DSGE Estimation

The Kalman Filter, Bayesian Methods, and Model Comparison

From Model to Data

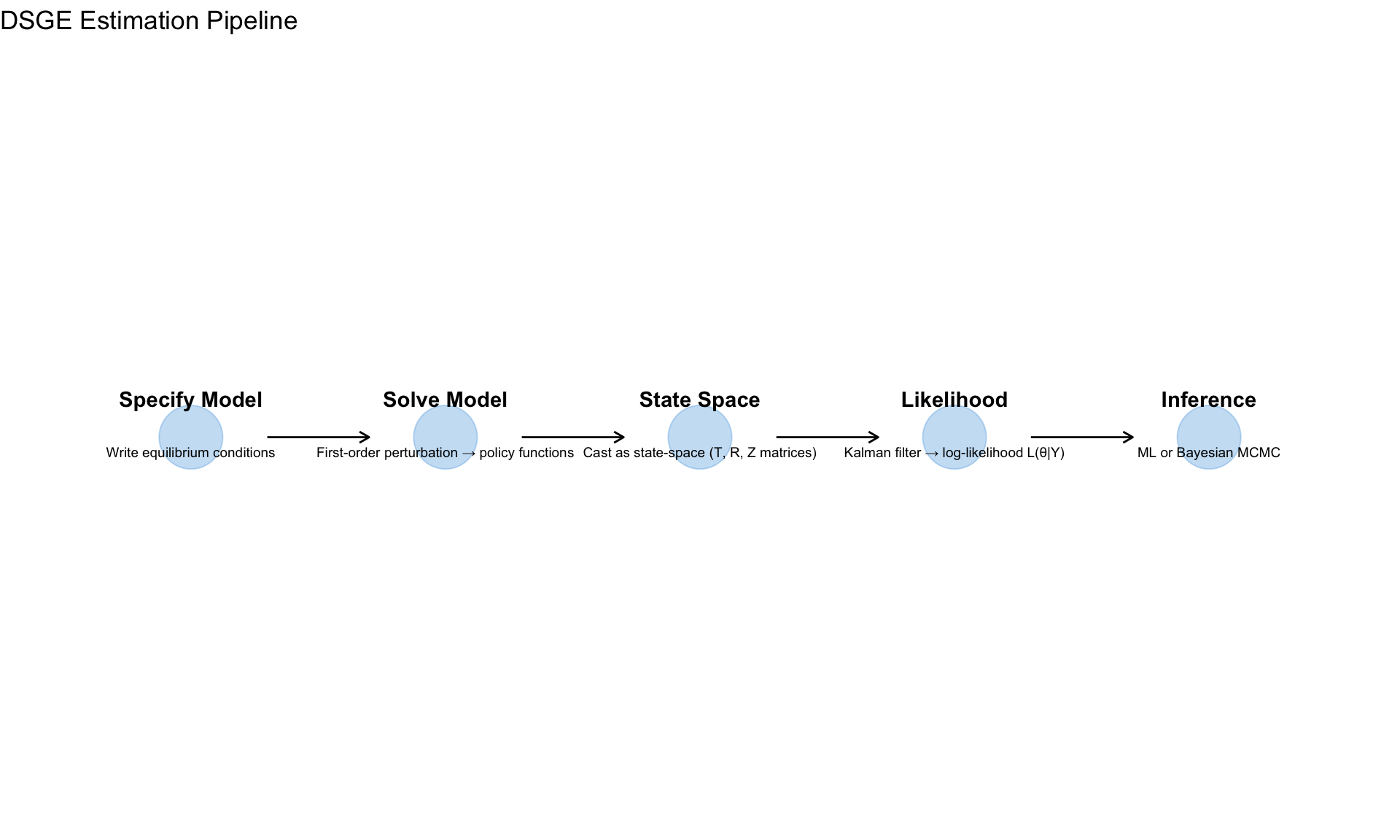

Module 10 showed how to solve DSGE models. Now we estimate them—finding parameter values that make the model consistent with observed data.

NoteThe Estimation Challenge

DSGE models have latent states (unobserved variables like potential output, natural rate) that we must infer while simultaneously estimating parameters.

The Workflow

State Space Representation

After solving the DSGE model (Module 10), we have:

\[ \hat{y}_t = G_x \hat{y}_{t-1} + G_u u_t \]

This is the transition equation. We add an observation equation linking model states to observables:

The State Space Form

\[ \underbrace{s_t = T s_{t-1} + R \eta_t}_{\text{Transition}} \quad \eta_t \sim N(0, Q) \]

\[ \underbrace{y_t = Z s_t + d + \varepsilon_t}_{\text{Observation}} \quad \varepsilon_t \sim N(0, H) \]

| Component | Meaning | From DSGE |

|---|---|---|

| \(s_t\) | State vector (all model variables) | Solution states |

| \(T\) | Transition matrix | \(G_x\) from perturbation |

| \(R\) | Shock impact | \(G_u\) from perturbation |

| \(Q\) | Shock variance-covariance | \(\text{diag}(\sigma_1^2, \ldots, \sigma_k^2)\) |

| \(y_t\) | Observables (data) | GDP growth, inflation, rate |

| \(Z\) | Selection/mapping matrix | Which states are observed |

| \(H\) | Measurement error variance | Often zero or small |

Example: 3-Variable NK Model

Observables: \(y_t = (\Delta \log Y_t, \pi_t, i_t)'\)

States: \(s_t = (\hat{y}_t, \hat{\pi}_t, \hat{i}_t, \hat{a}_t, \hat{\varepsilon}^m_t)'\)

Mapping: \[ Z = \begin{pmatrix} 1 & 0 & 0 & 0 & 0 \\ 0 & 1 & 0 & 0 & 0 \\ 0 & 0 & 1 & 0 & 0 \end{pmatrix} \]

The first three states are directly observed (up to measurement error).

