DSGE Foundations

Microfoundations, the New Keynesian Model, and Solution Methods

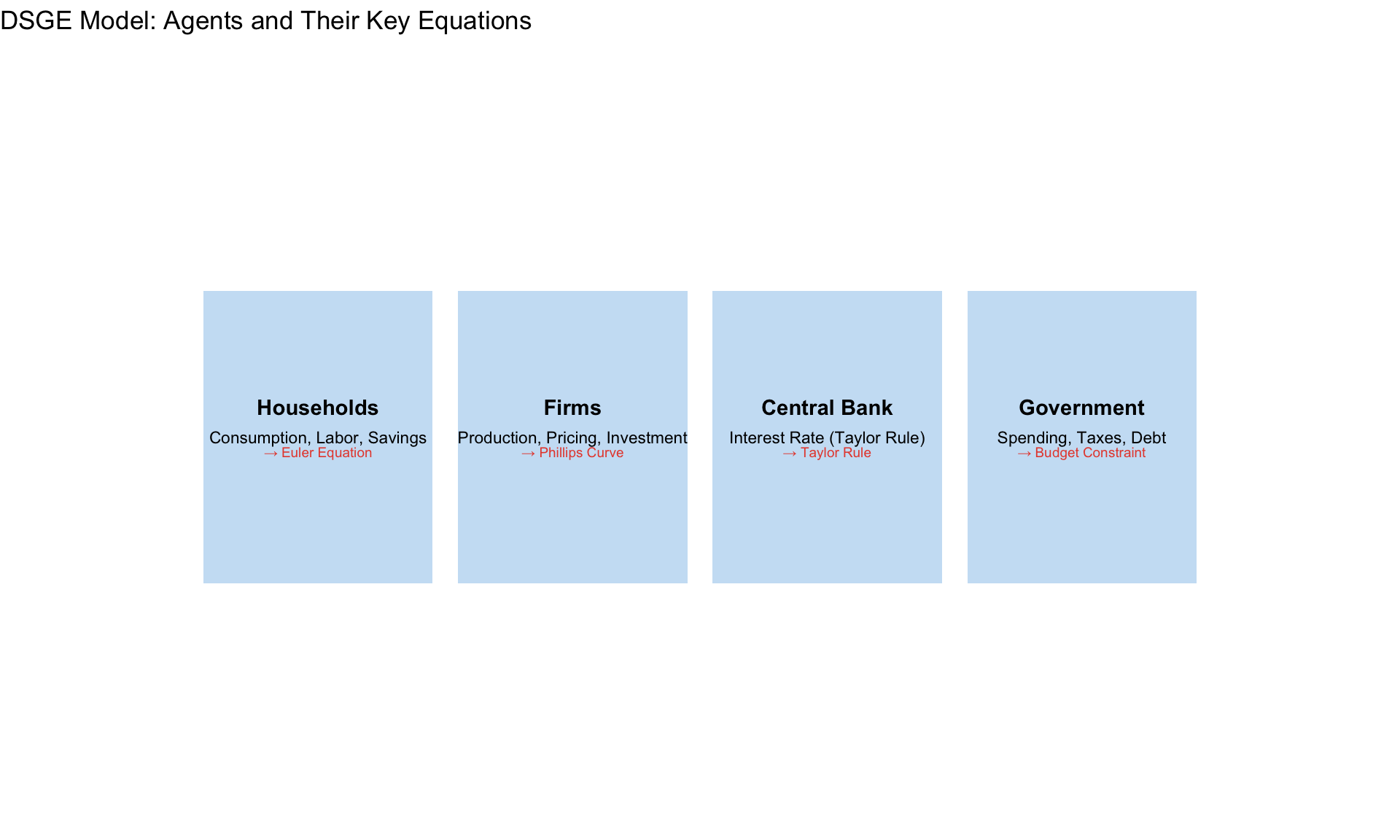

What is a DSGE Model?

Dynamic Stochastic General Equilibrium models are the workhorse of modern macroeconomics. They combine:

| Component | Meaning |

|---|---|

| Dynamic | Agents optimize over time, considering future |

| Stochastic | Random shocks drive business cycle fluctuations |

| General | All markets (goods, labor, capital) interact |

| Equilibrium | Supply equals demand in every market |

NoteThe Core Philosophy

DSGE models are microfounded: aggregate behavior emerges from explicit optimization by households, firms, and policymakers. No ad hoc aggregate relationships.

From Micro to Macro

The General Form

All DSGE models can be written as:

\[ \mathbb{E}_t\left[f(y_{t+1}, y_t, y_{t-1}, u_t)\right] = 0 \]

where:

- \(y_t\) = vector of endogenous variables (output, inflation, interest rate, capital, …)

- \(u_t\) = vector of exogenous shocks (technology, monetary, fiscal, …)

- \(f\) = system of equilibrium conditions (Euler equations, market clearing, …)

- \(\mathbb{E}_t\) = expectation conditional on time-\(t\) information

The challenge: solving for \(y_t\) as a function of states and shocks.

