraically identical.

Practical implication: fixest::feols() uses the within transformation (fast), while lm() with dummy variables estimates all \(N\) dummy coefficients (slow, memory-intensive). Same \(\hat{\beta}\), different computational cost.

Two-Way Fixed Effects

The Model

\[

y_{it} = \mathbf{x}_{it}'\boldsymbol{\beta} + \alpha_i + \lambda_t + \varepsilon_{it}

\]

Now \(\lambda_t\) absorbs time-varying shocks common to all units:

- \(\alpha_i\): Country A is different from Country B in time-invariant ways

- \(\lambda_t\): 2022Q2 was different from 2019Q2 for all countries (global inflation surge, Fed tightening)

Double Demeaning

The two-way within transformation removes both \(\alpha_i\) and \(\lambda_t\):

\[

\tilde{y}_{it} = y_{it} - \bar{y}_{i\cdot} - \bar{y}_{\cdot t} + \bar{y}_{\cdot\cdot}

\]

What’s left: \(\tilde{y}_{it}\) is the part of \(y_{it}\) that can’t be explained by country-level or time-level averages. It’s the country-specific deviation from the global trend.

What Each Fixed Effect Absorbs

| Country FE (\(\alpha_i\)) |

All time-invariant country differences |

Regulatory frameworks, reserve currency status |

| Time FE (\(\lambda_t\)) |

All country-invariant time shocks |

Global inflation surge, commodity price spikes |

| Neither |

Country-specific, time-varying variation |

Country A’s holdings rose more in 2020 than average |

Interactions in Panel Models

The Interaction Term

Consider a specification with an interaction:

\[

y_{it} = \gamma_1 x_{it} + \gamma_2 z_{it} + \gamma_3 (x_{it} \times z_{it}) + \alpha_i + \lambda_t + \varepsilon_{it}

\]

What does \(\gamma_3\) mean?

The marginal effect of \(x\) on \(y\) is:

\[

\frac{\partial y_{it}}{\partial x_{it}} = \gamma_1 + \gamma_3 \cdot z_{it}

\]

This is not constant—it depends on the level of \(z_{it}\).

If \(\gamma_1 > 0\) and \(\gamma_3 < 0\), there exists a “crossing point” \(z^* = -\gamma_1/\gamma_3\) where the marginal effect of \(x\) switches sign. Below \(z^*\), \(x\) has a positive effect; above \(z^*\), negative.

Clustering Standard Errors

Standard OLS assumes \(\varepsilon_{it}\) is i.i.d. This fails in panels because:

- Serial correlation within country: A country’s error in 2022Q1 is correlated with its error in 2022Q2

- Cross-sectional dependence: Country A’s error in 2022Q1 may correlate with Country B’s (global shocks)

Clustering by country handles (1): it allows arbitrary within-country correlation over time.

Important: Cluster-robust inference requires \(N \to \infty\). With only 30 countries, cluster SEs may be unreliable. Rule of thumb: need \(N \geq 50\) for good coverage. With small \(N\), consider wild cluster bootstrap.

Monte Carlo Simulations

This section uses Monte Carlo simulations to demonstrate the properties of panel estimators.