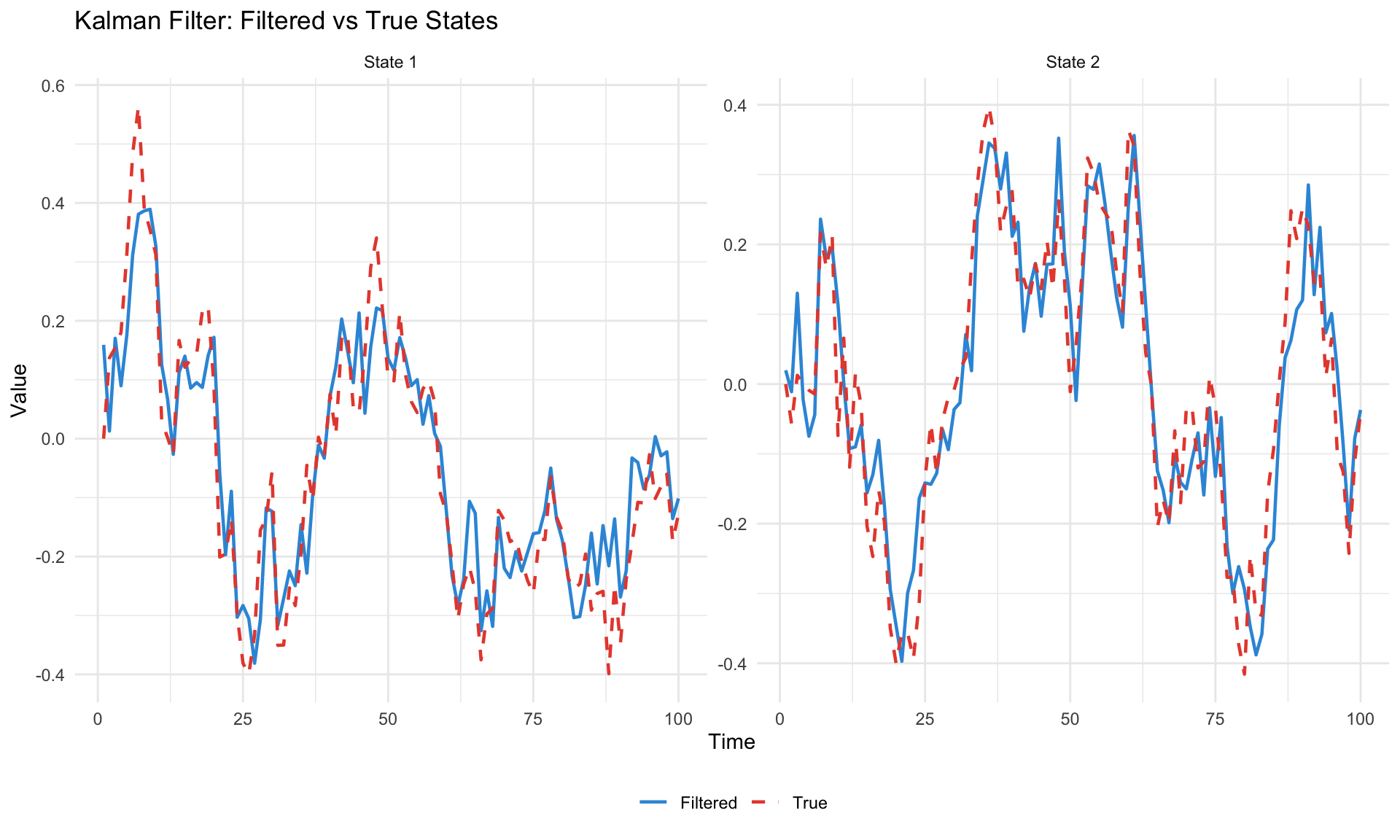

The Kalman Filter

The Kalman filter recursively computes the likelihood \(L(\theta | Y)\) where \(\theta\) are the DSGE parameters.

The Algorithm

For each time period \(t = 1, \ldots, T\):

Step 1: Prediction

Given information up to \(t-1\): \[ s_{t|t-1} = T s_{t-1|t-1} \] \[ P_{t|t-1} = T P_{t-1|t-1} T' + R Q R' \]

where \(P_{t|t-1}\) is the variance of the state forecast.

Step 2: Innovation

Compare prediction to actual observation: \[ v_t = y_t - Z s_{t|t-1} - d \] \[ F_t = Z P_{t|t-1} Z' + H \]

\(v_t\) is the forecast error and \(F_t\) is its variance.