The RBC Core

Before New Keynesian elements, we start with the Real Business Cycle foundation.

Household Problem

A representative household maximizes expected lifetime utility:

\[ \max_{\{C_t, N_t, K_t\}} \mathbb{E}_0 \sum_{t=0}^{\infty} \beta^t U(C_t, N_t) \]

Subject to budget constraint: \[ C_t + K_t = W_t N_t + R_t^K K_{t-1} + \Pi_t - T_t + (1-\delta)K_{t-1} \]

where: - \(C_t\) = consumption - \(N_t\) = labor supply - \(K_t\) = end-of-period capital - \(W_t\) = real wage - \(R_t^K\) = rental rate on capital - \(\delta\) = depreciation rate - \(\Pi_t\) = firm profits - \(T_t\) = lump-sum taxes

First-Order Conditions

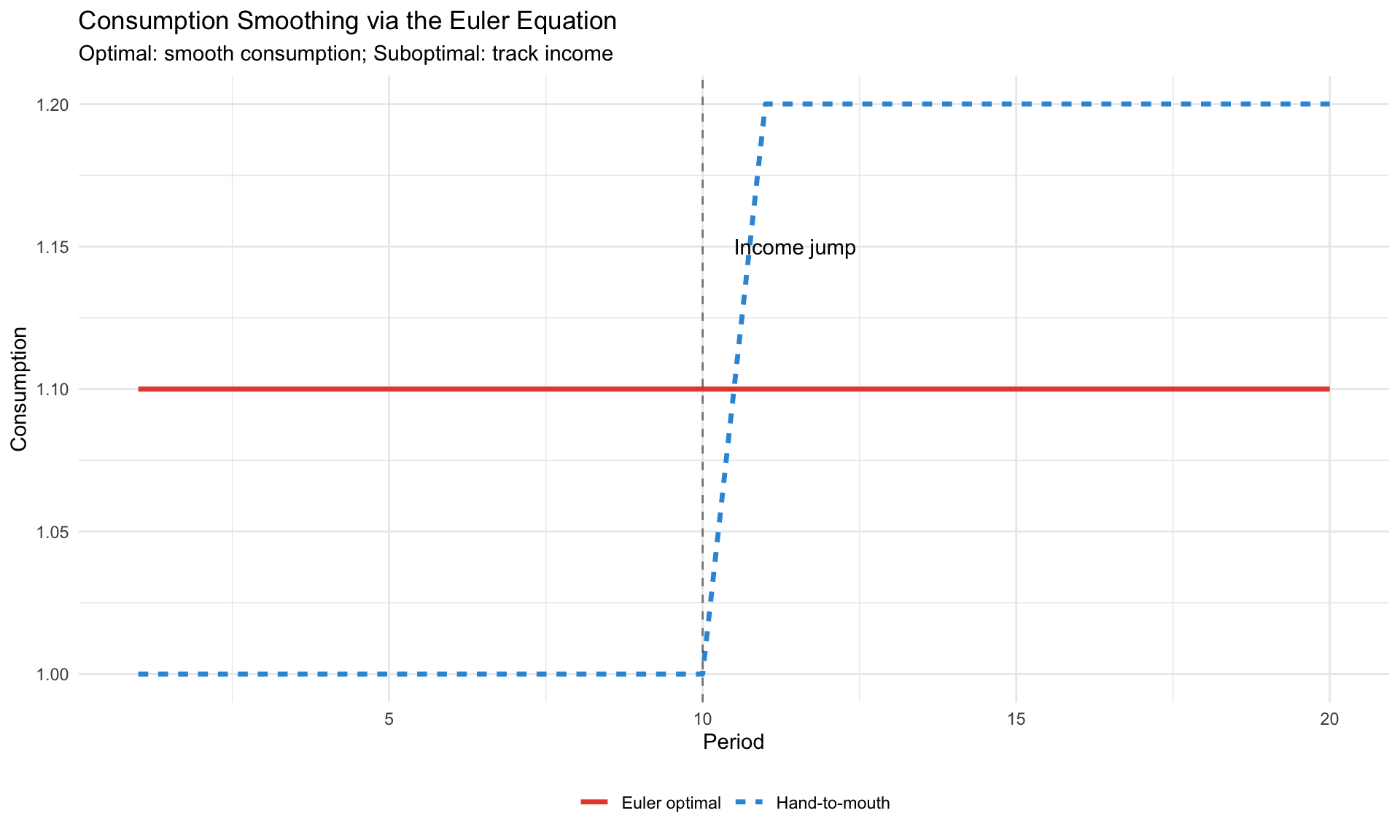

Euler equation (intertemporal consumption choice): \[ U_C(C_t, N_t) = \beta \mathbb{E}_t\left[U_C(C_{t+1}, N_{t+1}) \cdot (R_{t+1}^K + 1 - \delta)\right] \]

