Bayesian Panel Methods

Hierarchical Models, Panel VARs, and Cross-Sectional Dependence

The Panel Data Challenge

Cross-country macroeconomic panels present a fundamental tension:

Heterogeneity: Countries differ in institutions, structures, and responses Limited Data: Each country has finite time series (T = 84 quarters) Efficiency: Ignoring cross-country information wastes data

NoteThe Core Question

How do we pool information across countries while respecting heterogeneity?

Three Approaches

| Approach | Assumption | Problem |

|---|---|---|

| Pooled | All countries identical | Ignores heterogeneity |

| Country-by-country | Countries unrelated | Inefficient, noisy |

| Hierarchical Bayes | Countries related but different | Best of both worlds |

With N = 46 countries and T = 84 quarters, hierarchical Bayesian methods offer the natural solution.

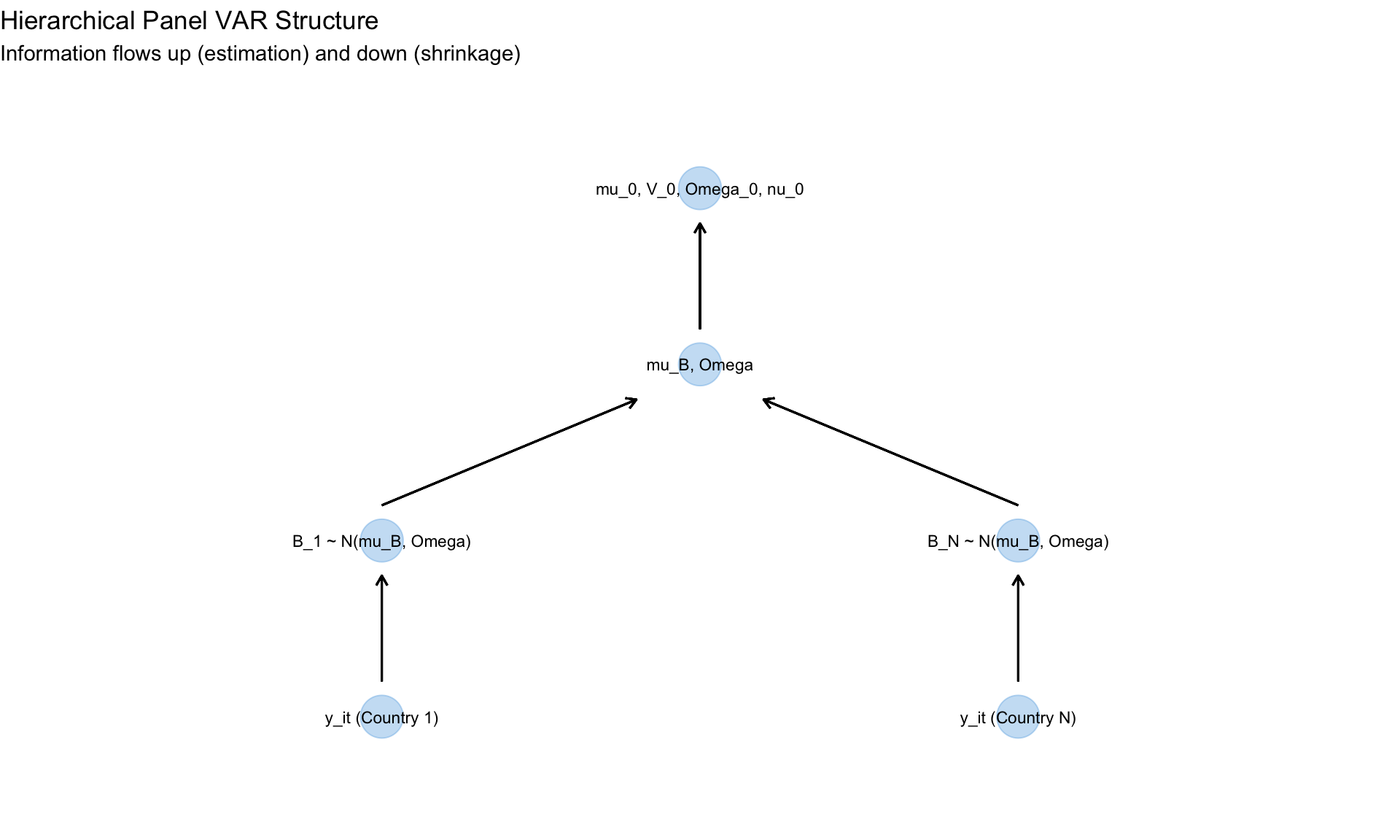

Hierarchical Models: The Framework

The Multilevel Structure

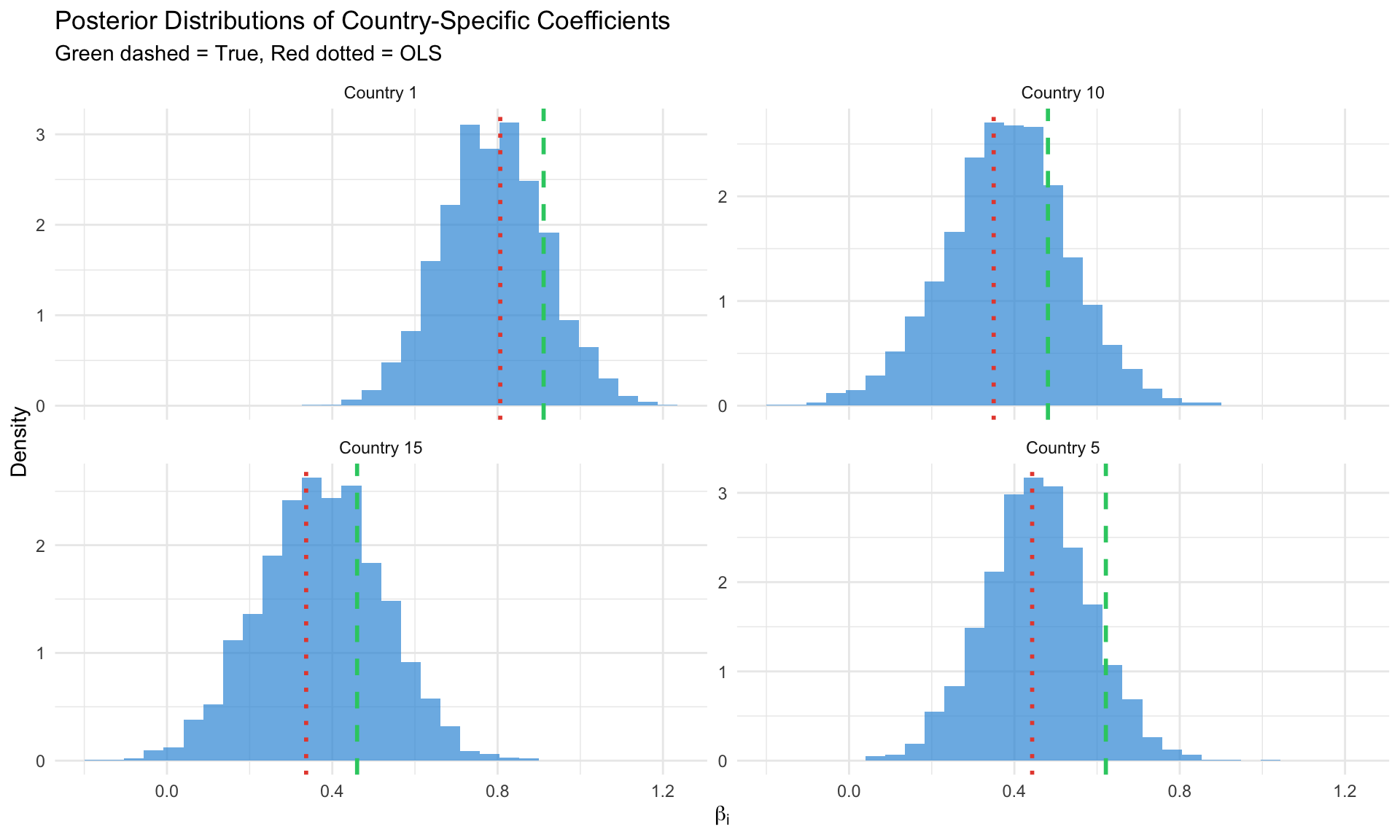

Consider a simple panel regression: \[ y_{it} = x_{it}'\beta_i + \varepsilon_{it}, \quad \varepsilon_{it} \sim N(0, \sigma^2_i) \]

Level 1 (Within-Country): \[ \beta_i | \mu, \Omega \sim N(\mu, \Omega) \]

Level 2 (Across-Countries): \[ \mu \sim N(\mu_0, V_0), \quad \Omega \sim \text{Inverse-Wishart}(\Omega_0, \nu_0) \]

The country-specific coefficients \(\beta_i\) are drawn from a common distribution with unknown mean \(\mu\) and variance \(\Omega\).