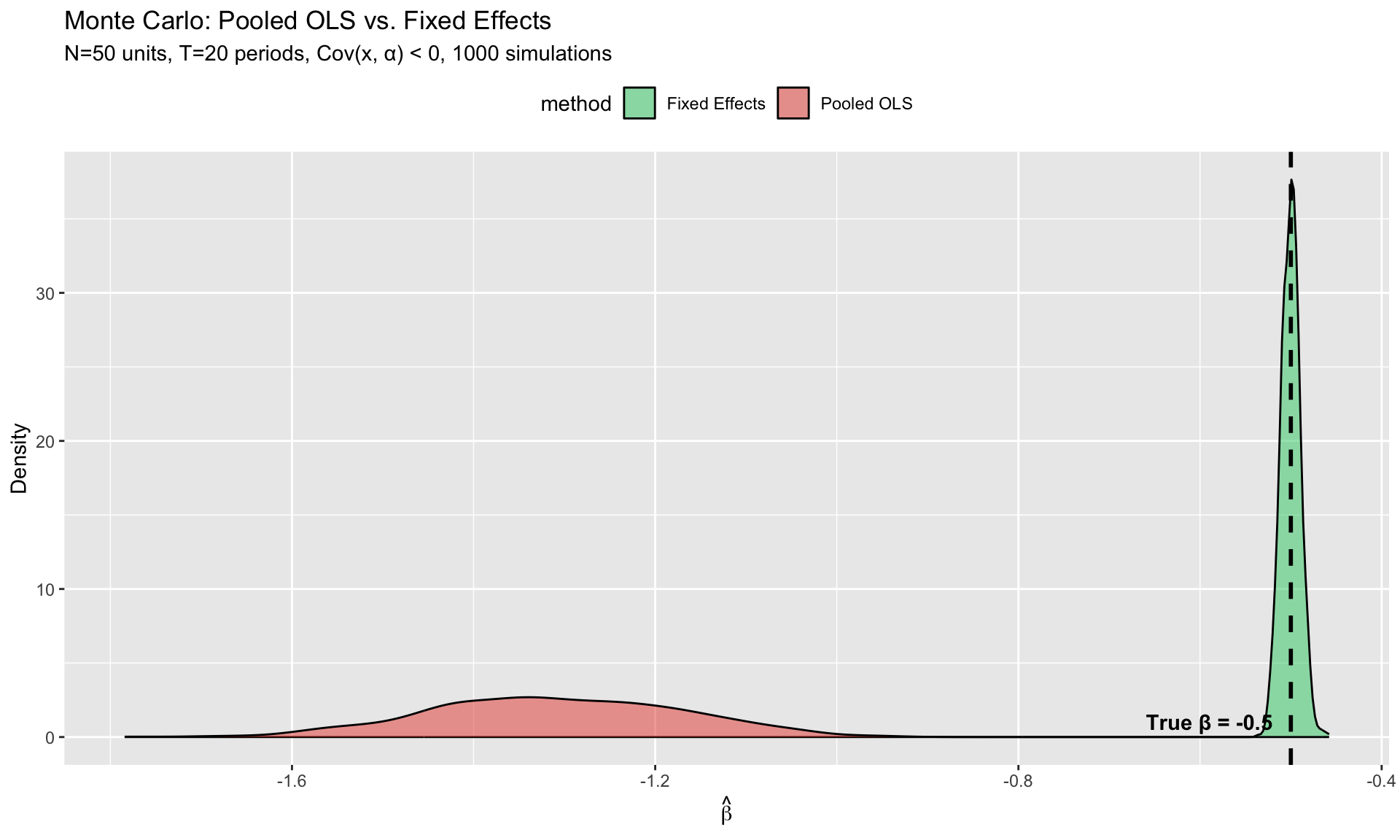

Demonstrating OVB: Pooled OLS vs. FE

We simulate a panel where \(\text{Cov}(x_{it}, \alpha_i) \neq 0\) and show that pooled OLS is biased while FE is consistent.

set.seed(42)

# Parameters

N <- 50 # countries

T_per <- 20 # quarters

beta_true <- -0.5 # true effect: negative

gamma_alpha <- 3 # how much alpha matters for y

# Simulation

n_sims <- 1000

beta_ols <- numeric(n_sims)

beta_fe <- numeric(n_sims)

for (s in 1:n_sims) {

# Generate unobserved heterogeneity

alpha <- rnorm(N, mean = 5, sd = 2) # country effect

# Generate x correlated with alpha

# Countries with higher alpha have LOWER x (negative correlation)

x <- matrix(NA, N, T_per)

for (i in 1:N) {

x[i, ] <- -0.8 * alpha[i] + rnorm(T_per, mean = 20, sd = 3)

}

# Generate y

y <- matrix(NA, N, T_per)

eps <- matrix(rnorm(N * T_per, sd = 1), N, T_per)

for (i in 1:N) {

y[i, ] <- beta_true * x[i, ] + gamma_alpha * alpha[i] + eps[i, ]

}

# Reshape to panel

id <- rep(1:N, each = T_per)

tt <- rep(1:T_per, times = N)

yy <- as.vector(t(y))

xx <- as.vector(t(x))

# Pooled OLS

beta_ols[s] <- coef(lm(yy ~ xx))[2]

# Fixed Effects

df <- data.frame(y = yy, x = xx, id = factor(id))

beta_fe[s] <- coef(fixest::feols(y ~ x | id, data = df))["x"]

}

# Results

cat("=== Monte Carlo Results (1000 simulations) ===\n")

=== Monte Carlo Results (1000 simulations) ===

cat(sprintf("True beta: %.3f\n", beta_true))

cat(sprintf("Pooled OLS mean: %.3f (bias = %.3f)\n", mean(beta_ols), mean(beta_ols) - beta_true))