Labor supply (consumption-leisure trade-off): \[ \frac{-U_N(C_t, N_t)}{U_C(C_t, N_t)} = W_t \]

Example: Log Utility

With \(U(C, N) = \log(C) - \chi \frac{N^{1+\phi}}{1+\phi}\):

\[ \frac{1}{C_t} = \beta \mathbb{E}_t\left[\frac{1}{C_{t+1}} (R_{t+1}^K + 1 - \delta)\right] \]

\[ \chi N_t^\phi \cdot C_t = W_t \]

Firm Problem

A representative firm maximizes profits with Cobb-Douglas production:

\[ Y_t = A_t K_{t-1}^\alpha N_t^{1-\alpha} \]

Factor demands (competitive markets, firms are price-takers): \[ W_t = (1-\alpha) \frac{Y_t}{N_t} \] \[ R_t^K = \alpha \frac{Y_t}{K_{t-1}} \]

Technology shock follows AR(1): \[ \log(A_t) = \rho_A \log(A_{t-1}) + \varepsilon_{A,t}, \quad \varepsilon_{A,t} \sim N(0, \sigma_A^2) \]

Market Clearing

\[ Y_t = C_t + I_t \]

where investment \(I_t = K_t - (1-\delta)K_{t-1}\).

The Complete RBC Model

| Equation | Name | Variables |

|---|---|---|

| \(\frac{1}{C_t} = \beta \mathbb{E}_t\left[\frac{1}{C_{t+1}}(R_{t+1}^K + 1 - \delta)\right]\) | Euler | \(C, R^K\) |

| \(\chi N_t^\phi C_t = W_t\) | Labor supply | \(N, C, W\) |

| \(Y_t = A_t K_{t-1}^\alpha N_t^{1-\alpha}\) | Production | \(Y, A, K, N\) |

| \(W_t = (1-\alpha) Y_t / N_t\) | Labor demand | \(W, Y, N\) |

| \(R_t^K = \alpha Y_t / K_{t-1}\) | Capital demand | \(R^K, Y, K\) |

| \(Y_t = C_t + K_t - (1-\delta)K_{t-1}\) | Resource | \(Y, C, K\) |

| \(\log A_t = \rho_A \log A_{t-1} + \varepsilon_A\) | Technology | \(A\) |

7 equations, 7 unknowns: \((Y, C, N, K, W, R^K, A)\)

The New Keynesian Model

The RBC model has no role for monetary policy (all real). The New Keynesian model adds:

- Nominal rigidities (sticky prices/wages)

- Monopolistic competition (firms have pricing power)

- Monetary policy (central bank sets interest rate)