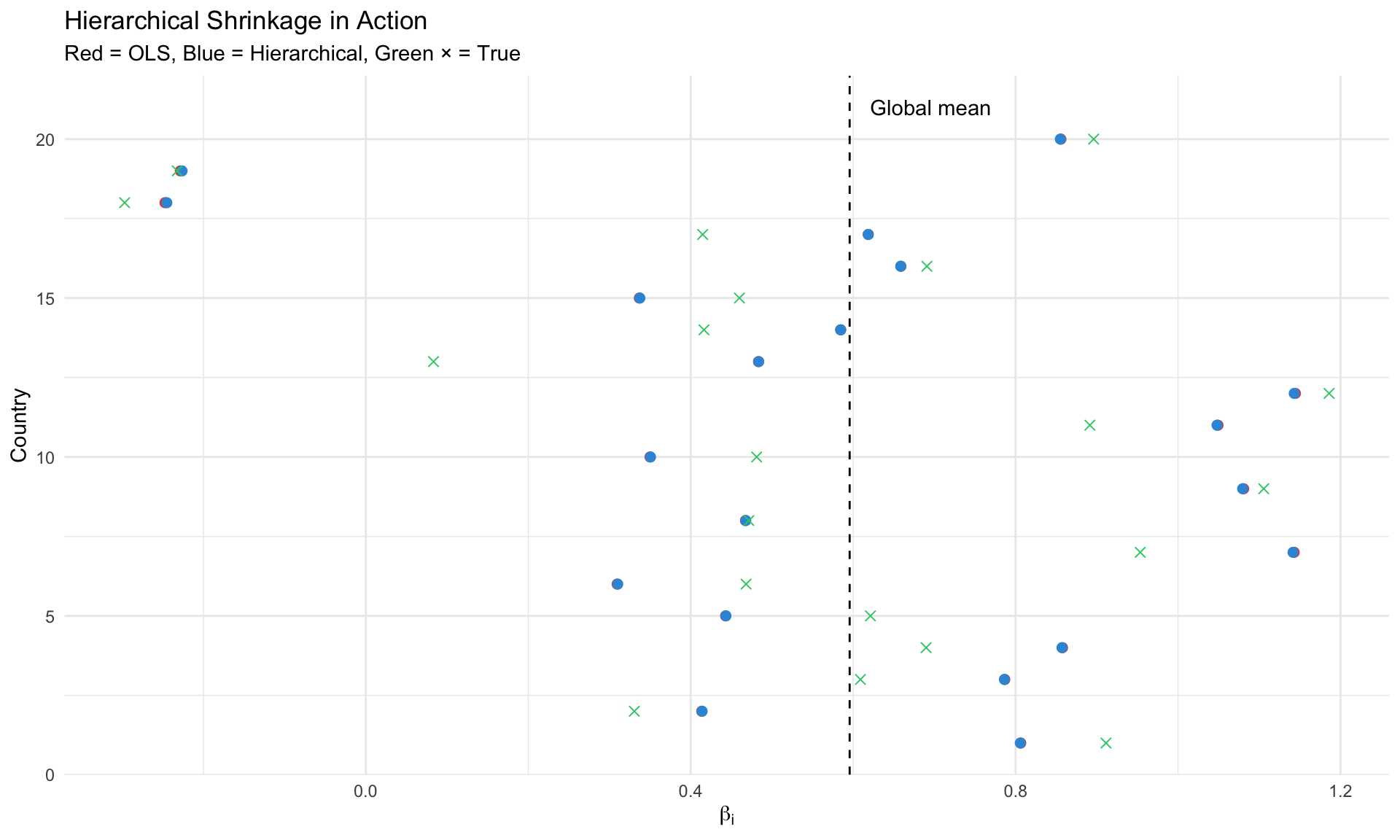

Shrinkage and Partial Pooling

The posterior for \(\beta_i\) combines:

- Country-specific data (likelihood)

- Cross-country information (hierarchical prior)

\[ \hat{\beta}_i^{\text{Bayes}} = \lambda_i \hat{\beta}_i^{\text{OLS}} + (1 - \lambda_i) \bar{\beta} \]

where \(\lambda_i \in [0,1]\) depends on: - Precision of country data: More data → less shrinkage - Cross-country heterogeneity: More variance in \(\Omega\) → less shrinkage

Why Shrinkage Helps

Key Insight: Countries with less precise estimates get shrunk more toward the global mean.

| Country Type | Data Quality | Shrinkage | Result |

|---|---|---|---|

| Data-rich (US, Germany) | High | Low | Near OLS |

| Data-poor (small EMs) | Low | High | Near global mean |

This is not bias — it’s optimal use of information under the hierarchical structure.

