Causal Machine Learning

Heterogeneous Treatment Effects, Causal Forests, and Double ML

# Python setup (run in your Python environment)

import numpy as np

import pandas as pd

np.random.seed(42)From Prediction to Causation

Machine learning excels at prediction: minimizing \(\mathbb{E}[(Y - \hat{f}(X))^2]\). But economists care about causation: what happens to \(Y\) if we intervene on \(X\)?

| Goal | Question | Method |

|---|---|---|

| Prediction | What is \(\hat{y}\) given \(x\)? | Random forest, neural net, boosting |

| Causation | What happens to \(y\) if we change \(x\)? | Experiments, IV, DiD, RDD |

NoteThe Causal ML Revolution

Recent methods—causal forests, double ML, meta-learners—combine ML’s flexibility for high-dimensional data with causal inference’s focus on identification (Athey and Imbens 2019). The key insight: use ML for nuisance parameters (propensity scores, outcome models) while preserving valid causal inference. Key methodological foundations include causal forests (Wager and Athey 2018) and double/debiased ML (Chernozhukov et al. 2018).

Key Papers

| Paper | Contribution |

|---|---|

| Athey & Imbens (2016) | Recursive partitioning for heterogeneous causal effects |

| Wager & Athey (2018) | Causal forests with valid asymptotic inference |

| Chernozhukov et al. (2018) | Double/Debiased ML for high-dimensional controls |

| Künzel et al. (2019) | Meta-learners (X-learner) for CATE |

| Athey & Wager (2021) | Policy learning with observational data |

The Potential Outcomes Framework

Setup

For each unit \(i\):

- Treatment: \(W_i \in \{0, 1\}\)

- Potential outcomes: \(Y_i(0), Y_i(1)\) — what would happen under control/treatment

- Observed outcome: \(Y_i = W_i \cdot Y_i(1) + (1 - W_i) \cdot Y_i(0)\)

- Covariates: \(X_i\) (pre-treatment characteristics)

Treatment Effects Taxonomy

| Estimand | Definition | Interpretation |

|---|---|---|

| ITE | \(\tau_i = Y_i(1) - Y_i(0)\) | Individual effect (unobservable) |

| CATE | \(\tau(x) = \mathbb{E}[Y(1) - Y(0) \mid X = x]\) | Conditional average effect |

| ATE | \(\mathbb{E}[\tau_i]\) | Average treatment effect |

| ATT | \(\mathbb{E}[\tau_i \mid W_i = 1]\) | Effect on the treated |

The Fundamental Problem of Causal Inference

We observe either \(Y_i(1)\) OR \(Y_i(0)\), never both. The individual treatment effect \(\tau_i\) is fundamentally unidentifiable.

Solution: Under unconfoundedness (selection on observables): \[ (Y_i(0), Y_i(1)) \perp\!\!\!\perp W_i \mid X_i \]

Plus overlap (positivity): \(0 < P(W_i = 1 \mid X_i = x) < 1\) for all \(x\).