Pooled OLS mean: -1.310 (bias = -0.810)

cat(sprintf("FE mean: %.3f (bias = %.3f)\n", mean(beta_fe), mean(beta_fe) - beta_true))

FE mean: -0.500 (bias = -0.000)

df_mc <- data.frame(

estimate = c(beta_ols, beta_fe),

method = rep(c("Pooled OLS", "Fixed Effects"), each = n_sims)

)

ggplot(df_mc, aes(x = estimate, fill = method)) +

geom_density(alpha = 0.5) +

geom_vline(xintercept = beta_true, linetype = "dashed", linewidth = 1) +

annotate("text", x = beta_true - 0.02, y = 0, label = paste("True β =", beta_true),

hjust = 1, vjust = -0.5, fontface = "bold") +

labs(

title = "Monte Carlo: Pooled OLS vs. Fixed Effects",

subtitle = "N=50 units, T=20 periods, Cov(x, α) < 0, 1000 simulations",

x = expression(hat(beta)),

y = "Density"

) +

scale_fill_manual(values = c("Pooled OLS" = "#e74c3c", "Fixed Effects" = "#2ecc71")) +

theme(legend.position = "top")

What you should see: The OLS distribution is centered well above the true value (biased positive). The FE distribution is centered on the truth.

Demonstrating Time FE Importance

set.seed(123)

N <- 40

T_per <- 20

beta_true <- -0.3

n_sims <- 500

beta_country_fe <- numeric(n_sims)

beta_twoway_fe <- numeric(n_sims)

for (s in 1:n_sims) {

alpha <- rnorm(N, sd = 3) # country effects

lambda <- rnorm(T_per, sd = 2) # time effects

# x correlated with both alpha AND lambda

x <- matrix(NA, N, T_per)

for (i in 1:N) {

for (t in 1:T_per) {

x[i, t] <- -0.5 * alpha[i] + 0.4 * lambda[t] + rnorm(1, mean = 20, sd = 2)

}

}

y <- matrix(NA, N, T_per)

for (i in 1:N) {

for (t in 1:T_per) {

y[i, t] <- beta_true * x[i, t] + alpha[i] + lambda[t] + rnorm(1, sd = 1)

}

}

id <- rep(1:N, each = T_per)

tt <- rep(1:T_per, times = N)

df <- data.frame(y = as.vector(t(y)), x = as.vector(t(x)),

id = factor(id), time = factor(tt))

beta_country_fe[s] <- coef(feols(y ~ x | id, data = df))["x"]

beta_twoway_fe[s] <- coef(feols(y ~ x | id + time, data = df))["x"]

}

cat("=== Time FE Matters When x Correlates with Time Shocks ===\n")

=== Time FE Matters When x Correlates with Time Shocks ===

cat(sprintf("True beta: %.3f\n", beta_true))

cat(sprintf("Country FE only: %.3f (bias = %.3f)\n",

mean(beta_country_fe), mean(beta_country_fe) - beta_true))

Country FE only: 0.045 (bias = 0.345)

cat(sprintf("Two-way FE: %.3f (bias = %.3f)\n",

mean(beta_twoway_fe), mean(beta_twoway_fe) - beta_true))

Two-way FE: -0.300 (bias = -0.000)

Key lesson: Country FE alone is not enough if the regressors correlate with common time shocks.

Cluster SE Coverage

set.seed(99)

N <- 30 # small number of clusters

T_per <- 12

beta_true <- -0.5

n_sims <- 1000

cover_iid <- 0

cover_cluster <- 0

for (s in 1:n_sims) {

alpha <- rnorm(N, sd = 3)

# Generate x and y with serially correlated errors

x <- matrix(NA, N, T_per)

y <- matrix(NA, N, T_per)

for (i in 1:N) {

x[i, ] <- -0.5 * alpha[i] + rnorm(T_per, 20, 3)

eps <- arima.sim(list(ar = 0.6), n = T_per, sd = 1) # AR(1) errors

y[i, ] <- beta_true * x[i, ] + alpha[i] + eps

}

df <- data.frame(y = as.vector(t(y)), x = as.vector(t(x)),

id = factor(rep(1:N, each = T_per)))

fit <- feols(y ~ x | id, data = df)

# IID standard errors

ci_iid <- confint(fit, se = "iid")

cover_iid <- cover_iid + (ci_iid[1] <= beta_true & beta_true <= ci_iid[2])

# Cluster standard errors

ci_cluster <- confint(fit, cluster = ~id)

cover_cluster <- cover_cluster + (ci_cluster[1] <= beta_true & beta_true <= ci_cluster[2])

