Regularization for Macro

LASSO, Ridge, Elastic Net, and High-Dimensional Methods

The High-Dimensional Challenge

Modern macroeconomics faces a dimensionality problem:

- Many potential predictors (hundreds of macro indicators)

- Short time series (T = 50-200 quarters)

- Traditional methods overfit: \(K > T\) makes OLS infeasible

NoteThe Core Trade-off

Bias-variance trade-off: More flexible models fit training data better but may generalize poorly. Regularization adds bias to reduce variance.

When Regularization Matters

| Setting | Problem | Solution |

|---|---|---|

| Large VARs | K variables → K²p parameters | Minnesota prior (shrinkage) |

| Forecasting | Many predictors, short samples | LASSO/Ridge selection |

| Factor models | High-dimensional data | PCA, factor extraction |

| Causal inference | Many potential confounders | Double LASSO |

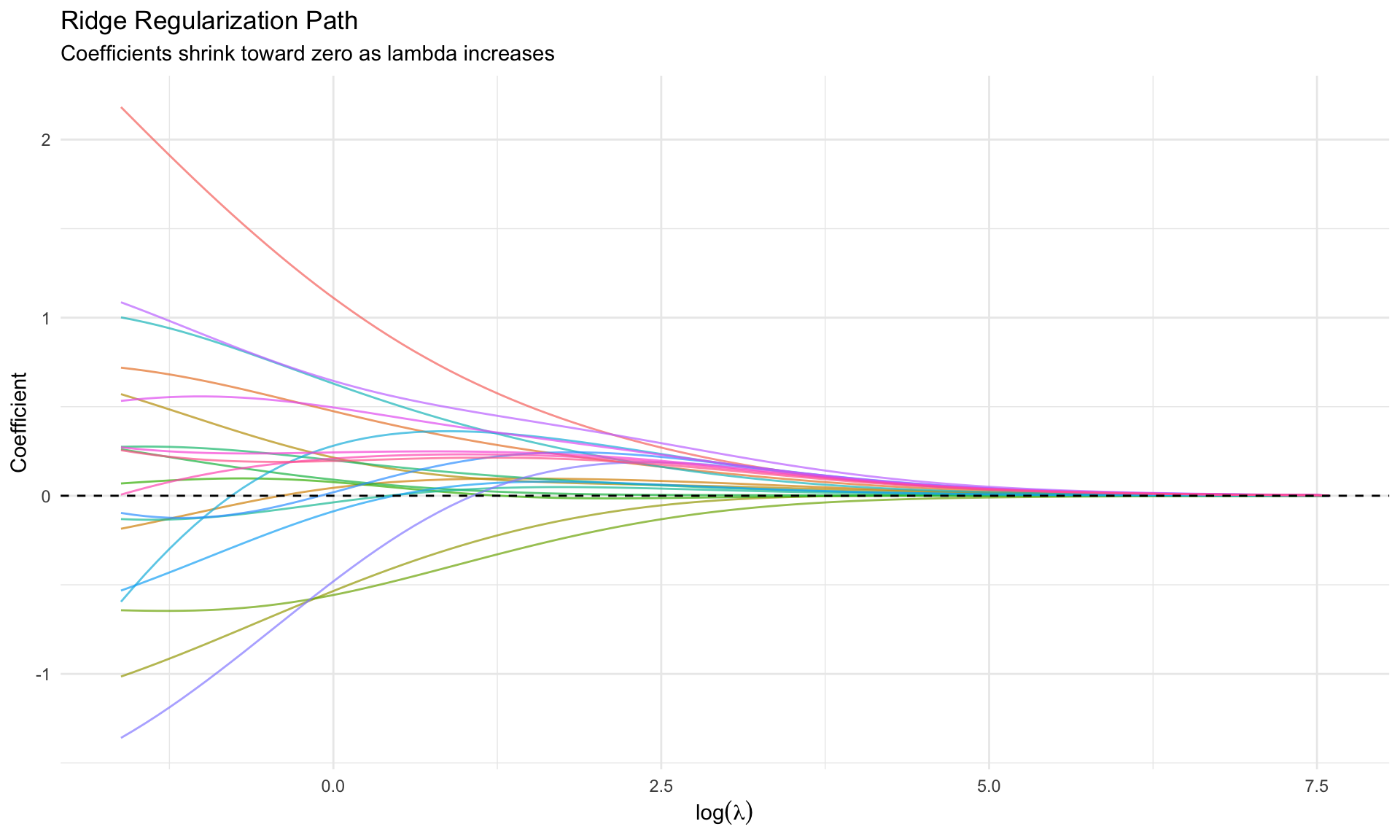

Ridge Regression

The Idea

Add an \(\ell_2\) penalty to prevent coefficients from exploding:

\[ \hat{\beta}^{\text{ridge}} = \arg\min_\beta \left\{ \sum_{i=1}^n (y_i - x_i'\beta)^2 + \lambda \sum_{j=1}^p \beta_j^2 \right\} \]