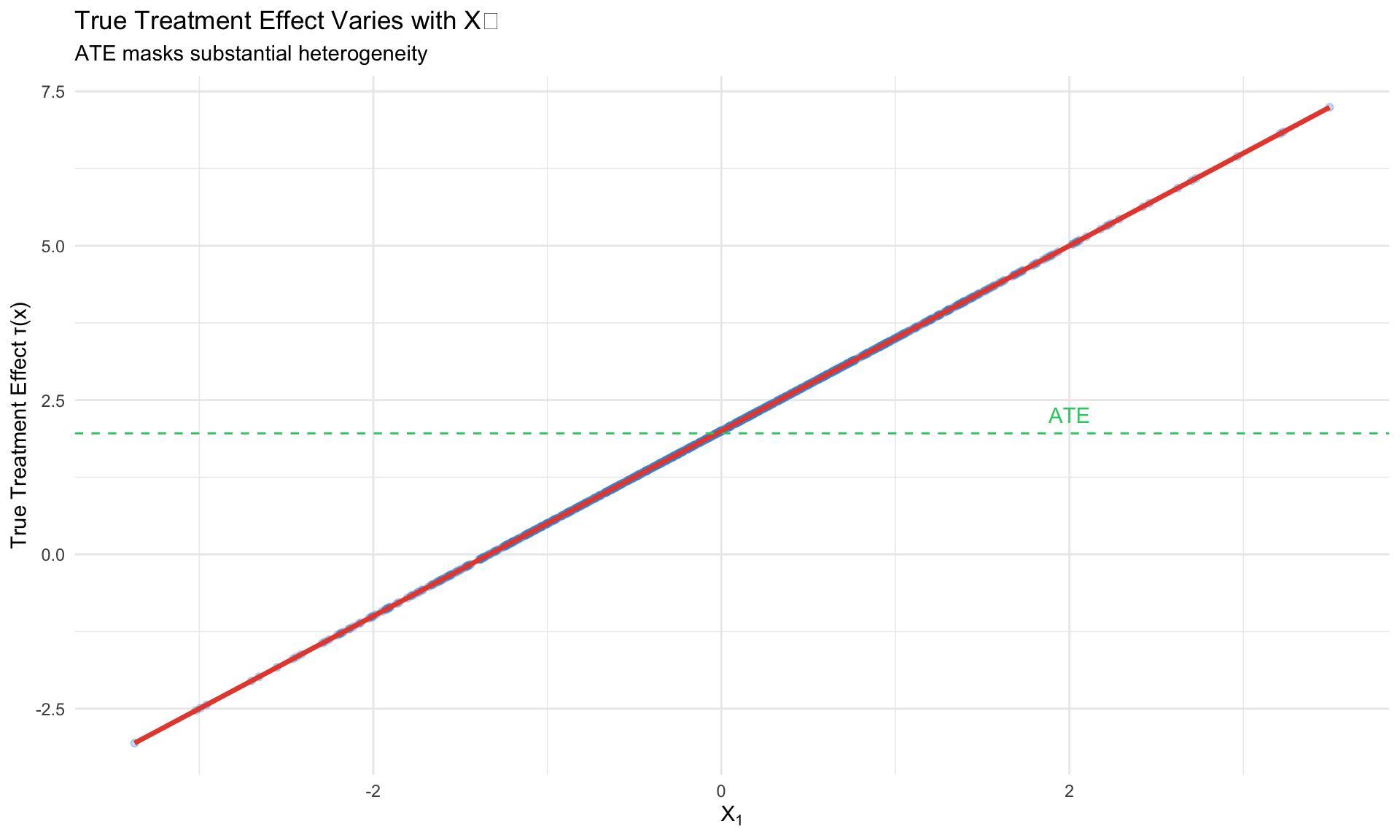

Heterogeneous Treatment Effects

Why Heterogeneity Matters

The ATE \(= 2\) could mask:

- Subgroup A: \(\tau = 5\) (strong benefit)

- Subgroup B: \(\tau = -1\) (harm)

Understanding heterogeneity enables:

- Targeting: Treat those who benefit most

- Mechanism identification: What drives variation?

- Policy optimization: Maximize welfare under constraints

Traditional Approaches and Their Limitations

Subgroup analysis: Pre-specify groups, estimate effects within each.

- Problem: Many possible subgroups → multiple testing

- Problem: Boundaries are arbitrary

Interaction terms: \(Y = \alpha + \tau W + \gamma W \cdot X + \beta X + \varepsilon\)

- Problem: Must specify functional form

- Problem: Doesn’t scale to many \(X\)

Causal ML: Learn \(\tau(x)\) flexibly from data with valid inference.