Step 3: Update

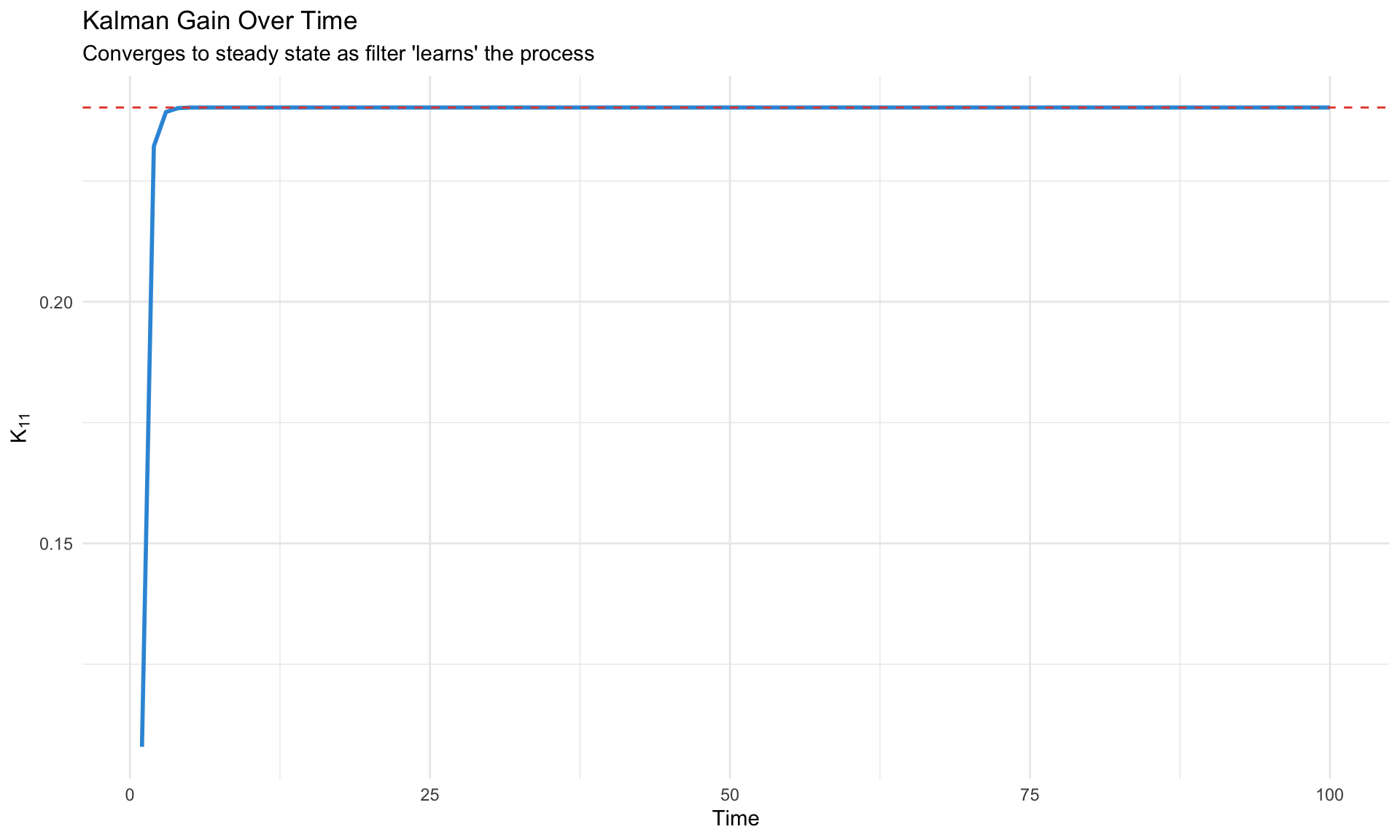

Incorporate new observation: \[ K_t = P_{t|t-1} Z' F_t^{-1} \] \[ s_{t|t} = s_{t|t-1} + K_t v_t \] \[ P_{t|t} = (I - K_t Z) P_{t|t-1} \]

\(K_t\) is the Kalman gain—how much to adjust the state given the forecast error.

Step 4: Likelihood Contribution

\[ \log L_t = -\frac{n_y}{2} \log(2\pi) - \frac{1}{2} \log|F_t| - \frac{1}{2} v_t' F_t^{-1} v_t \]

Total log-likelihood: \[ \log L(\theta | Y) = \sum_{t=1}^{T} \log L_t \]

Kalman Gain Intuition

The Kalman gain \(K_t\) balances:

- Model confidence (small \(P_{t|t-1}\)) → trust the prediction, small \(K_t\)

- Observation precision (small \(H\)) → trust the data, large \(K_t\)