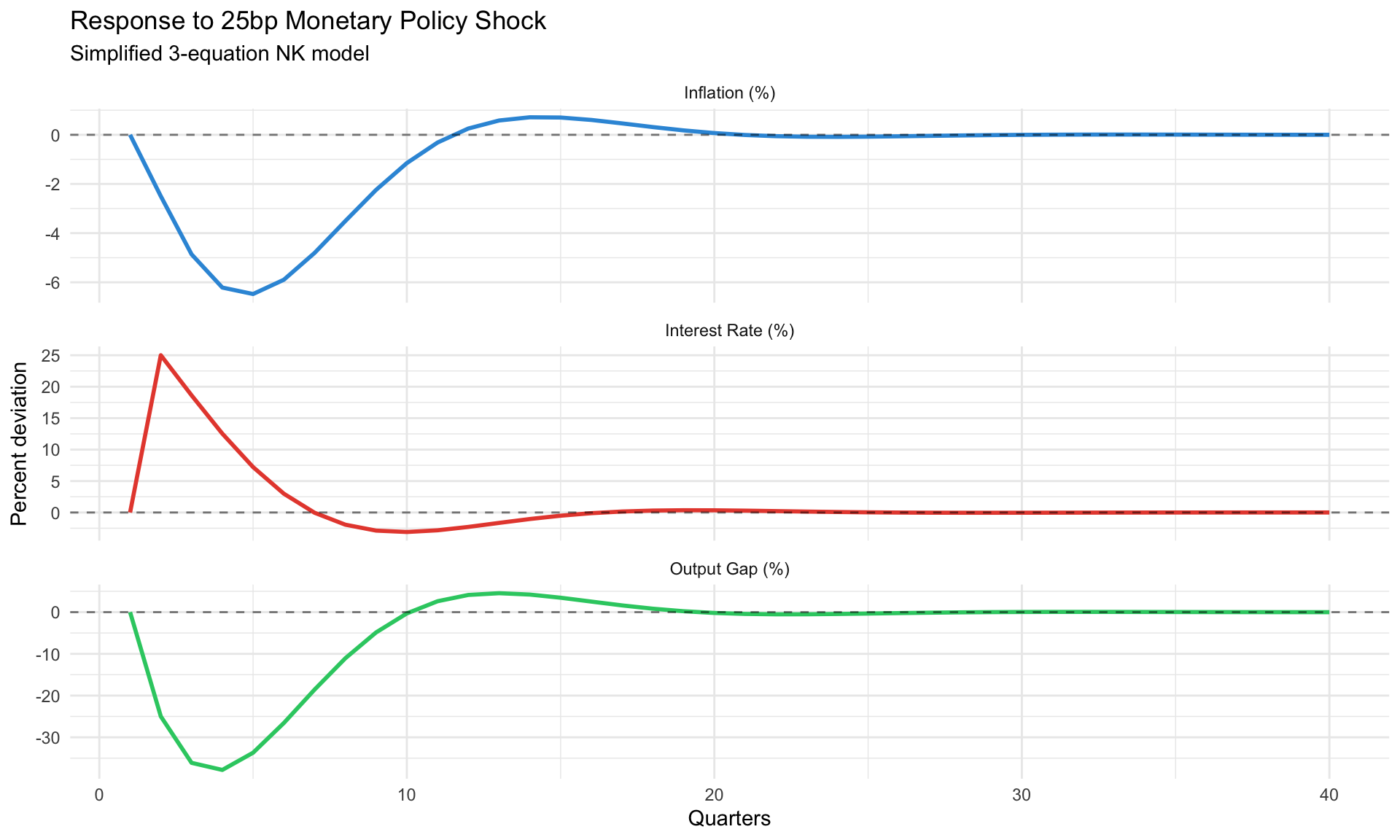

The 3-Equation NK Model

The canonical log-linearized NK model:

1. IS Curve (Dynamic IS)

From the household’s Euler equation: \[ \hat{y}_t = \mathbb{E}_t[\hat{y}_{t+1}] - \frac{1}{\sigma}(i_t - \mathbb{E}_t[\pi_{t+1}] - r_t^n) \]

where: - \(\hat{y}_t\) = output gap (deviation from flexible-price equilibrium) - \(i_t\) = nominal interest rate - \(\pi_t\) = inflation - \(r_t^n\) = natural rate of interest - \(\sigma\) = inverse elasticity of intertemporal substitution

Interpretation: Higher real interest rate → postpone consumption → lower output today.

2. Phillips Curve (NKPC)

From Calvo pricing (fraction \(1-\theta\) of firms adjust each period): \[ \pi_t = \beta \mathbb{E}_t[\pi_{t+1}] + \kappa \hat{y}_t \]

where: \[ \kappa = \frac{(1-\theta)(1-\beta\theta)}{\theta} \cdot (\sigma + \phi) \]

Interpretation: Inflation today depends on expected future inflation plus current output gap (marginal cost pressure).

3. Taylor Rule

Central bank sets interest rate: \[ i_t = \rho_i i_{t-1} + (1-\rho_i)\left[r^* + \phi_\pi(\pi_t - \pi^*) + \phi_y \hat{y}_t\right] + \varepsilon_{m,t} \]

Standard calibration:

| Parameter | Value | Interpretation |

|---|---|---|

| \(\rho_i\) | 0.8 | Interest rate smoothing |

| \(\phi_\pi\) | 1.5 | Response to inflation (Taylor principle: \(\phi_\pi > 1\)) |

| \(\phi_y\) | 0.5/4 = 0.125 | Response to output gap (quarterly) |

Deriving the Phillips Curve

Calvo Pricing Setup

- Each period, fraction \(1-\theta\) of firms can reset prices

- Fraction \(\theta\) are “stuck” with last period’s price

- When firms can adjust, they set price to maximize expected profits over the time they’ll be stuck

Optimal Price Setting

A firm that can adjust at time \(t\) chooses \(P_t^*\) to maximize: \[ \mathbb{E}_t \sum_{k=0}^{\infty} (\beta\theta)^k \left[ \frac{P_t^*}{P_{t+k}} Y_{t+k|t} - MC_{t+k} Y_{t+k|t} \right] \]

Result (after log-linearization): \[ \hat{p}_t^* = (1-\beta\theta) \sum_{k=0}^{\infty} (\beta\theta)^k \mathbb{E}_t[\widehat{mc}_{t+k}] \]

Firms set prices as a weighted average of expected future marginal costs.

Aggregating to the Phillips Curve

Price index evolution: \[ P_t = \left[\theta P_{t-1}^{1-\epsilon} + (1-\theta)(P_t^*)^{1-\epsilon}\right]^{\frac{1}{1-\epsilon}} \]

Log-linearizing and combining: \[ \pi_t = \beta \mathbb{E}_t[\pi_{t+1}] + \kappa \cdot \widehat{mc}_t \]

With \(\widehat{mc}_t \propto \hat{y}_t\) (output gap approximates marginal cost deviations).