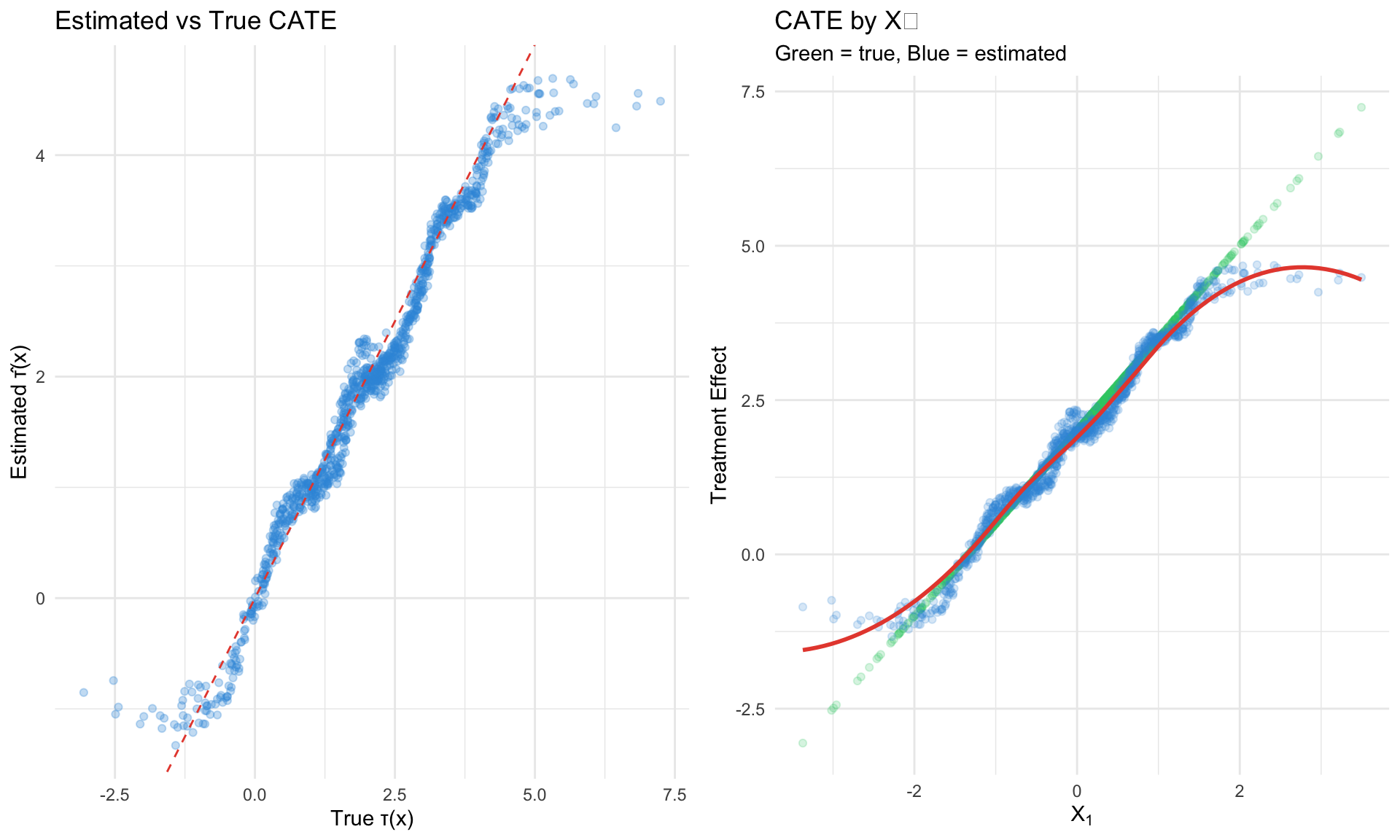

Causal Forests

The Key Idea (Wager & Athey 2018)

Adapt random forests from predicting \(\mathbb{E}[Y|X]\) to predicting \(\tau(x) = \mathbb{E}[Y(1) - Y(0)|X=x]\).

Key innovations:

- Honest splitting: Separate samples for tree structure vs. leaf estimation

- Heterogeneity-maximizing splits: Split to maximize treatment effect variation

- Valid inference: Asymptotic normality of estimates

Algorithm

For each tree \(b = 1, \ldots, B\):

- Subsample data into tree-building (\(\mathcal{I}_1\)) and estimation (\(\mathcal{I}_2\)) sets

- Build tree on \(\mathcal{I}_1\): at each node, find split maximizing heterogeneity

- Estimate leaf effects using \(\mathcal{I}_2\) only (honesty)

- Aggregate: \(\hat{\tau}(x) = \frac{1}{B} \sum_b \hat{\tau}_b(x)\)

R Implementation with grf

Key grf Functions

library(grf)

# Fit causal forest

cf <- causal_forest(X, Y, W, num.trees = 2000)

# Point predictions

tau_hat <- predict(cf)$predictions

# Predictions with variance (for CIs)

tau_ci <- predict(cf, estimate.variance = TRUE)

lower <- tau_ci$predictions - 1.96 * sqrt(tau_ci$variance.estimates)

upper <- tau_ci$predictions + 1.96 * sqrt(tau_ci$variance.estimates)

# Average treatment effect with SE

ate <- average_treatment_effect(cf, target.sample = "all")

cat("ATE:", ate[1], "SE:", ate[2], "\n")

# ATT

att <- average_treatment_effect(cf, target.sample = "treated")