}

cat("=== 95% CI Coverage (AR(1) errors within clusters) ===\n")

=== 95% CI Coverage (AR(1) errors within clusters) ===

cat(sprintf("IID SEs: %.1f%% (should be 95%%)\n", 100 * cover_iid / n_sims))

IID SEs: 95.7% (should be 95%)

cat(sprintf("Cluster SEs: %.1f%% (should be 95%%)\n", 100 * cover_cluster / n_sims))

Cluster SEs: 95.4% (should be 95%)

What you should see: IID standard errors have coverage well below 95% (too many false positives). Cluster SEs restore correct coverage.

Application

This section applies the methods to macroeconomic panel data.

Data Preparation

# Prepare the analysis sample

analysis <- master %>%

mutate(quarter = as.integer(gsub(".*Q", "", year_quarter))) %>%

group_by(country) %>%

arrange(year, quarter) %>%

mutate(

# Lagged variables

L1_bank_holdings_pct = lag(bank_holdings_pct),

L1_cb_holdings_pct = lag(cb_holdings_pct)

) %>%

ungroup() %>%

filter(!is.na(policy_rate), !is.na(bank_holdings_pct))

# Post-2022 subsample

tightening <- analysis %>%

filter(year >= 2022) %>%

filter(!is.na(L1_bank_holdings_pct))

cat("Full sample:", nrow(analysis), "obs,", n_distinct(analysis$country), "countries\n")

Full sample: 3406 obs, 41 countries

cat("Post-2022 sample:", nrow(tightening), "obs,", n_distinct(tightening$country), "countries\n")

Post-2022 sample: 480 obs, 40 countries

Building Up: OLS → FE → TWFE

# Check if we have the necessary variables

if ("inflation_yoy" %in% names(tightening) || "sovereign_debt_gdp" %in% names(tightening)) {

# Step 1: Pooled OLS

m1 <- feols(policy_rate ~ L1_bank_holdings_pct + sovereign_debt_gdp,

data = tightening)

# Step 2: Country FE only

m2 <- feols(policy_rate ~ L1_bank_holdings_pct | country,

data = tightening)

# Step 3: Two-way FE

m3 <- feols(policy_rate ~ L1_bank_holdings_pct | country + year_quarter,

data = tightening)

# Step 4: Add CB holdings

m4 <- feols(policy_rate ~ L1_bank_holdings_pct + L1_cb_holdings_pct

| country + year_quarter,

data = tightening)

# Step 5: Interaction

m5 <- feols(policy_rate ~ L1_bank_holdings_pct * L1_cb_holdings_pct

| country + year_quarter,

data = tightening)

# Display with appropriate SEs

# Note: In practice, FE models should use clustered SEs

etable(m1, m2, m3, m4, m5,

headers = c("Pooled", "Country FE", "TWFE", "+CB", "Interaction"),

vcov = list("iid", ~country, ~country, ~country, ~country),

fitstat = ~ n + r2 + wr2)

} else {

cat("Note: Full specification requires inflation and debt variables.\n")

cat("Running simplified demonstration with available variables.\n")

m1 <- feols(policy_rate ~ L1_bank_holdings_pct, data = tightening)

m2 <- feols(policy_rate ~ L1_bank_holdings_pct | country, data = tightening)

m3 <- feols(policy_rate ~ L1_bank_holdings_pct | country + year_quarter, data = tightening)

etable(m1, m2, m3,

headers = c("Pooled", "Country FE", "TWFE"),

vcov = list("iid", ~country, ~country),

fitstat = ~ n + r2 + wr2)

}

m1 m2

Pooled Country FE

Dependent Var.: policy_rate policy_rate

Constant 7.886*** (1.510)

L1_bank_holdings_pct 0.0687. (0.0369) 0.3734 (0.6231)

sovereign_debt_gdp -0.0402** (0.0146)

L1_cb_holdings_pct

L1_bank_holdings_pct x L1_cb_holdings_pct

Fixed-Effects: ------------------ ---------------

country No Yes

year_quarter No No

________________________________________ __________________ _______________

S.E. type IID by: country

Observations 480 480

R2 0.02667 0.81188

Within R2 -- 0.00812

m3 m4

TWFE +CB

Dependent Var.: policy_rate policy_rate

Constant

L1_bank_holdings_pct 0.5777 (0.6425) 0.6562 (0.6863)

sovereign_debt_gdp

L1_cb_holdings_pct 0.5837 (0.6104)