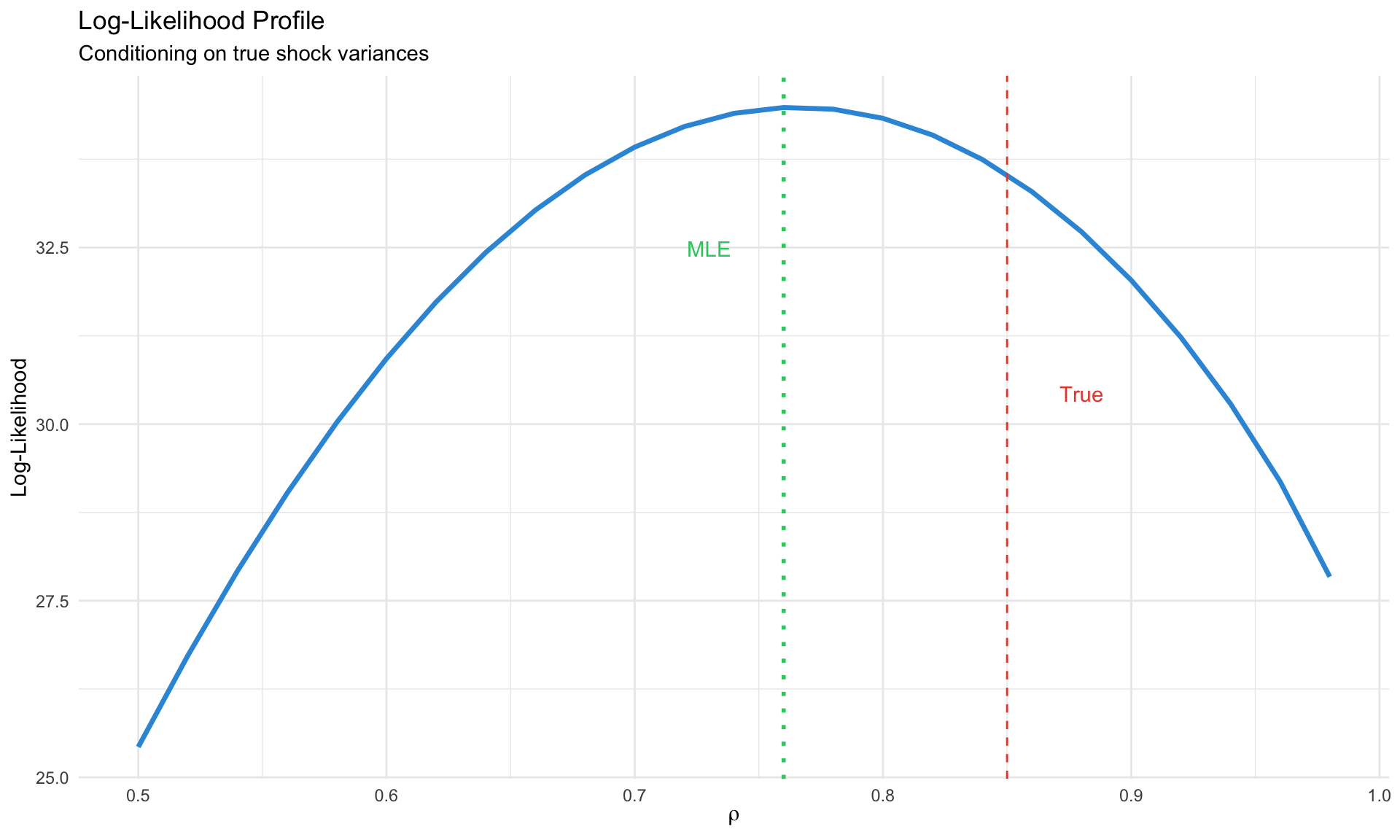

Maximum Likelihood Estimation

Given the Kalman filter likelihood, we can maximize:

\[ \hat{\theta}_{ML} = \arg\max_\theta \log L(\theta | Y) \]

The Challenge

For each candidate \(\theta\):

- Solve the DSGE → get \(T(\theta), R(\theta)\)

- Run Kalman filter → get \(\log L(\theta | Y)\)

This is computationally expensive. Gradient-free optimizers (Nelder-Mead, simulated annealing) or specialized methods (csminwel) are common.

Standard Errors

At the MLE, compute the Hessian (matrix of second derivatives):

\[ \hat{V}(\hat{\theta}) = -H^{-1}, \quad H_{ij} = \frac{\partial^2 \log L}{\partial \theta_i \partial \theta_j}\bigg|_{\hat{\theta}} \]

Standard errors: \(\text{SE}(\hat{\theta}_j) = \sqrt{\hat{V}_{jj}}\)

Bayesian Estimation

The Bayesian approach combines prior beliefs with data:

\[ \underbrace{p(\theta | Y)}_{\text{posterior}} \propto \underbrace{L(Y | \theta)}_{\text{likelihood}} \times \underbrace{p(\theta)}_{\text{prior}} \]

Why Bayesian for DSGE?

| Advantage | Explanation |

|---|---|

| Regularization | Priors prevent extreme/implausible estimates |

| Identification | Informative priors help weakly identified parameters |

| Full uncertainty | Posterior distribution, not just point estimate |

| Model comparison | Marginal likelihood is natural Bayesian output |

| Small samples | Works well with limited macro data |

Prior Selection

Priors should reflect economic knowledge without being too restrictive.