Gibbs Sampler for Hierarchical Panel

The Algorithm

For the hierarchical linear model:

Block 1: Draw \(\beta_i | y_i, \mu, \Omega, \sigma^2_i\) for each country \[ \beta_i | \cdot \sim N\left( V_i^{-1}(X_i'y_i/\sigma^2_i + \Omega^{-1}\mu), V_i^{-1} \right) \] where \(V_i = X_i'X_i/\sigma^2_i + \Omega^{-1}\)

Block 2: Draw \(\sigma^2_i | y_i, \beta_i\) \[ \sigma^2_i | \cdot \sim \text{Inverse-Gamma}\left( \frac{T_i}{2}, \frac{(y_i - X_i\beta_i)'(y_i - X_i\beta_i)}{2} \right) \]

Block 3: Draw \(\mu | \beta_1, \ldots, \beta_N, \Omega\) \[ \mu | \cdot \sim N\left( (N\Omega^{-1} + V_0^{-1})^{-1}(N\Omega^{-1}\bar{\beta} + V_0^{-1}\mu_0), (N\Omega^{-1} + V_0^{-1})^{-1} \right) \]

Block 4: Draw \(\Omega | \beta_1, \ldots, \beta_N, \mu\) \[ \Omega | \cdot \sim \text{Inverse-Wishart}\left( \Omega_0 + \sum_{i=1}^N (\beta_i - \mu)(\beta_i - \mu)', \nu_0 + N \right) \]

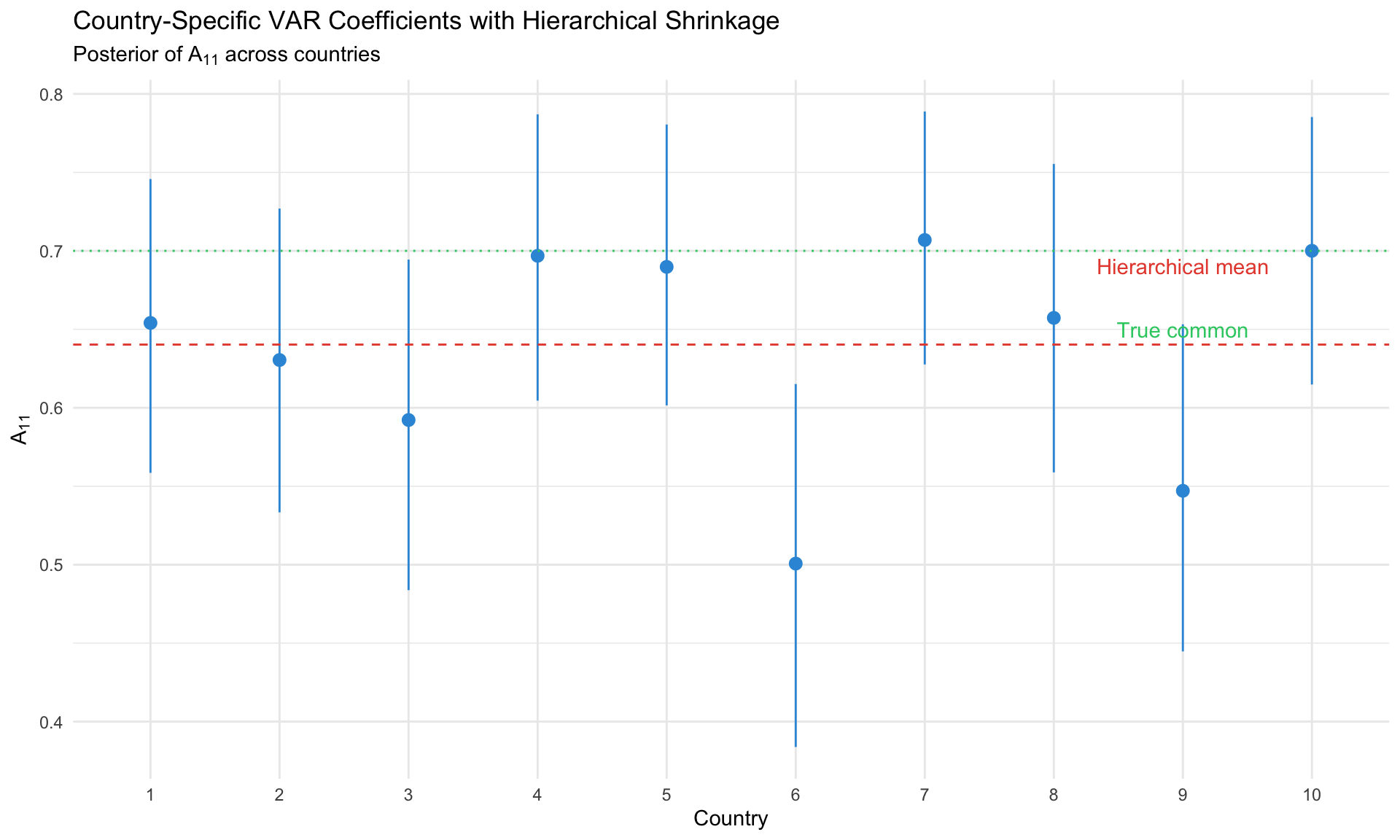

Bayesian Panel VAR

The Model Structure

For N countries, each with a K-variable VAR(p):

\[ y_{it} = c_i + A_{i,1} y_{i,t-1} + \cdots + A_{i,p} y_{i,t-p} + u_{it} \]

Hierarchical Prior: \[ \text{vec}(B_i) | \mu_B, \Omega_B \sim N(\mu_B, \Omega_B) \]

where \(B_i = [c_i, A_{i,1}, \ldots, A_{i,p}]'\) stacks all VAR coefficients for country \(i\).