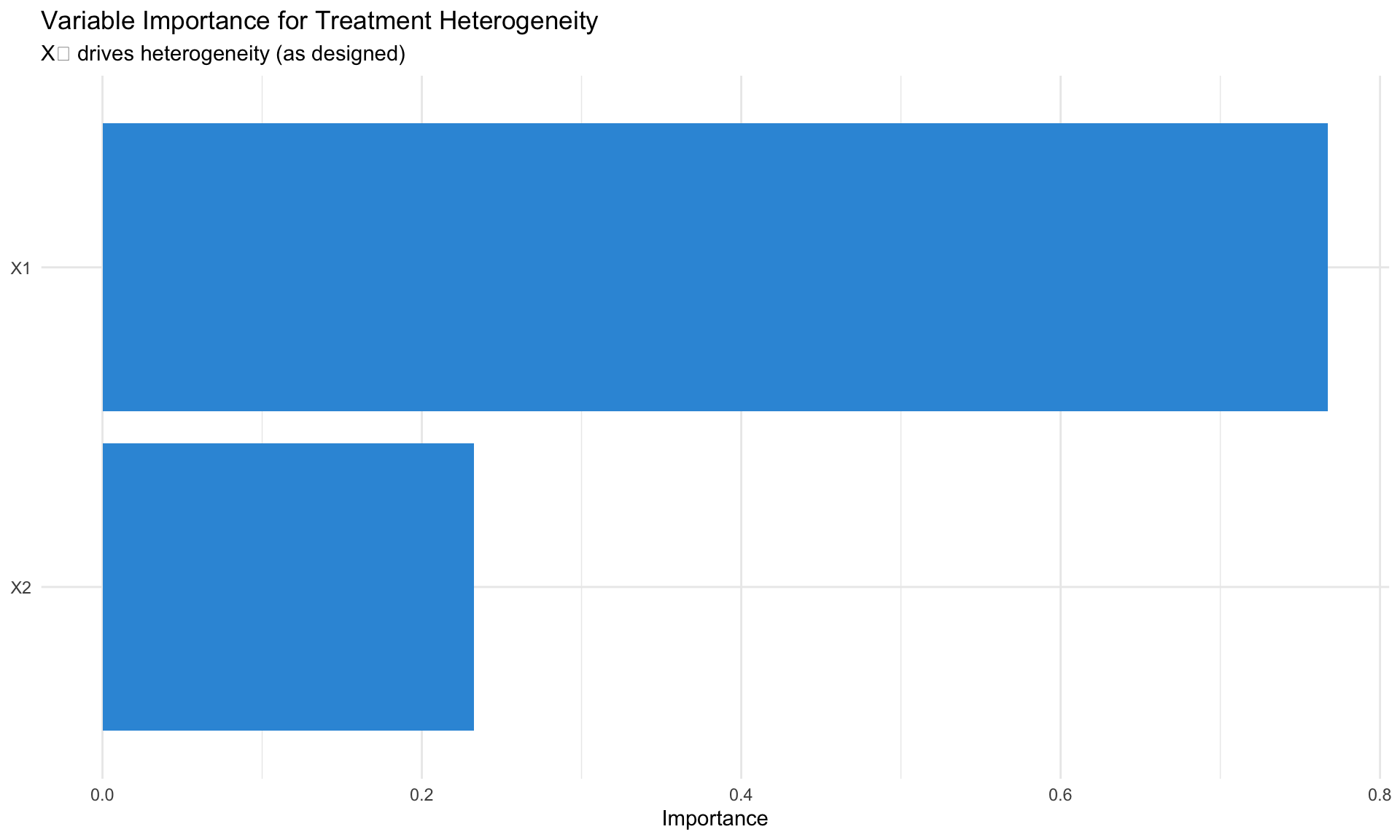

# Variable importance: which X drive heterogeneity?

vi <- variable_importance(cf)

# Best linear projection: linear approximation of τ(x)

blp <- best_linear_projection(cf, X)

# Calibration test: is there heterogeneity?

test_calibration(cf)Variable Importance

Which covariates drive treatment effect heterogeneity?

Observational Data: Pre-Estimated Nuisance Functions

For observational studies, pre-fit propensity and outcome models:

# Pre-fit nuisance models (recommended for observational data)

W.hat <- predict(regression_forest(X, W))$predictions # propensity

Y.hat <- predict(regression_forest(X, Y))$predictions # outcome

# Causal forest with pre-estimated nuisance

cf_obs <- causal_forest(X, Y, W, W.hat = W.hat, Y.hat = Y.hat)Double/Debiased Machine Learning

The Problem

When using ML for nuisance parameters (propensity score, outcome model), regularization introduces bias that invalidates standard inference.

Example: LASSO shrinks coefficients → biased treatment effect → invalid t-statistics.

The Solution (Chernozhukov et al. 2018)

Two key ingredients:

- Cross-fitting: Train ML on fold \(-k\), predict on fold \(k\)

- Neyman orthogonality: Use score function robust to nuisance estimation error

Partially Linear Model

\[ Y = \theta D + g(X) + U, \quad \mathbb{E}[U|X,D] = 0 \] \[ D = m(X) + V, \quad \mathbb{E}[V|X] = 0 \]

Target: \(\theta\) (treatment effect)

Nuisance: \(g(X)\) (outcome confounding), \(m(X)\) (propensity/treatment model)

The Algorithm

- Split data into \(K\) folds (typically \(K = 5\))

- For each fold \(k\):

- Train \(\hat{g}_{-k}(X)\) and \(\hat{m}_{-k}(X)\) on all other folds

- Compute residuals on fold \(k\):

- \(\tilde{Y}_i = Y_i - \hat{g}_{-k}(X_i)\)

- \(\tilde{D}_i = D_i - \hat{m}_{-k}(X_i)\)

- Estimate: \(\hat{\theta} = \frac{\sum_i \tilde{D}_i \tilde{Y}_i}{\sum_i \tilde{D}_i^2}\)

- Standard error: standard OLS formula on residualized data

Why It Works: Orthogonality

The orthogonal moment condition: \[ \psi(W; \theta, \eta) = (Y - g(X) - \theta D)(D - m(X)) \]

has the property that small errors in \(\hat{g}, \hat{m}\) don’t bias \(\hat{\theta}\): \[ \frac{\partial}{\partial \eta} \mathbb{E}[\psi(W; \theta_0, \eta)] \bigg|_{\eta = \eta_0} = 0 \]