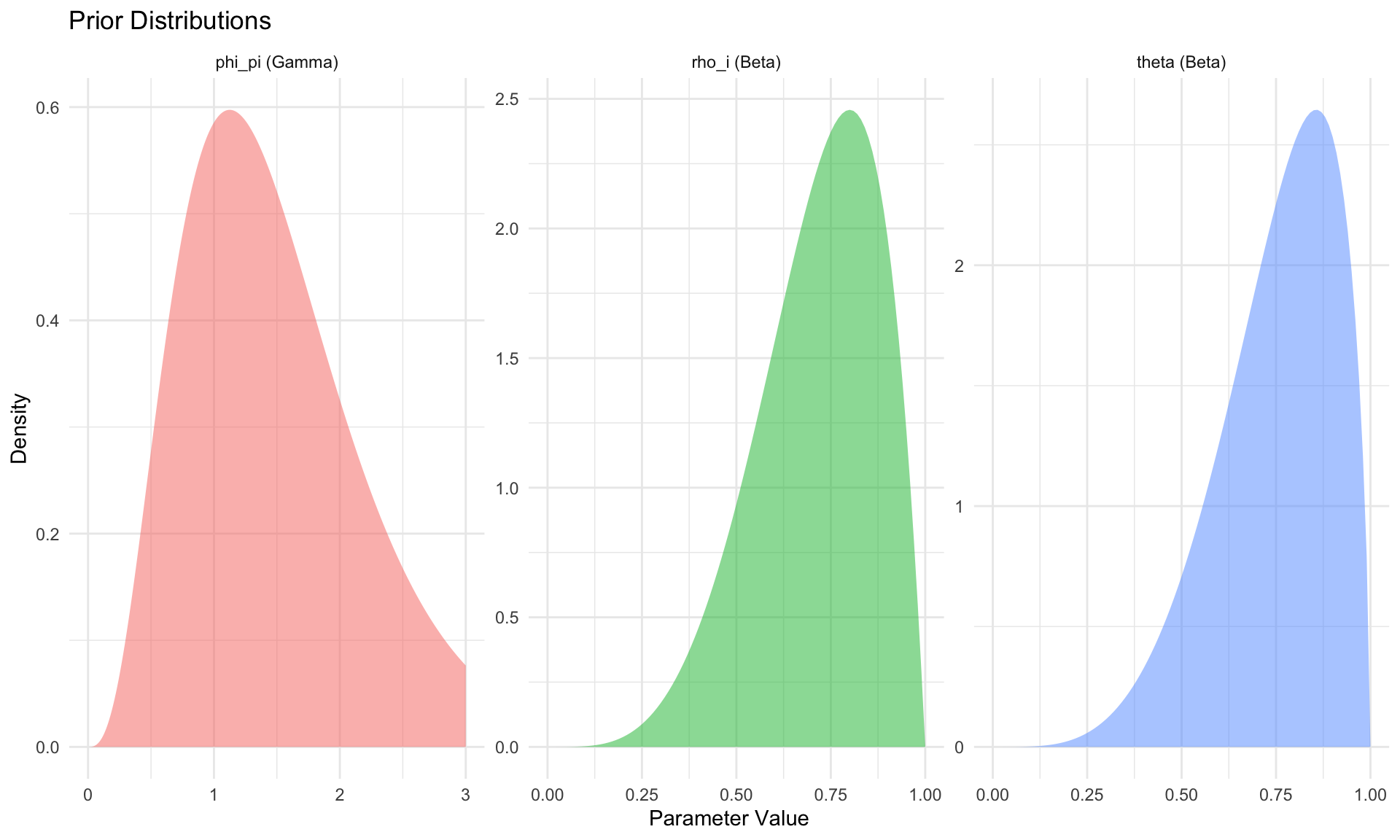

Standard Prior Distributions

| Parameter Type | Distribution | Rationale |

|---|---|---|

| Persistence (\(\rho\)) | Beta(a, b) | Bounded [0, 1] |

| Elasticities | Gamma(a, b) | Positive, right-skewed |

| Fractions (\(\alpha, \theta\)) | Beta(a, b) | Bounded [0, 1] |

| Shock std (\(\sigma\)) | Inv-Gamma(s, \(\nu\)) | Positive, proper |

| Policy weights (\(\phi_\pi\)) | Gamma or Normal | Positive or unrestricted |

| Discount factor (\(\beta\)) | Beta near 0.99 | Close to 1 |

Example: NK Model Priors

| Parameter | Distribution | Mean | SD | Interpretation |

|---|---|---|---|---|

| \(\beta\) | Beta | 0.9900 | 0.002 | Discount factor |

| \(\sigma\) | Gamma | 1.5000 | 0.250 | Risk aversion |

| \(\phi\) | Gamma | 2.0000 | 0.500 | Frisch elasticity |

| \(\theta\) | Beta | 0.7500 | 0.100 | Calvo parameter |

| \(\phi_\pi\) | Gamma | 1.5000 | 0.250 | Taylor: inflation |

| \(\phi_y\) | Gamma | 0.1250 | 0.050 | Taylor: output |

| \(\rho_i\) | Beta | 0.8000 | 0.100 | Rate smoothing |

| \(\rho_a\) | Beta | 0.9000 | 0.050 | Tech persistence |

| \(\sigma_a\) | Inv-Gamma | 0.0100 | 2.000 | Tech shock std |

| \(\sigma_m\) | Inv-Gamma | 0.0025 | 2.000 | MP shock std |

Metropolis-Hastings MCMC

The posterior \(p(\theta | Y)\) is rarely available analytically. We use Markov Chain Monte Carlo (MCMC) to sample from it.

The Algorithm

Initialize: Start at some \(\theta^{(0)}\) (often the posterior mode)

Propose: Draw candidate \(\theta^* \sim q(\theta^* | \theta^{(g)})\)

- Common: Random walk \(\theta^* = \theta^{(g)} + \varepsilon\), \(\varepsilon \sim N(0, c \cdot \Sigma)\)

- \(\Sigma\) = inverse Hessian at mode; \(c\) = scaling factor

Accept/Reject: \[ \alpha = \min\left(1, \frac{p(\theta^* | Y)}{p(\theta^{(g)} | Y)}\right) = \min\left(1, \frac{L(Y|\theta^*) p(\theta^*)}{L(Y|\theta^{(g)}) p(\theta^{(g)})}\right) \]

- Draw \(u \sim \text{Uniform}(0, 1)\)

- If \(u < \alpha\): accept \(\theta^{(g+1)} = \theta^*\)

- Else: reject \(\theta^{(g+1)} = \theta^{(g)}\)

Repeat for \(G\) draws; discard first \(B\) as burn-in

Acceptance rate: 0.793

Tuning the Proposal

Target acceptance rate: 20-30% for random walk MH

| Acceptance Rate | Diagnosis | Action |

|---|---|---|

| < 10% | Proposals too bold | Decrease \(c\) |

| 20-30% | Optimal | Keep |

| > 50% | Proposals too timid | Increase \(c\) |

Dynare’s mh_jscale parameter controls this.

Dynare Estimation

Dynare automates DSGE estimation with the estimation command.

Complete Example: 3-Equation NK Model

%% nk_estimation.mod

%% Preamble

var y pi i a eps_m;

varexo eta_a eta_m;

parameters BETA SIGMA KAPPA PHI_PI PHI_Y RHO_I RHO_A;

%% Calibrated parameters

BETA = 0.99;

SIGMA = 1;

%% Model

model(linear);

% IS curve

y = y(+1) - (1/SIGMA) * (i - pi(+1));

% Phillips curve

pi = BETA * pi(+1) + KAPPA * y;

% Taylor rule

i = RHO_I * i(-1) + (1 - RHO_I) * (PHI_PI * pi + PHI_Y * y) + eps_m;

% Shocks

a = RHO_A * a(-1) + eta_a; % technology (affects natural rate)

eps_m = eta_m; % monetary policy

end;

%% Steady state

initval;

y = 0; pi = 0; i = 0; a = 0; eps_m = 0;

end;

steady;

check;

%% Shocks

shocks;

var eta_a; stderr 0.01;

var eta_m; stderr 0.0025;

end;

%% Observables (must match data columns)

varobs y pi i;

%% Estimated parameters with priors

estimated_params;

% Structural

KAPPA, gamma_pdf, 0.1, 0.05;

% Policy rule

PHI_PI, gamma_pdf, 1.5, 0.25;

PHI_Y, gamma_pdf, 0.125, 0.05;

RHO_I, beta_pdf, 0.8, 0.1;

% Shock processes

RHO_A, beta_pdf, 0.9, 0.05;

stderr eta_a, inv_gamma_pdf, 0.01, 2;

stderr eta_m, inv_gamma_pdf, 0.0025, 2;

end;