Why Panel VAR?

| Feature | Separate VARs | Pooled VAR | Panel VAR |

|---|---|---|---|

| Heterogeneity | Yes | No | Yes |

| Sample size | T per country | N×T | N×T (shared info) |

| Curse of dimensionality | Severe | Moderate | Mitigated |

| Interpretation | Country-specific | Global average | Both |

With K = 3 variables, p = 2 lags, and T = 84: - Parameters per country: 3 × (1 + 3×2) = 21 - Observations per country: 84 - 2 = 82 - Degrees of freedom: Tight!

Hierarchical pooling provides effective sample size boost without forcing homogeneity.

Mean-Group Prior Structure

Following Canova & Ciccarelli (2009), we can decompose:

\[ B_i = \underbrace{\bar{B}}_{\text{common}} + \underbrace{\tilde{B}_i}_{\text{country-specific}} + \underbrace{Z_i \gamma}_{\text{observed heterogeneity}} \]

where: - \(\bar{B}\): Common component (global dynamics) - \(\tilde{B}_i\): Idiosyncratic deviation - \(Z_i\): Country characteristics (GDP per capita, openness, institutions)

Gibbs Sampler for Panel VAR

Estimating Panel VAR...Draw 500 of 2500

Draw 1000 of 2500

Draw 1500 of 2500

Draw 2000 of 2500

Draw 2500 of 2500

Random Coefficients Models

Swamy (1970) Random Coefficients

The classic frequentist approach:

\[ y_{it} = x_{it}'\beta_i + \varepsilon_{it} \] \[ \beta_i = \bar{\beta} + v_i, \quad v_i \sim N(0, \Omega) \]

Bayesian version adds priors on \((\bar{\beta}, \Omega)\) and uses Gibbs sampling.