Python Implementation with doubleml

# Double ML estimation in Python

from sklearn.ensemble import RandomForestRegressor

from sklearn.model_selection import cross_val_predict

import warnings

warnings.filterwarnings('ignore')

# Simulate data

n = 2000

p = 10

X = np.random.randn(n, p)

theta_true = 0.5 # true treatment effect

D = X[:, 0] + 0.5 * X[:, 1] + np.random.randn(n) # treatment depends on X

Y = theta_true * D + X[:, 0] + X[:, 1] + np.random.randn(n) # outcome

# Manual Double ML

def double_ml_plr(Y, D, X, K=5):

"""

Double ML for Partially Linear Regression

Y = theta * D + g(X) + U

D = m(X) + V

"""

n = len(Y)

# Cross-fitted predictions

g_hat = cross_val_predict(

RandomForestRegressor(n_estimators=100, max_depth=5, random_state=42),

X, Y, cv=K

)

m_hat = cross_val_predict(

RandomForestRegressor(n_estimators=100, max_depth=5, random_state=42),

X, D, cv=K

)

# Residualize

Y_tilde = Y - g_hat

D_tilde = D - m_hat

# Estimate theta

theta_hat = np.sum(D_tilde * Y_tilde) / np.sum(D_tilde ** 2)

# Standard error

residuals = Y_tilde - theta_hat * D_tilde

se_hat = np.sqrt(np.sum(residuals ** 2 * D_tilde ** 2) / (np.sum(D_tilde ** 2) ** 2))

return {

'estimate': theta_hat,

'se': se_hat,

'ci_lower': theta_hat - 1.96 * se_hat,

'ci_upper': theta_hat + 1.96 * se_hat

}

# Run Double ML

result = double_ml_plr(Y, D, X)

print(f"True θ: {theta_true}")

print(f"Double ML estimate: {result['estimate']:.4f}")

print(f"Standard error: {result['se']:.4f}")

print(f"95% CI: [{result['ci_lower']:.4f}, {result['ci_upper']:.4f}]")Using the DoubleML Package

from doubleml import DoubleMLPLR, DoubleMLData

from sklearn.ensemble import RandomForestRegressor

# Create data object

df = pd.DataFrame(X, columns=[f'X{i}' for i in range(p)])

df['Y'] = Y

df['D'] = D

dml_data = DoubleMLData(

df, y_col='Y', d_cols='D',

x_cols=[f'X{i}' for i in range(p)]

)

# Specify learners

ml_l = RandomForestRegressor(n_estimators=500, max_depth=5)

ml_m = RandomForestRegressor(n_estimators=500, max_depth=5)

# Fit

dml_plr = DoubleMLPLR(dml_data, ml_l, ml_m, n_folds=5)

dml_plr.fit()

print(dml_plr.summary)R Implementation

Double ML ATE: 1.864 SE: 0.084 True ATE: 1.961 95% CI: [ 1.699 , 2.029 ]Meta-Learners

Overview

Meta-learners are strategies for combining base ML models to estimate CATE.

T-Learner (Two Models)

Train separate models for treatment and control:

\[ \hat{\tau}(x) = \hat{\mu}_1(x) - \hat{\mu}_0(x) \]

# T-Learner implementation

from sklearn.ensemble import RandomForestRegressor

# Binary treatment simulation

n = 1000

X_sim = np.random.randn(n, 5)

W_sim = np.random.binomial(1, 0.5, n)

tau_sim = X_sim[:, 0] + 0.5 * X_sim[:, 1]

Y_sim = tau_sim * W_sim + X_sim[:, 0] + np.random.randn(n)

# T-Learner: separate models for treatment and control

model_0 = RandomForestRegressor(n_estimators=100, random_state=42)

model_1 = RandomForestRegressor(n_estimators=100, random_state=42)

model_0.fit(X_sim[W_sim == 0], Y_sim[W_sim == 0])

model_1.fit(X_sim[W_sim == 1], Y_sim[W_sim == 1])

tau_t = model_1.predict(X_sim) - model_0.predict(X_sim)

print(f"T-Learner correlation with true τ: {np.corrcoef(tau_sim, tau_t)[0,1]:.3f}")Pros: Simple, no propensity needed

Cons: High variance, especially with imbalanced treatment

S-Learner (Single Model)

Single model with treatment as feature:

\[ \hat{\mu}(x, w) \rightarrow \hat{\tau}(x) = \hat{\mu}(x, 1) - \hat{\mu}(x, 0) \]

# S-Learner: single model with treatment as feature

X_aug = np.column_stack([X_sim, W_sim])

model_s = RandomForestRegressor(n_estimators=100, random_state=42)

model_s.fit(X_aug, Y_sim)