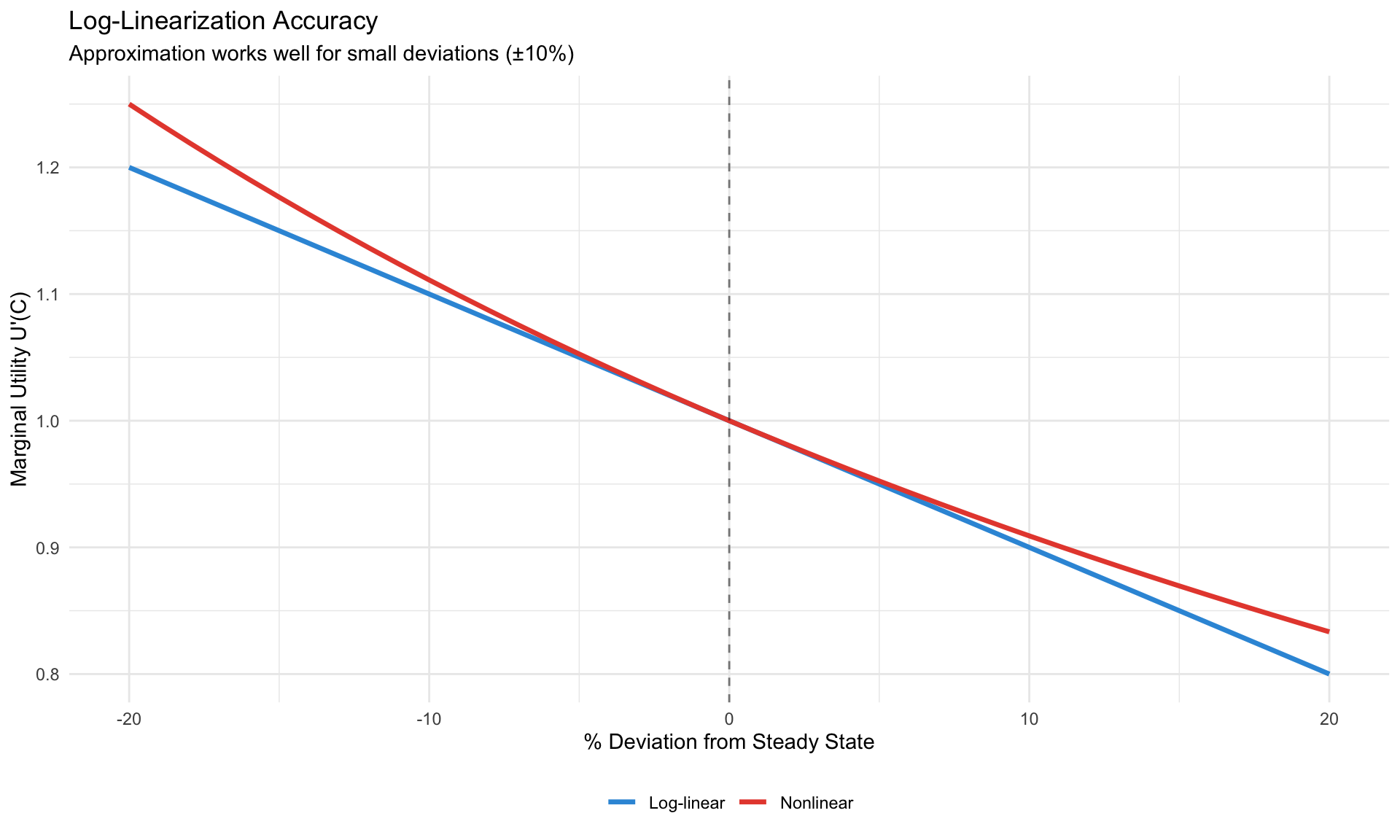

Log-Linearization

DSGE models are nonlinear. To solve them analytically (or with first-order perturbation), we log-linearize around the steady state.

The Technique

For any variable \(X_t\):

\[ \hat{x}_t \equiv \log(X_t) - \log(\bar{X}) = \log\left(\frac{X_t}{\bar{X}}\right) \approx \frac{X_t - \bar{X}}{\bar{X}} \]

So \(\hat{x}_t\) is the percentage deviation from steady state.

Key Approximation

For any function \(f(X_t, Y_t)\): \[ f(X_t, Y_t) \approx f(\bar{X}, \bar{Y}) + f_X(\bar{X}, \bar{Y})(X_t - \bar{X}) + f_Y(\bar{X}, \bar{Y})(Y_t - \bar{Y}) \]

Example: Euler Equation

Nonlinear Euler: \[ \frac{1}{C_t} = \beta \mathbb{E}_t\left[\frac{1}{C_{t+1}} R_{t+1}\right] \]

Step 1: Steady state \[ \frac{1}{\bar{C}} = \beta \frac{1}{\bar{C}} \bar{R} \implies \bar{R} = \frac{1}{\beta} \]

Step 2: Log-linearize. Let \(C_t = \bar{C} e^{\hat{c}_t} \approx \bar{C}(1 + \hat{c}_t)\): \[ \frac{1}{\bar{C}(1 + \hat{c}_t)} = \beta \mathbb{E}_t\left[\frac{1}{\bar{C}(1 + \hat{c}_{t+1})} \bar{R}(1 + \hat{r}_{t+1})\right] \]