%% Estimation

estimation(

datafile = 'us_macro_data.csv',

first_obs = 1,

mode_compute = 4, % csminwel optimizer

mode_check, % plot likelihood around mode

mh_replic = 100000, % MH draws

mh_nblocks = 2, % parallel chains

mh_jscale = 0.3, % proposal scaling

mh_drop = 0.5, % burn-in fraction

bayesian_irf, % posterior IRFs

smoother % smoothed states

);Key Estimation Options

| Option | Purpose | Typical Value |

|---|---|---|

mode_compute |

Optimizer for mode | 4 (csminwel) or 9 (dynare default) |

mode_check |

Plot likelihood around mode | Include |

mh_replic |

MH draws | 100,000-500,000 |

mh_nblocks |

Parallel chains | 2-4 |

mh_jscale |

Proposal scaling | 0.2-0.5 (tune for 25% acceptance) |

mh_drop |

Burn-in fraction | 0.5 |

bayesian_irf |

Compute posterior IRFs | Include |

smoother |

Compute smoothed states | Include |

Dynare Output

After estimation, Dynare produces:

| Output | Location | Content |

|---|---|---|

| Posterior mode | oo_.posterior_mode |

Point estimates |

| Posterior draws | oo_.posterior_draws |

MCMC chain |

| Prior/posterior plots | *_PriorPosterior.pdf |

Comparison |

| MCMC diagnostics | *_MCMCdiagnostics.pdf |

Convergence |

| IRFs | oo_.irfs |

Impulse responses |

| Smoothed variables | oo_.SmoothedVariables |

Filtered states |

| Marginal likelihood | oo_.MarginalDensity |

Model comparison |

Model Comparison

Marginal Likelihood

The marginal likelihood (or marginal data density) is:

\[ p(Y | M) = \int p(Y | \theta, M) p(\theta | M) d\theta \]

This integrates over parameter uncertainty, automatically penalizing complexity.

Bayes Factors

Compare models \(M_1\) vs \(M_2\):

\[ BF_{12} = \frac{p(Y | M_1)}{p(Y | M_2)} \]

| \(\log BF_{12}\) | Evidence for \(M_1\) |

|---|---|

| < 0 | Favors \(M_2\) |

| 0-1 | Weak |

| 1-3 | Positive |

| 3-5 | Strong |

| > 5 | Decisive |

Computing Marginal Likelihood

Laplace approximation (fast, less accurate): \[ \log p(Y | M) \approx \log p(Y | \hat{\theta}) + \log p(\hat{\theta}) + \frac{k}{2} \log(2\pi) - \frac{1}{2} \log|H| \]

Modified harmonic mean (Dynare default with MCMC): \[ \hat{p}(Y | M) = \left[\frac{1}{G} \sum_{g=1}^G \frac{f(\theta^{(g)})}{\tilde{p}(\theta^{(g)} | Y)}\right]^{-1} \]

where \(f\) is a truncated Normal centered at the posterior mode.

Log Bayes Factor (correct vs misspecified): 1.58 Interpretation: Positive evidence Diagnostics