# Predict under treatment and control

tau_s = (model_s.predict(np.column_stack([X_sim, np.ones(n)])) -

model_s.predict(np.column_stack([X_sim, np.zeros(n)])))

print(f"S-Learner correlation with true τ: {np.corrcoef(tau_sim, tau_s)[0,1]:.3f}")Pros: Simple, regularization shared

Cons: Treatment effect can be shrunk to zero

X-Learner (Künzel et al. 2019)

Best for imbalanced treatment (few treated or few controls):

- Fit \(\hat{\mu}_0, \hat{\mu}_1\) (T-learner)

- Impute treatment effects:

- Treated: \(\tilde{D}_1 = Y_1 - \hat{\mu}_0(X_1)\)

- Control: \(\tilde{D}_0 = \hat{\mu}_1(X_0) - Y_0\)

- Fit models: \(\hat{\tau}_0(x), \hat{\tau}_1(x)\)

- Combine: \(\hat{\tau}(x) = e(x) \hat{\tau}_0(x) + (1-e(x)) \hat{\tau}_1(x)\)

Comparison

| Learner | Best When | Weakness |

|---|---|---|

| T-Learner | Balanced, large samples | High variance |

| S-Learner | Small effects, regularization needed | Shrinks effects |

| X-Learner | Imbalanced treatment | Complex, needs propensity |

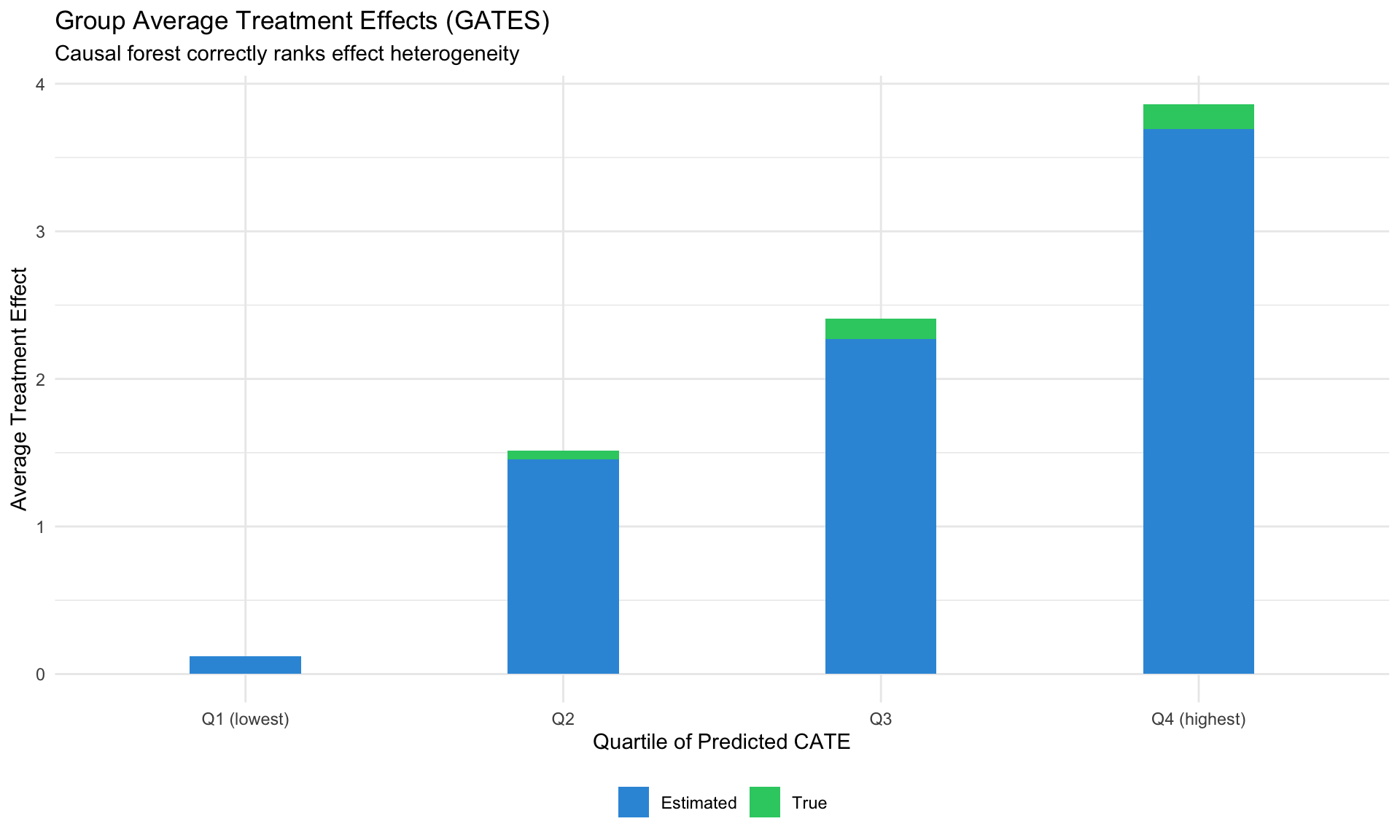

Group Average Treatment Effects (GATES)