Step 3: First-order Taylor expansion (ignore second-order terms): \[ 1 - \hat{c}_t = \beta \bar{R} \mathbb{E}_t\left[(1 - \hat{c}_{t+1})(1 + \hat{r}_{t+1})\right] \] \[ 1 - \hat{c}_t \approx \mathbb{E}_t[1 - \hat{c}_{t+1} + \hat{r}_{t+1}] \]

Result: \[ \hat{c}_t = \mathbb{E}_t[\hat{c}_{t+1}] - (\hat{r}_{t+1} - 0) \]

This is the log-linearized Euler equation (with \(\sigma = 1\)).

Solving Rational Expectations Models

After log-linearization, DSGE models take the form:

\[ A \mathbb{E}_t[y_{t+1}] = B y_t + C u_t \]

where \(y_t\) contains both predetermined (state) and jump (control) variables.

Partitioning the System

Split \(y_t = \begin{pmatrix} x_t \\ z_t \end{pmatrix}\) where:

- \(x_t\): Predetermined (state) variables — known at time \(t\) (e.g., capital \(K_{t-1}\))

- \(z_t\): Jump (forward-looking) variables — can adjust freely (e.g., consumption, inflation)

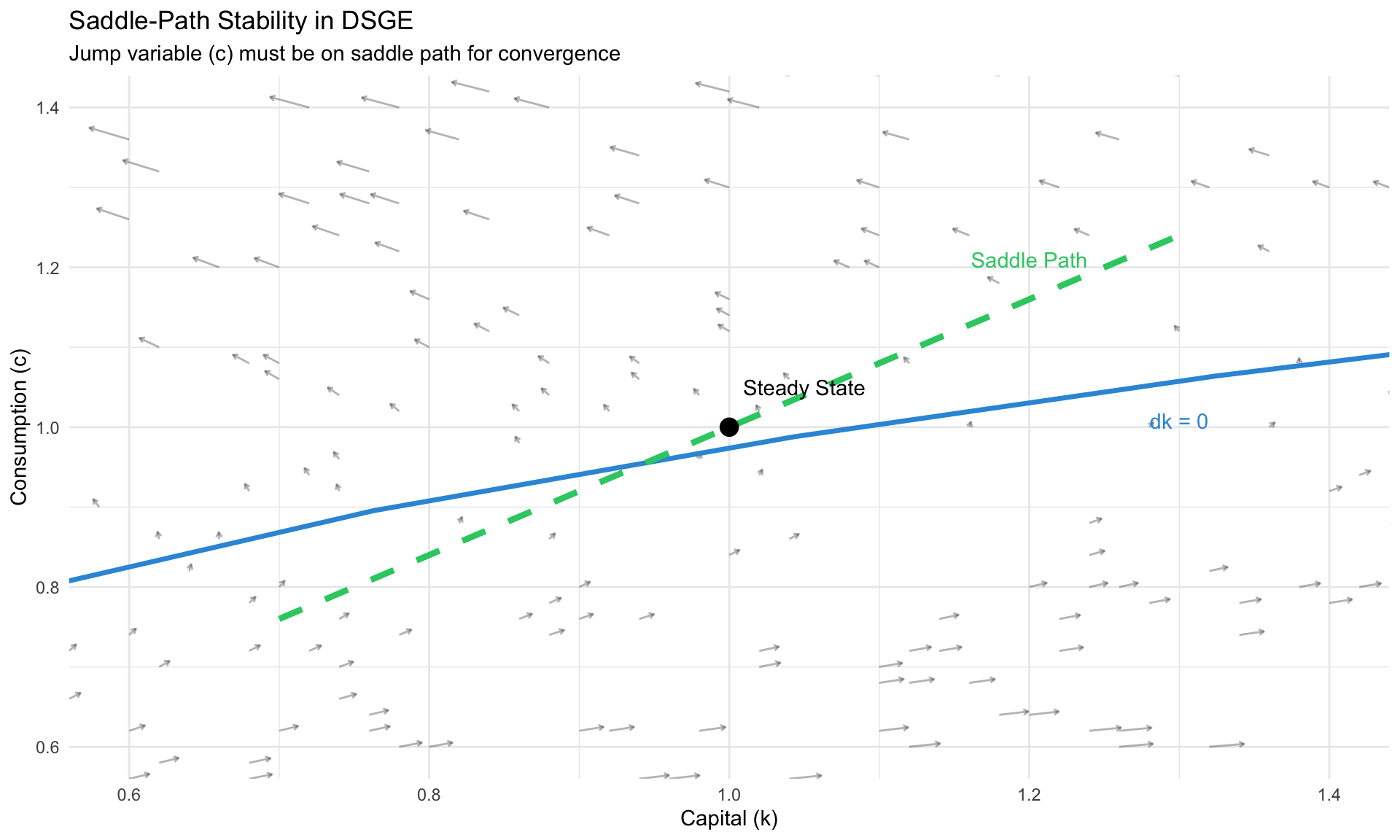

Blanchard-Kahn Conditions

The eigenvalue decomposition of the system matrix determines solvability (Blanchard and Kahn 1980).