L1_bank_holdings_pct x L1_cb_holdings_pct

Fixed-Effects: --------------- ---------------

country Yes Yes

year_quarter Yes Yes

________________________________________ _______________ _______________

S.E. type by: country by: country

Observations 480 480

R2 0.83693 0.84322

Within R2 0.02141 0.05916

m5

Interaction

Dependent Var.: policy_rate

Constant

L1_bank_holdings_pct 0.4222 (0.3321)

sovereign_debt_gdp

L1_cb_holdings_pct 0.2438 (0.4371)

L1_bank_holdings_pct x L1_cb_holdings_pct 0.0201 (0.0386)

Fixed-Effects: ---------------

country Yes

year_quarter Yes

________________________________________ _______________

S.E. type by: country

Observations 480

R2 0.84451

Within R2 0.06693

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Within-Country Variation

within_var <- tightening %>%

group_by(country) %>%

summarise(

mean_holdings = mean(L1_bank_holdings_pct, na.rm = TRUE),

sd_within = sd(L1_bank_holdings_pct, na.rm = TRUE),

range_within = max(L1_bank_holdings_pct, na.rm = TRUE) -

min(L1_bank_holdings_pct, na.rm = TRUE),

n_obs = n()

) %>%

arrange(desc(sd_within))

cat("=== Within-Country Variation ===\n")

=== Within-Country Variation ===

print(head(within_var, 5))

# A tibble: 5 × 5

country mean_holdings sd_within range_within n_obs

<chr> <dbl> <dbl> <dbl> <int>

1 Argentina 20.7 2.94 8.95 12

2 Turkey 56.8 2.65 9.22 12

3 Denmark 6.33 2.37 7.61 12

4 Sweden 35.7 2.26 9.05 12

5 Hungary 25.3 2.22 6.39 12

# Variance decomposition

between_var <- var(within_var$mean_holdings, na.rm = TRUE)

avg_within_var <- mean(within_var$sd_within^2, na.rm = TRUE)

total_var <- var(tightening$L1_bank_holdings_pct, na.rm = TRUE)

cat(sprintf("\n=== Variance Decomposition ===\n"))

=== Variance Decomposition ===

cat(sprintf("Between variance: %.0f%%\n", 100 * between_var / total_var))

cat(sprintf("Within variance: %.0f%%\n", 100 * avg_within_var / total_var))