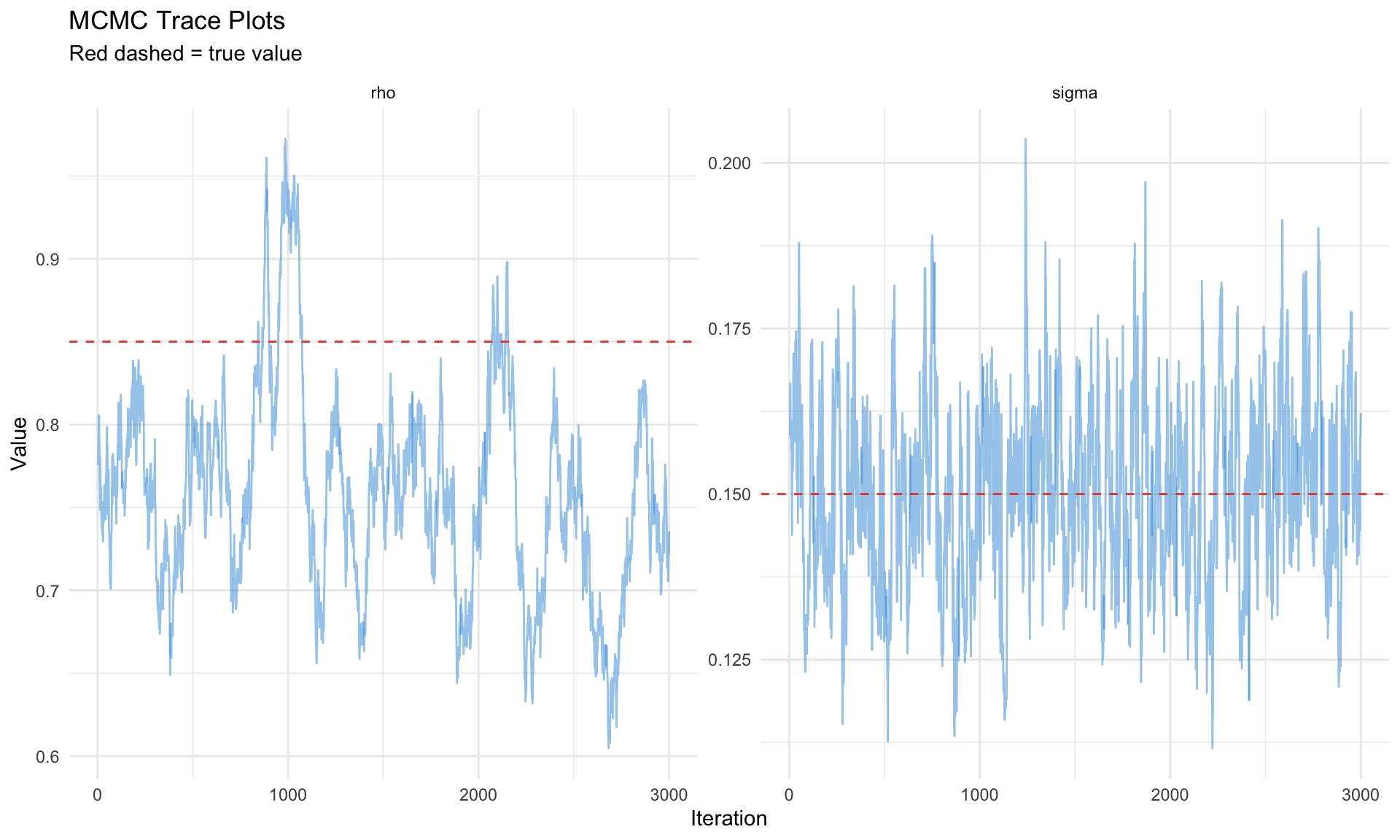

MCMC Convergence

Trace Plots

Chains should: - Explore the full parameter space - Not get stuck in one region - Look like “hairy caterpillars” (good mixing)

Gelman-Rubin Statistic

For multiple chains, compare within-chain vs between-chain variance:

\[ \hat{R} = \sqrt{\frac{\hat{V}(\theta)}{W}} \]

Rule of thumb: \(\hat{R} < 1.1\) (ideally \(< 1.05\))

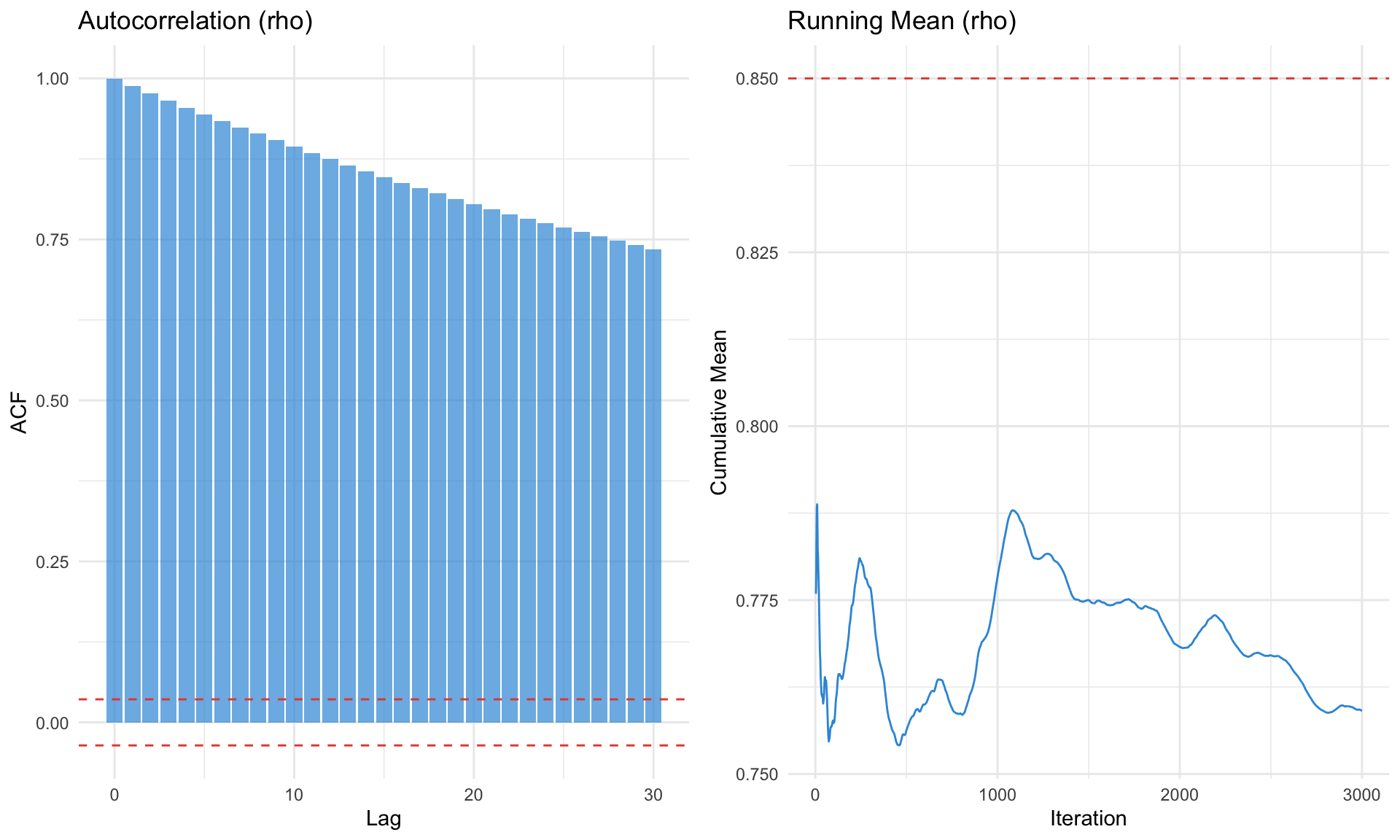

Effective Sample Size

Accounts for autocorrelation in the chain:

\[ \text{ESS} = \frac{n}{1 + 2\sum_{k=1}^\infty \rho_k} \]