ImportantBlanchard-Kahn (1980) Conditions

For a unique stable solution:

Number of eigenvalues outside unit circle = Number of jump variables

| Eigenvalue Count | Diagnosis |

|---|---|

| Equals number of jump vars | Unique solution (saddle-path stable) |

| Less than number of jump vars | Indeterminacy (multiple equilibria, sunspots) |

| Greater than number of jump vars | No solution (explosive dynamics) |

The Solution Form

If BK conditions hold, the solution is:

\[ x_{t+1} = H_x x_t + H_u u_{t+1} \] \[ z_t = G_x x_t \]

The policy function \(G_x\) tells us how jump variables respond to states. The transition matrix \(H_x\) governs state evolution.

Common Causes of BK Violations

| Problem | Symptom | Common Fix |

|---|---|---|

| Taylor principle violated | Too few unstable roots | Raise \(\phi_\pi\) above 1 |

| Missing expectations | Wrong root count | Check all \(\mathbb{E}_t\) terms |

| Timing error | Explosive solutions | Dynare uses end-of-period capital: use \(K(-1)\) |

| Wrong variable classification | Indeterminacy | Re-check predetermined vs. jump |

Numerical Solution: QZ Decomposition

For larger models, we use the generalized Schur (QZ) decomposition:

\[ A = Q \Lambda Z', \quad B = Q \Omega Z' \]

where \(\Lambda/\Omega\) gives generalized eigenvalues. Reorder to put unstable eigenvalues in the bottom block.

# R code sketch for BK solution

solve_dsge_bk <- function(A, B, n_state) {

# A * E[y_{t+1}] = B * y_t

# y = [x; z] where x = states, z = jumps

n_total <- nrow(A)

n_jump <- n_total - n_state

# QZ decomposition

qz <- geigen::gqz(A, B) # Generalized Schur

# Eigenvalues

eig <- qz$alpha / qz$beta

n_unstable <- sum(abs(eig) > 1)

# Check BK conditions

if (n_unstable != n_jump) {

stop(paste("BK violation:", n_unstable, "unstable,", n_jump, "jump vars"))

}

# Extract policy function (from stable block)

# ... (reorder and partition)

list(G = G_matrix, H = H_matrix, eigenvalues = eig)

}Calibration

Before estimation (Module 11), we calibrate parameters using:

- Microeconomic evidence (labor supply elasticity, depreciation rate)

- Long-run averages (capital-output ratio, hours worked)

- Steady-state relationships (Euler equation pins down \(\beta\))

Standard RBC/NK Calibration

| Parameter | Symbol | Value | Source |

|---|---|---|---|

| Discount factor | \(\beta\) | 0.99 | Real interest rate ≈ 4% annually |

| Capital share | \(\alpha\) | 0.33 | National accounts |

| Depreciation | \(\delta\) | 0.025 | 10% annual depreciation |

| Risk aversion | \(\sigma\) | 1-2 | Micro studies |

| Frisch elasticity | \(1/\phi\) | 0.5-2 | Labor supply literature |

| Calvo parameter | \(\theta\) | 0.75 | Prices adjust every 4 quarters |

| Inflation weight | \(\phi_\pi\) | 1.5 | Taylor (1993) |

| Output weight | \(\phi_y\) | 0.125 | Taylor (1993), quarterly |

Matching Moments

Target: Model-implied moments ≈ Data moments

| Moment | Data (US) | Typical RBC |

|---|---|---|

| std(Y) | 1.5-2% | Match by calibrating \(\sigma_A\) |

| std(C)/std(Y) | 0.5-0.7 | Endogenous |

| std(I)/std(Y) | 2.5-3.5 | Endogenous |

| corr(C, Y) | 0.8-0.9 | Endogenous |

| corr(N, Y) | 0.8-0.9 | Endogenous |

| Variable | Std Dev (%)_Model | Std Dev (%)_Data | Rel to Y_Model | Rel to Y_Data | Corr with Y_Model | Corr with Y_Data |

|---|---|---|---|---|---|---|

| Output | 2.26 | 1.8 | 1.00 | 1.00 | 1.00 | 1.00 |

| Consumption | 1.60 | 1.0 | 0.71 | 0.55 | 0.99 | 0.85 |

| Investment | 6.77 | 5.0 | 2.99 | 2.80 | 1.00 | 0.90 |

| Hours | 1.14 | 1.5 | 0.50 | 0.83 | 0.96 | 0.85 |

Calibration: matching business cycle moments

Steady-State Relationships

Many parameters are pinned down by steady-state conditions:

From Euler equation: \[ \bar{R} = \frac{1}{\beta} \implies \beta = \frac{1}{1 + r^*} \] With \(r^* = 4\%\) annually → \(\beta = 1/1.01 \approx 0.99\) quarterly.