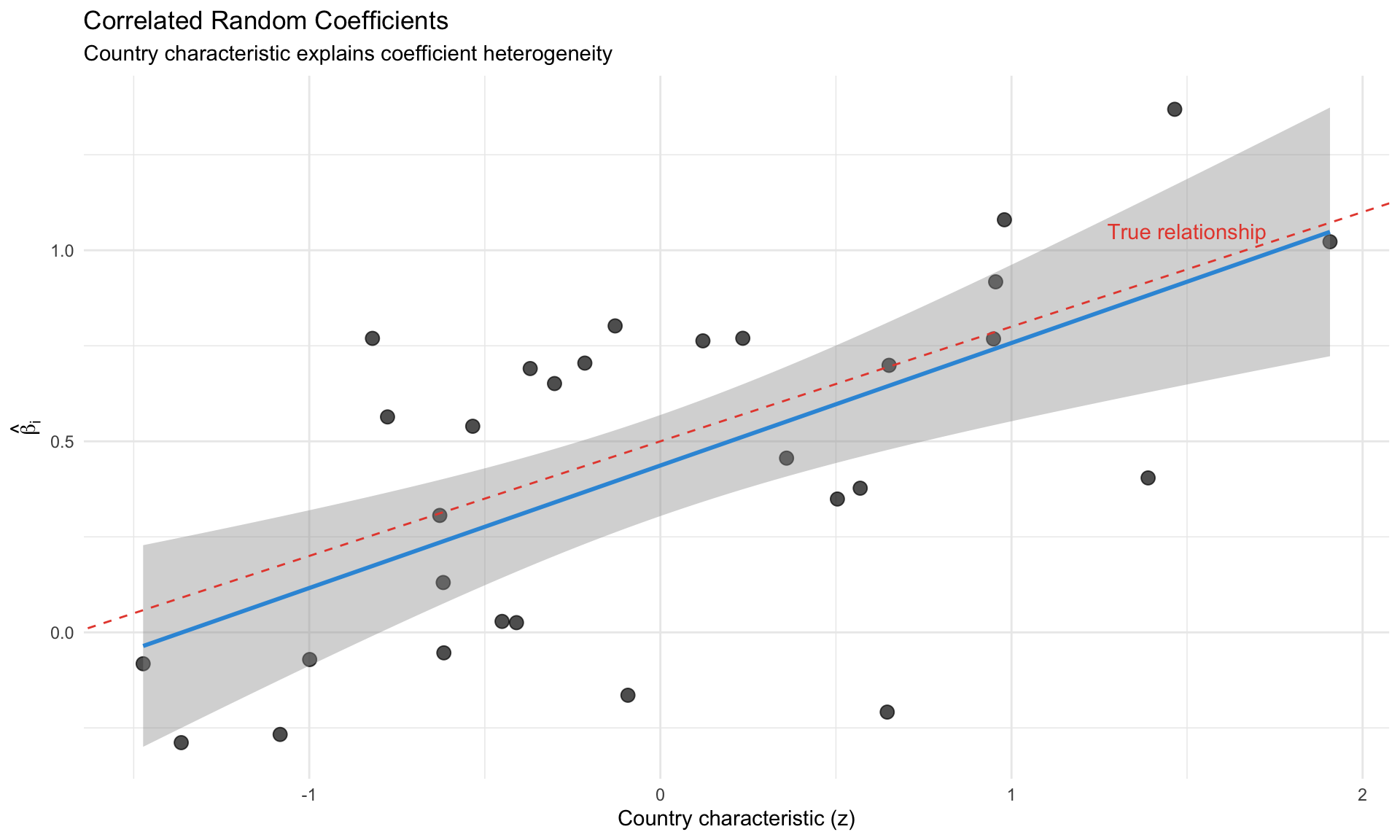

Correlated Random Coefficients

Allow \(\beta_i\) to correlate with observables:

\[ \beta_i = \bar{\beta} + Z_i'\gamma + v_i \]

where \(Z_i\) are country characteristics (GDP per capita, openness, institutions).

Application: Countries with higher institutional quality might have different Taylor rule coefficients.