Evaluating Heterogeneity

GATES groups units by predicted CATE and estimates average effects within each group:

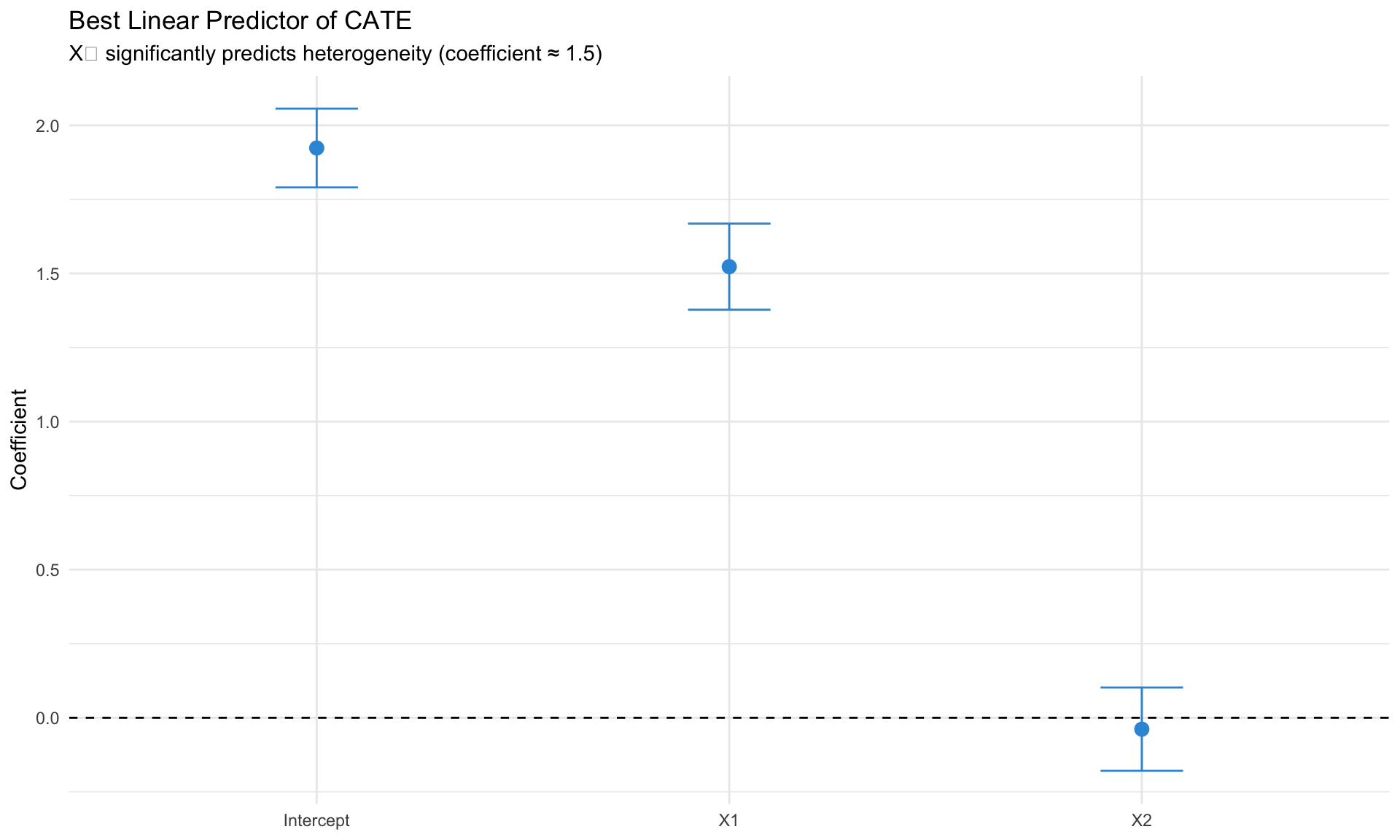

Best Linear Predictor (BLP)

Which covariates explain heterogeneity?

Best linear projection of the conditional average treatment effect.

Confidence intervals are cluster- and heteroskedasticity-robust (HC3):

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.923589 0.067767 28.3853 <2e-16 ***

X1 1.522921 0.074177 20.5308 <2e-16 ***

X2 -0.038501 0.071713 -0.5369 0.5915

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

EconML: Microsoft’s Causal ML Toolkit

Overview

EconML provides a unified API for heterogeneous treatment effect estimation in Python.