From capital demand: \[ \bar{R}^K = \alpha \frac{\bar{Y}}{\bar{K}} = \frac{1}{\beta} - (1-\delta) \] Given \(\beta\), \(\delta\), and capital-output ratio, backs out \(\alpha\).

From labor supply: \[ \chi \bar{N}^\phi \bar{C} = \bar{W} = (1-\alpha)\frac{\bar{Y}}{\bar{N}} \] Given target \(\bar{N} = 1/3\) (8 hours/day), backs out \(\chi\).

Dynare Basics

Dynare is the standard software for solving and estimating DSGE models. Here’s a minimal example.

A Simple RBC Model in Dynare

%% RBC Model - rbc_simple.mod

%% Preamble

var y c k n w r a;

varexo eps_a;

parameters BETA ALPHA DELTA RHO_A SIGMA_A CHI PHI;

%% Calibration

BETA = 0.99;

ALPHA = 0.33;

DELTA = 0.025;

RHO_A = 0.95;

SIGMA_A = 0.007;

CHI = 1; % labor disutility

PHI = 1; % inverse Frisch elasticity

%% Model equations

model;

% Euler equation

1/c = BETA * (1/c(+1)) * (r(+1) + 1 - DELTA);

% Labor supply

CHI * n^PHI * c = w;

% Production function

y = a * k(-1)^ALPHA * n^(1-ALPHA);

% Factor prices

w = (1-ALPHA) * y / n;

r = ALPHA * y / k(-1);

% Resource constraint

y = c + k - (1-DELTA)*k(-1);

% Technology shock

log(a) = RHO_A * log(a(-1)) + eps_a;

end;

%% Steady state

initval;

a = 1;

r = 1/BETA - 1 + DELTA;

k = (ALPHA/r)^(1/(1-ALPHA)) * 0.33;

n = 0.33;

y = a * k^ALPHA * n^(1-ALPHA);

c = y - DELTA*k;

w = (1-ALPHA) * y / n;

end;

steady;

check;

%% Shocks

shocks;

var eps_a; stderr SIGMA_A;

end;

%% Simulation

stoch_simul(order=1, irf=40, periods=200);Key Dynare Commands

| Command | Purpose |

|---|---|

steady |

Compute deterministic steady state |

check |

Verify Blanchard-Kahn conditions |

stoch_simul(order=1) |

First-order perturbation solution |

stoch_simul(irf=40) |

Generate IRFs for 40 periods |

estimation(...) |

Bayesian estimation (Module 11) |

model_diagnostics |

Check model specification |

Important Timing Convention

WarningDynare Timing

Dynare uses end-of-period capital: - k without subscript = \(K_t\) (end of period \(t\)) - k(-1) = \(K_{t-1}\) (beginning of period \(t\) = end of \(t-1\))

So the production function uses k(-1):

y = a * k(-1)^ALPHA * n^(1-ALPHA);Summary

| Concept | Key Insight |

|---|---|

| DSGE structure | Microfounded optimization → aggregate equilibrium |

| Households | Euler equation governs intertemporal choice |

| Firms (NK) | Calvo pricing → forward-looking Phillips curve |

| Monetary policy | Taylor rule with \(\phi_\pi > 1\) for stability |

| Log-linearization | Approximate around steady state for solution |

| Blanchard-Kahn | Saddle-path stability requires correct eigenvalue count |

| Calibration | Match parameters to micro evidence and steady-state targets |

TipNext Steps

Module 11 covers DSGE estimation: - Bayesian methods with Metropolis-Hastings - The Kalman filter for likelihood evaluation - Model comparison via marginal likelihood - Dynare’s estimation command

Key References

Foundational

- Kydland & Prescott (1982) “Time to Build and Aggregate Fluctuations” Econometrica — RBC origins

- Blanchard & Kahn (1980) “The Solution of Linear Difference Models” Econometrica — BK conditions

- Galí (2015) Monetary Policy, Inflation, and the Business Cycle — NK textbook

Medium-Scale Models

- Smets & Wouters (2003, 2007) “An Estimated DSGE Model” — Benchmark estimated NK

- Christiano, Eichenbaum & Evans (2005) “Nominal Rigidities” JPE — CEE model

Solution Methods

- Uhlig (1999) “A Toolkit for Analysing Nonlinear Dynamic Stochastic Models” — Perturbation

- Sims (2002) “Solving Linear Rational Expectations Models” — QZ decomposition

Calibration

- Cooley & Prescott (1995) “Economic Growth and Business Cycles” — Calibration methodology

- Chari, Kehoe & McGrattan (2007) “Business Cycle Accounting” Econometrica — Wedges approach

Software

- Adjemian et al. “Dynare” — Standard DSGE solver

- Herbst & Schorfheide (2016) Bayesian Estimation of DSGE Models — Modern estimation