Rule of thumb: ESS > 400 for reliable posterior summaries

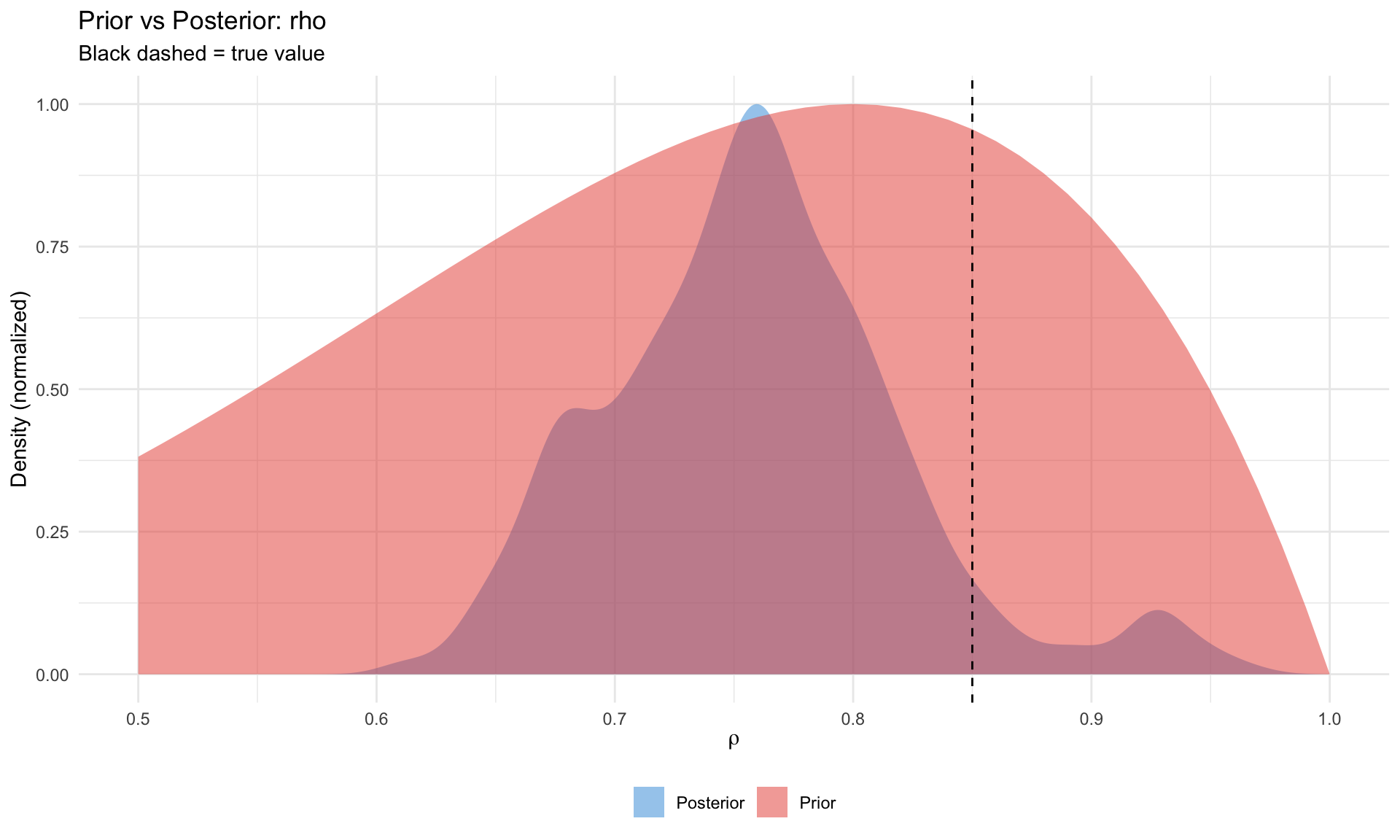

Prior vs Posterior

A key diagnostic: did the data inform the parameter?

| Pattern | Interpretation |

|---|---|

| Posterior ≠ Prior | Data is informative |

| Posterior ≈ Prior | Weak identification or uninformative data |

| Posterior outside prior support | Prior may be misspecified |

Identification

Local identification: Can different \(\theta\) values produce the same observables?

Dynare’s identification command checks: 1. Rank of the Jacobian at the mode 2. Which parameters are weakly identified

Symptoms of weak identification: - Flat likelihood surface - Prior ≈ Posterior - High posterior correlation between parameters

Summary

| Concept | Key Insight |

|---|---|

| State space | DSGE solution → transition + observation equations |

| Kalman filter | Recursive likelihood via prediction + update |

| Maximum likelihood | Point estimate, fast but no uncertainty |

| Bayesian | Full posterior, regularization, model comparison |

| Metropolis-Hastings | Sample from posterior via accept/reject |

| Marginal likelihood | Integrate out parameters for model comparison |

| Diagnostics | Check convergence, identification, prior vs posterior |

TipPractical Workflow

- Start with ML mode to find a good starting point

- Check identification before running full MCMC

- Run short chains first to tune

mh_jscale - Multiple chains for convergence diagnostics

- Compare prior/posterior to assess informativeness

- Model comparison only with converged chains

Key References

Estimation

- An & Schorfheide (2007) “Bayesian Analysis of DSGE Models” Econometric Reviews — Standard reference

- Herbst & Schorfheide (2016) Bayesian Estimation of DSGE Models — Modern textbook

- Del Negro & Schorfheide (2011) “Bayesian Macroeconometrics” Handbook — Survey chapter

Kalman Filter

- Hamilton (1994) Time Series Analysis Ch. 13 — Classic treatment

- Durbin & Koopman (2012) Time Series Analysis by State Space Methods — Comprehensive

MCMC

- Chib & Greenberg (1995) “Understanding the Metropolis-Hastings Algorithm” American Statistician

- Geweke (1999) “Using Simulation Methods for Bayesian Econometric Models” — Practical guide

Model Comparison

- Geweke (1999) “Bayesian Analysis of the Multinomial Probit Model” — Marginal likelihood computation

- Del Negro & Schorfheide (2004) “Priors from General Equilibrium Models for VARs” — DSGE-VAR

Software

- Adjemian et al. “Dynare” — Standard solver/estimator

- Herbst & Schorfheide companion — MATLAB/Python code