Key Estimators

| Estimator | Description |

|---|---|

LinearDML |

DML with linear final stage |

CausalForestDML |

Causal forest with DML |

ForestDRLearner |

Doubly robust forest |

OrthoIV |

Orthogonal IV learner |

DynamicDML |

Panel data |

Python Implementation

# EconML example

from econml.dml import LinearDML, CausalForestDML

from sklearn.ensemble import RandomForestRegressor, RandomForestClassifier

# Setup

X_hetero = X_sim[:, :3] # features for heterogeneity

W_confound = X_sim[:, 3:] # confounders

# LinearDML

est_linear = LinearDML(

model_y=RandomForestRegressor(n_estimators=100),

model_t=RandomForestClassifier(n_estimators=100),

cv=5

)

est_linear.fit(Y_sim, W_sim, X=X_hetero, W=W_confound)

# Effects

tau_linear = est_linear.effect(X_hetero)

# Inference

tau_lower, tau_upper = est_linear.effect_interval(X_hetero, alpha=0.05)

# Summary

print(est_linear.summary())Unified API Pattern

All EconML estimators follow:

est.fit(Y, T, X=X, W=W) # fit (Y=outcome, T=treatment, X=hetero, W=confound)

est.effect(X_test) # point estimates

est.effect_interval(X_test) # confidence intervals

est.summary() # inference summaryApplications in Macroeconomics

Heterogeneous Policy Effects

Question: How do monetary policy effects vary across firms/regions/time?

Approach:

- Identify policy shocks (high-frequency, narrative)

- Estimate heterogeneous effects using causal forests

- Characterize which observables predict sensitivity

Example: Cross-Country Monetary Transmission

# Do bank holdings predict constrained monetary response?

cf_policy <- causal_forest(

X = cbind(bank_holdings, cbi_index, debt_gdp, trade_openness),

Y = delta_inflation,

W = tightening_dummy

)

# Which characteristics drive heterogeneity?

variable_importance(cf_policy)

# Linear approximation

best_linear_projection(cf_policy,

cbind(bank_holdings, cbi_index, debt_gdp))Fiscal Multiplier Heterogeneity

Do fiscal multipliers vary by:

- Slack (output gap)?

- Monetary policy stance (ZLB)?

- Debt levels?

Causal forests can flexibly estimate: \[ \text{Multiplier}(x) = \mathbb{E}[\Delta Y \mid \text{Fiscal shock}, X = x] \]

Practical Considerations

Sample Size Requirements

| Method | Minimum N | Recommended N |

|---|---|---|

| ATE (Double ML) | 200 | 500+ |

| CATE (Causal Forest) | 500 | 2000+ |

| GATES | 1000 | 3000+ |

| Variable Importance | 2000 | 5000+ |

Diagnostics

Overlap Check

# Propensity score distribution

e_hat <- cf$W.hat

hist(e_hat, breaks = 50, main = "Propensity Scores")

abline(v = c(0.1, 0.9), col = "red", lty = 2)

# Extreme values

cat("Extreme propensity:", mean(e_hat < 0.1 | e_hat > 0.9) * 100, "%\n")Calibration Test

# Is there actually heterogeneity?

test_calibration(cf)

# Look for significant "differential.forest.prediction"AUTOC (Targeting Quality)

# Area Under the TOC Curve

rate <- rank_average_treatment_effect(cf, X[, 1])

print(rate) # CI should exclude 0Common Pitfalls

- Causal ML doesn’t solve identification: Still need unconfoundedness

- Overfitting CATE: Use honest forests, cross-validation

- Noise as heterogeneity: Run calibration tests

- Overlap violations: Check propensity scores, trim extremes

- Small samples: CATE unreliable with N < 500

Summary

| Method | Purpose | Package |

|---|---|---|

| Causal Forest | Heterogeneous treatment effects | grf (R) |

| Double ML | ATE with high-dimensional controls | DoubleML (Python/R) |

| EconML | Unified CATE estimation | econml (Python) |

| Meta-Learners | T/S/X strategies for CATE | Various |

TipFor Macro Applications

- Sample sizes matter: Cross-country panels may be too small for CATE

- Identification first: Causal ML requires the same assumptions as traditional methods

- Focus on BLP and GATES: Which characteristics predict heterogeneity?

- Aggregation concerns: Individual effects may aggregate differently at macro level

Key References

Foundational

- Athey & Imbens (2016) “Recursive Partitioning for Heterogeneous Causal Effects” PNAS

- Wager & Athey (2018) “Estimation and Inference of Heterogeneous Treatment Effects using Random Forests” JASA

- Chernozhukov et al. (2018) “Double/Debiased Machine Learning” Econometrics Journal

Extensions

- Künzel et al. (2019) “Metalearners for Heterogeneous Treatment Effects” PNAS

- Athey & Wager (2021) “Policy Learning with Observational Data” Econometrica

- Kennedy (2022) “Optimal Doubly Robust Estimation of Heterogeneous Causal Effects”

Resources

- Causal ML Book: https://causalml-book.org/

- ML for Economists: https://github.com/ml4econ/lecture-notes-2025

- grf Documentation: https://grf-labs.github.io/grf/

- EconML: https://github.com/py-why/EconML

- DoubleML: https://github.com/DoubleML/doubleml-for-py