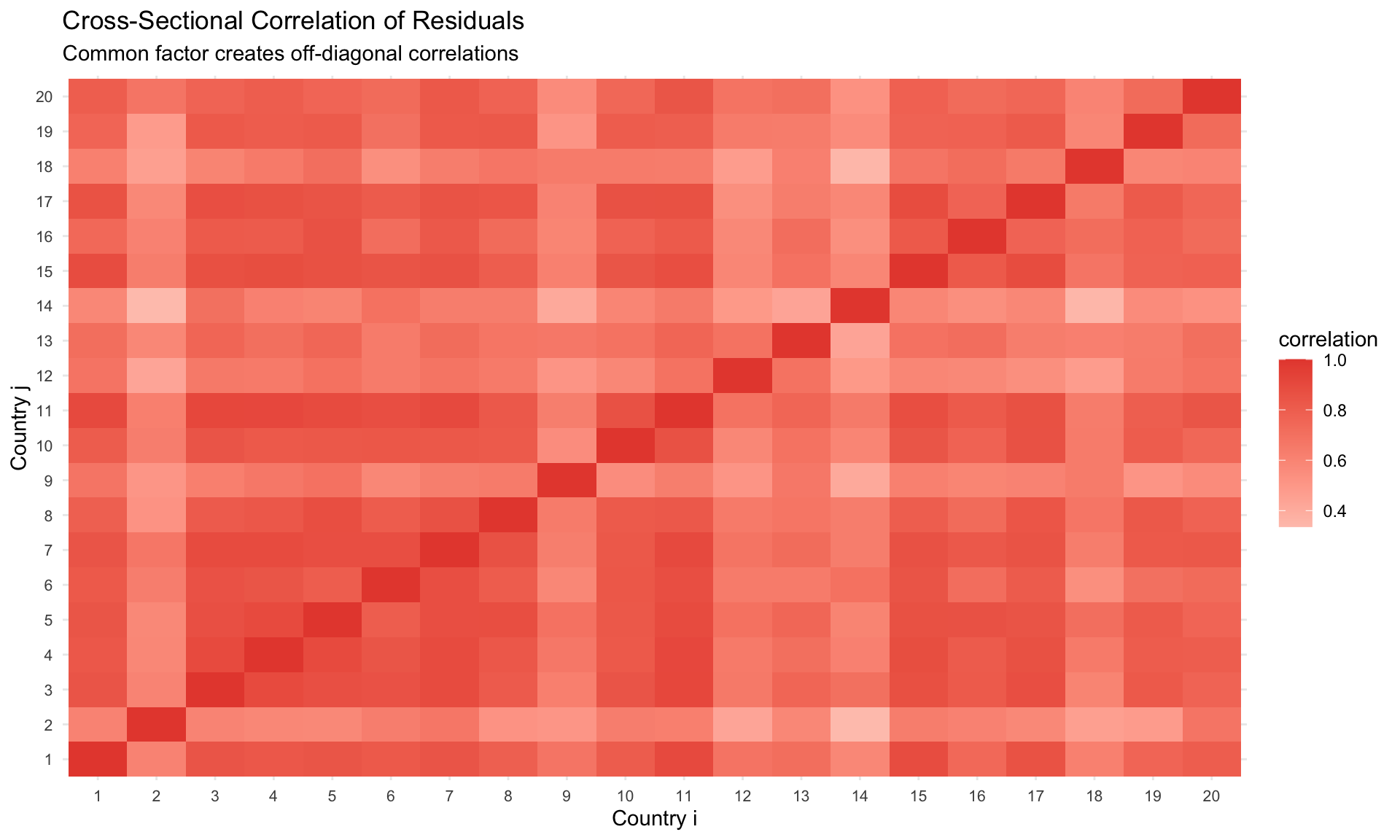

Cross-Sectional Dependence

The Problem

Standard panel methods assume: \[ E[\varepsilon_{it} \varepsilon_{js}] = 0 \quad \text{for } i \neq j \]

But in macro panels, global shocks (oil prices, US monetary policy, COVID) create cross-sectional dependence.

Factor Structure Approach

Model the error as: \[ \varepsilon_{it} = \lambda_i' f_t + e_{it} \]

where: - \(f_t\): Common factors (K_f × 1) - \(\lambda_i\): Country-specific factor loadings - \(e_{it}\): Idiosyncratic error

Interactive Fixed Effects (Bai 2009)

\[ y_{it} = x_{it}'\beta + \lambda_i' f_t + e_{it} \]

Jointly estimates \(\beta\), \(\Lambda = [\lambda_1, \ldots, \lambda_N]'\), and \(F = [f_1, \ldots, f_T]'\).

Bayesian Factor Model

Prior structure: \[ f_t | \Sigma_f \sim N(0, \Sigma_f), \quad \lambda_i \sim N(0, \Omega_\lambda) \]

Identification: Impose lower-triangular structure on loadings (first K_f countries).

Bayesian Factor-Augmented Panel VAR

Combine hierarchical panel VAR with factor structure:

\[ y_{it} = c_i + A_i y_{i,t-1} + \Gamma_i f_t + u_{it} \]

where \(f_t\) is a vector of global factors (extracted or observed).

Application in macro: Include Global Financial Cycle (GFC) factor from Miranda-Agrippino & Rey.

Python Implementation

For larger panels or more complex hierarchical structures, Python with NumPy/SciPy provides flexibility.

# Hierarchical Panel Model in Python

import numpy as np

from scipy import stats

from scipy.linalg import solve, cholesky

def hierarchical_panel_gibbs(y_list, X_list, n_draw=5000, n_burn=1000):

"""

Gibbs sampler for hierarchical panel regression.

y_list: list of (T_i,) arrays - outcomes by country

X_list: list of (T_i, K) arrays - regressors by country

"""

N = len(y_list)

K = X_list[0].shape[1]

# Priors

mu0 = np.zeros(K)

V0 = np.eye(K) * 10

V0_inv = np.linalg.inv(V0)

Omega0 = np.eye(K)

nu0 = K + 2

a0, b0 = 0.01, 0.01 # for sigma^2

# Storage

beta_draws = np.zeros((n_draw, N, K))

mu_draws = np.zeros((n_draw, K))

Omega_draws = np.zeros((n_draw, K, K))

# Initialize

beta_curr = np.zeros((N, K))

for i in range(N):

beta_curr[i] = np.linalg.lstsq(X_list[i], y_list[i], rcond=None)[0]

sigma2_curr = np.ones(N)

mu_curr = beta_curr.mean(axis=0)

Omega_curr = np.cov(beta_curr.T) + 0.01 * np.eye(K)

for g in range(n_draw + n_burn):

Omega_inv = np.linalg.inv(Omega_curr)

# Block 1: Draw beta_i | rest

for i in range(N):

X_i, y_i = X_list[i], y_list[i]

XtX = X_i.T @ X_i

Xty = X_i.T @ y_i

V_post_inv = XtX / sigma2_curr[i] + Omega_inv

V_post = np.linalg.inv(V_post_inv)

m_post = V_post @ (Xty / sigma2_curr[i] + Omega_inv @ mu_curr)

beta_curr[i] = np.random.multivariate_normal(m_post, V_post)

# Block 2: Draw sigma2_i | rest

for i in range(N):

resid = y_list[i] - X_list[i] @ beta_curr[i]

T_i = len(y_list[i])

a_post = a0 + T_i / 2

b_post = b0 + np.sum(resid**2) / 2

sigma2_curr[i] = 1 / np.random.gamma(a_post, 1/b_post)

# Block 3: Draw mu | rest

V_mu_post = np.linalg.inv(N * Omega_inv + V0_inv)

m_mu_post = V_mu_post @ (N * Omega_inv @ beta_curr.mean(axis=0) +

V0_inv @ mu0)

mu_curr = np.random.multivariate_normal(m_mu_post, V_mu_post)