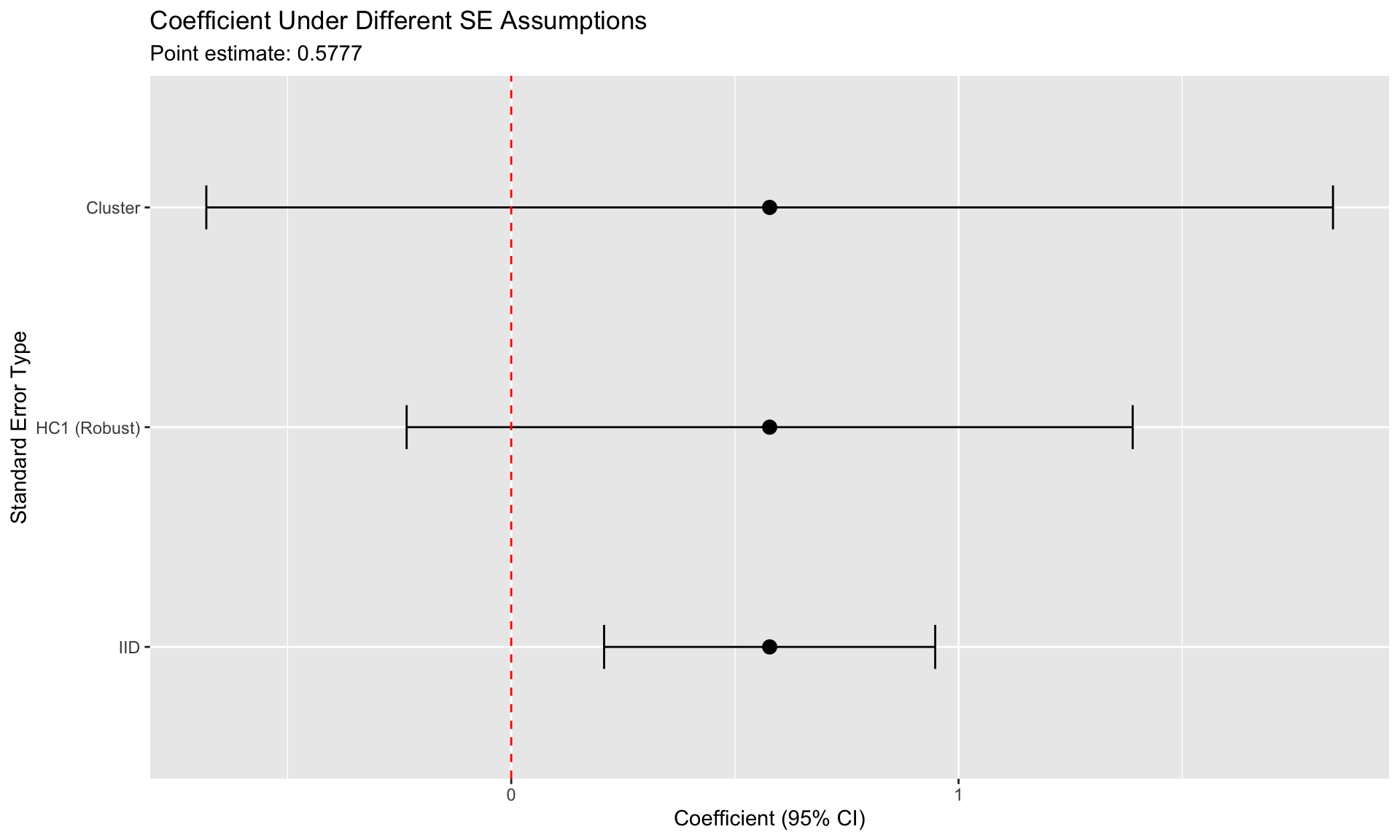

Standard Error Comparison

m_main <- feols(policy_rate ~ L1_bank_holdings_pct | country + year_quarter,

data = tightening)

coef_name <- "L1_bank_holdings_pct"

coef_val <- coef(m_main)[coef_name]

se_types <- c("IID", "HC1 (Robust)", "Cluster")

se_vals <- c(

sqrt(vcov(m_main, se = "iid")[coef_name, coef_name]),

sqrt(vcov(m_main, se = "hetero")[coef_name, coef_name]),

sqrt(vcov(m_main, cluster = ~country)[coef_name, coef_name])

)

se_df <- data.frame(

type = factor(se_types, levels = se_types),

se = se_vals,

lower = coef_val - 1.96 * se_vals,

upper = coef_val + 1.96 * se_vals

)

ggplot(se_df, aes(x = type, y = coef_val)) +

geom_point(size = 3) +

geom_errorbar(aes(ymin = lower, ymax = upper), width = 0.2) +

geom_hline(yintercept = 0, linetype = "dashed", color = "red") +

labs(

title = "Coefficient Under Different SE Assumptions",

subtitle = paste("Point estimate:", round(coef_val, 4)),

x = "Standard Error Type",

y = "Coefficient (95% CI)"

) +

coord_flip()

Frequently Asked Questions

Common conceptual questions when working with panel fixed effects.

Why not random effects?

The Hausman test typically rejects RE in favor of FE in macro panels. More importantly, RE assumes \(\text{Cov}(\mathbf{x}_{it}, \alpha_i) = 0\), which is often implausible: units with high values of the regressor may differ systematically from units with low values in ways that affect the outcome. FE is the safer choice when this correlation is likely.

What if within R² is low?

Within \(R^2\) in two-way FE models is supposed to be low. The overall \(R^2\) is often 70%+, with most explained by fixed effects. Within \(R^2\) measures how much of the remaining variation our regressors explain. In macro panels, a within \(R^2\) of 3-8% is normal. Statistical significance of coefficients is what matters for testing hypotheses.

What about endogeneity?

Fixed effects address endogeneity from time-invariant confounders. For time-varying endogeneity, consider:

- Instrumental variables (Module 2)

- Placebo tests in pre-treatment periods

- Timing variation within treated groups

- Lagged regressors (with caution about Nickell bias)

Summary

Key takeaways from this module:

Pooled OLS is biased when unobserved heterogeneity correlates with regressors

FE uses only within-unit variation — conservative but credible

Two-way FE absorbs global shocks — your coefficient captures country-specific deviations from global trends

Interactions reveal mechanisms — the effect of one variable may depend on another

Cluster your standard errors — IID SEs are too small due to within-country correlation

Low within R² is expected — the question is whether the mechanism is detectable, not whether it explains all variation

Next: Module 2: Identification in Macroeconomics