# Block 4: Draw Omega | rest (Inverse Wishart)

S_post = Omega0.copy()

for i in range(N):

diff = beta_curr[i] - mu_curr

S_post += np.outer(diff, diff)

# Draw from Inverse Wishart

df_post = nu0 + N

Omega_curr = stats.invwishart.rvs(df=df_post, scale=S_post)

# Store

if g >= n_burn:

idx = g - n_burn

beta_draws[idx] = beta_curr

mu_draws[idx] = mu_curr

Omega_draws[idx] = Omega_curr

return {

'beta': beta_draws,

'mu': mu_draws,

'Omega': Omega_draws

}

# Example usage:

# result = hierarchical_panel_gibbs(y_list, X_list)

# beta_posterior_mean = result['beta'].mean(axis=0)Model Comparison for Panel Models

Marginal Likelihood

For hierarchical models, the marginal likelihood integrates over all parameters:

\[ p(Y | M) = \int p(Y | \theta) p(\theta | M) d\theta \]

For linear hierarchical models: Often tractable analytically.

For complex models: Use bridge sampling or the Chib (1995) method.

DIC and WAIC

| Criterion | Formula | Use |

|---|---|---|

| DIC | \(\bar{D} + p_D\) | Effective parameters penalty |

| WAIC | Pointwise predictive density | Better for hierarchical models |

| LOO-CV | Leave-one-out cross-validation | Gold standard but expensive |

DIC: 2873.5 Effective parameters (p_D): 36.9 Practical Guidance

When to Use Hierarchical vs. Standard Panel

| Situation | Recommendation |

|---|---|

| Small T per country (< 30) | Hierarchical (shrinkage helps) |

| Large N, moderate T | Hierarchical (efficient) |

| Focus on average effect | Either works |

| Focus on heterogeneity | Hierarchical (full posterior) |

| Strong prior beliefs | Bayesian hierarchical |

Implementation Checklist

- Check MCMC convergence: Trace plots, R-hat, effective sample size

- Assess shrinkage: Compare hierarchical to OLS estimates

- Test homogeneity: Is \(\Omega\) small relative to coefficient magnitudes?

- Cross-sectional dependence: Test residuals, consider factors

- Model comparison: DIC/WAIC across specifications

Common Pitfalls

WarningWatch Out For

- Over-shrinkage: Very tight hyperpriors force all countries to look identical

- Under-shrinkage: Vague hyperpriors fail to borrow strength

- Ignoring cross-sectional dependence: Biases standard errors downward

- Too many parameters: K-variable panel VAR with p lags has \(N \times K \times (Kp + 1)\) parameters

- Improper mixing: Hierarchical models can have slow mixing — increase draws

Key References

Hierarchical Panel Models

- Gelman & Hill (2007) Data Analysis Using Regression and Multilevel/Hierarchical Models — Accessible introduction

- Swamy (1970) “Efficient Inference in a Random Coefficient Regression Model” Econometrica — Classic random coefficients

- Hsiao (2014) Analysis of Panel Data — Comprehensive textbook

Bayesian Panel VAR

- Canova & Ciccarelli (2009) “Estimating Multicountry VAR Models” IER — Foundational paper

- Canova & Ciccarelli (2013) “Panel Vector Autoregressive Models: A Survey” — Survey chapter

- Jarocinski (2010) “Responses to Monetary Policy Shocks in the East and the West of Europe” JAE — Application

Cross-Sectional Dependence

- Bai (2009) “Panel Data Models with Interactive Fixed Effects” Econometrica — Factor structure

- Pesaran (2006) “Estimation and Inference in Large Heterogeneous Panels” Econometrica — CCE estimator

- Chudik & Pesaran (2015) “Common Correlated Effects Estimation of Heterogeneous Dynamic Panel Data Models” JoE

Software

- R:

brms(Bürkner),lme4(Bates et al.), custom Gibbs samplers - Python:

PyMC, NumPy/SciPy for manual MCMC - Stan:

rstan/pystanfor complex hierarchical models

Summary

| Concept | Key Insight |

|---|---|

| Hierarchical models | Pool information while allowing heterogeneity |

| Shrinkage | Data-poor countries borrow from data-rich |

| Panel VAR | Country-specific dynamics with common structure |

| Cross-sectional dependence | Global factors create correlations |

| Gibbs sampling | Natural framework for hierarchical models |

TipFor Your Research

With N = 46 countries and T = 84 quarters: - Hierarchical shrinkage is valuable for EM countries with noisier data - Panel VAR can reveal heterogeneity in policy transmission - Factor structures capture global shocks (GFC, COVID) - Always check cross-sectional correlation in residuals