Equivalently: \[ \hat{\beta}^{\text{ridge}} = (X'X + \lambda I)^{-1} X'y \]

Key Properties

| Property | Implication |

|---|---|

| Shrinks toward zero | All coefficients are shrunk |

| Never exactly zero | Does NOT do variable selection |

| Continuous | Stable, smooth as function of \(\lambda\) |

| Handles multicollinearity | \((X'X + \lambda I)\) always invertible |

Connection to Bayesian Priors

Ridge regression is equivalent to Bayesian regression with: \[ \beta_j \sim N(0, \tau^2), \quad \tau^2 = \frac{\sigma^2}{\lambda} \]

This is exactly the Minnesota prior intuition: shrink toward zero with tightness \(\lambda\).

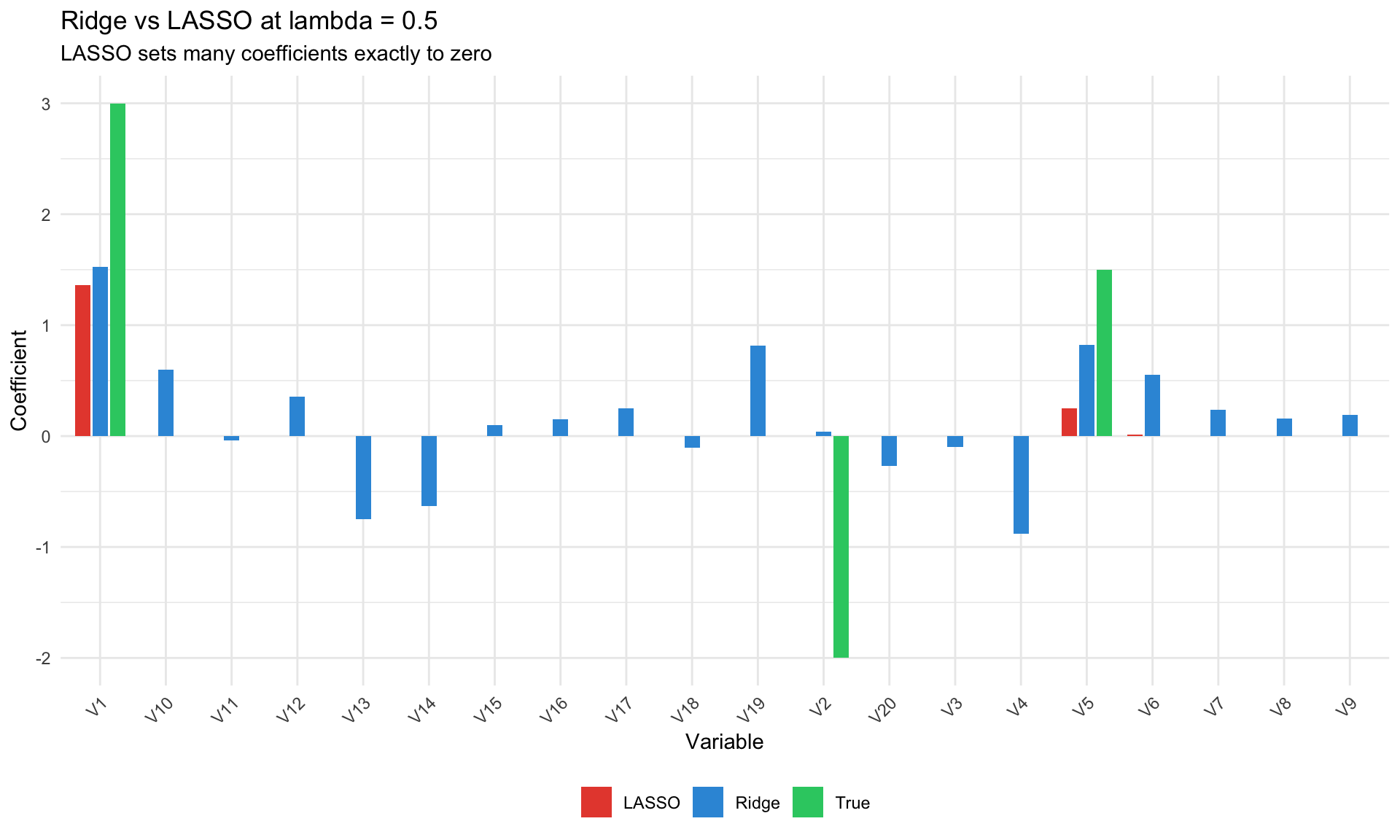

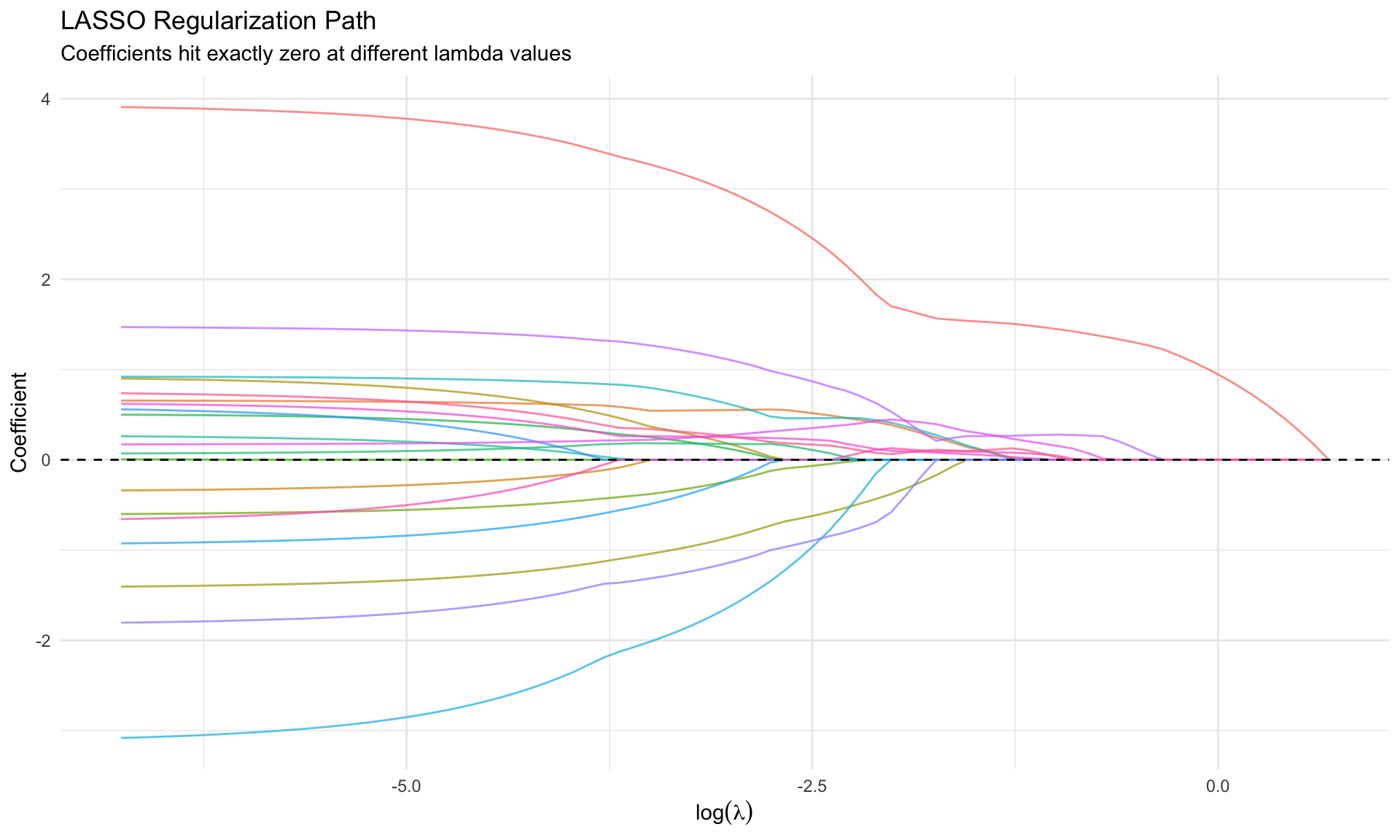

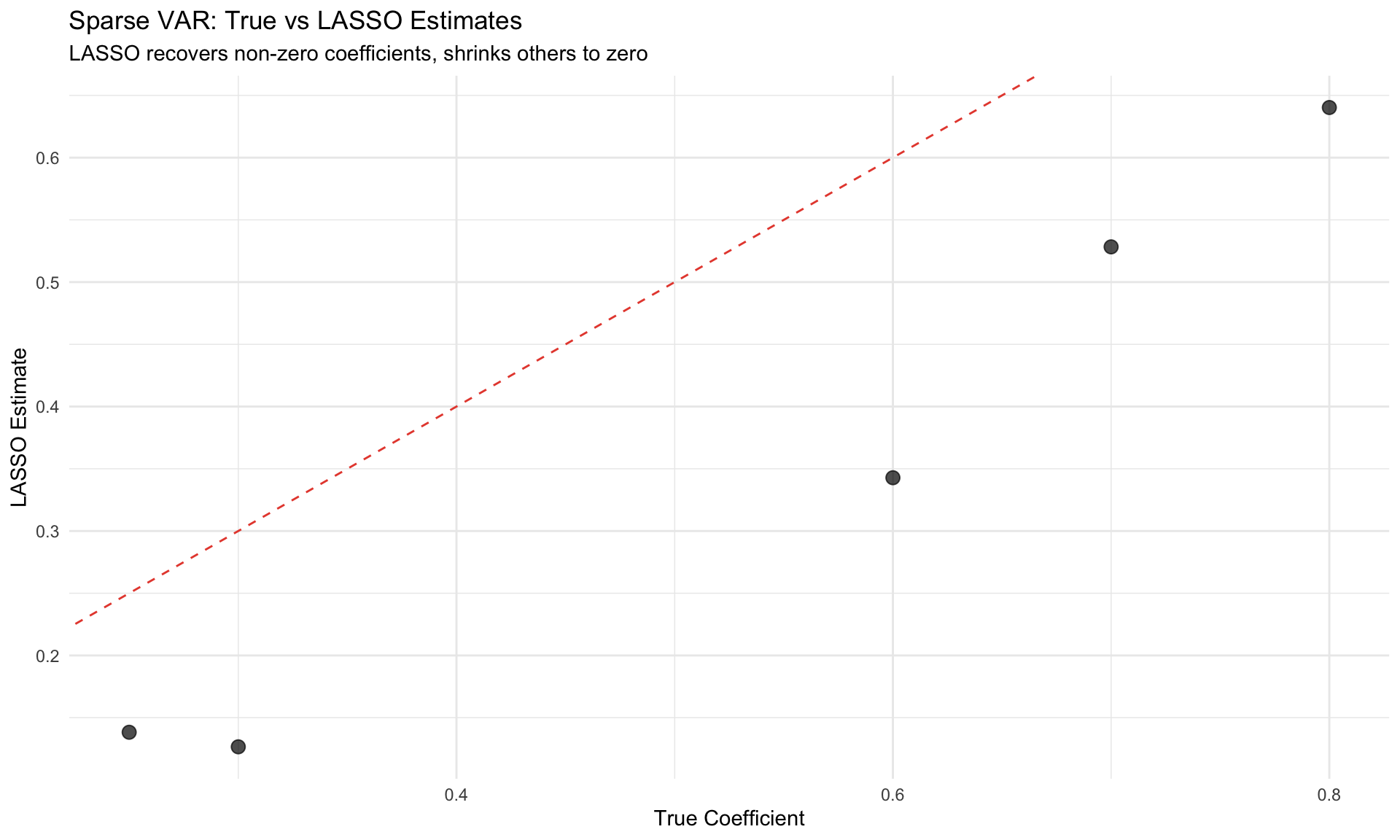

LASSO

The Idea

Replace \(\ell_2\) penalty with \(\ell_1\) (absolute value):

\[ \hat{\beta}^{\text{LASSO}} = \arg\min_\beta \left\{ \sum_{i=1}^n (y_i - x_i'\beta)^2 + \lambda \sum_{j=1}^p |\beta_j| \right\} \]

Key Properties

| Property | Implication |

|---|---|

| Shrinks to exactly zero | Automatic variable selection |

| Sparse solutions | Most coefficients are zero |

| Non-smooth | Path has kinks (not differentiable) |

| Selects one from correlated group | Arbitrary among correlated predictors |

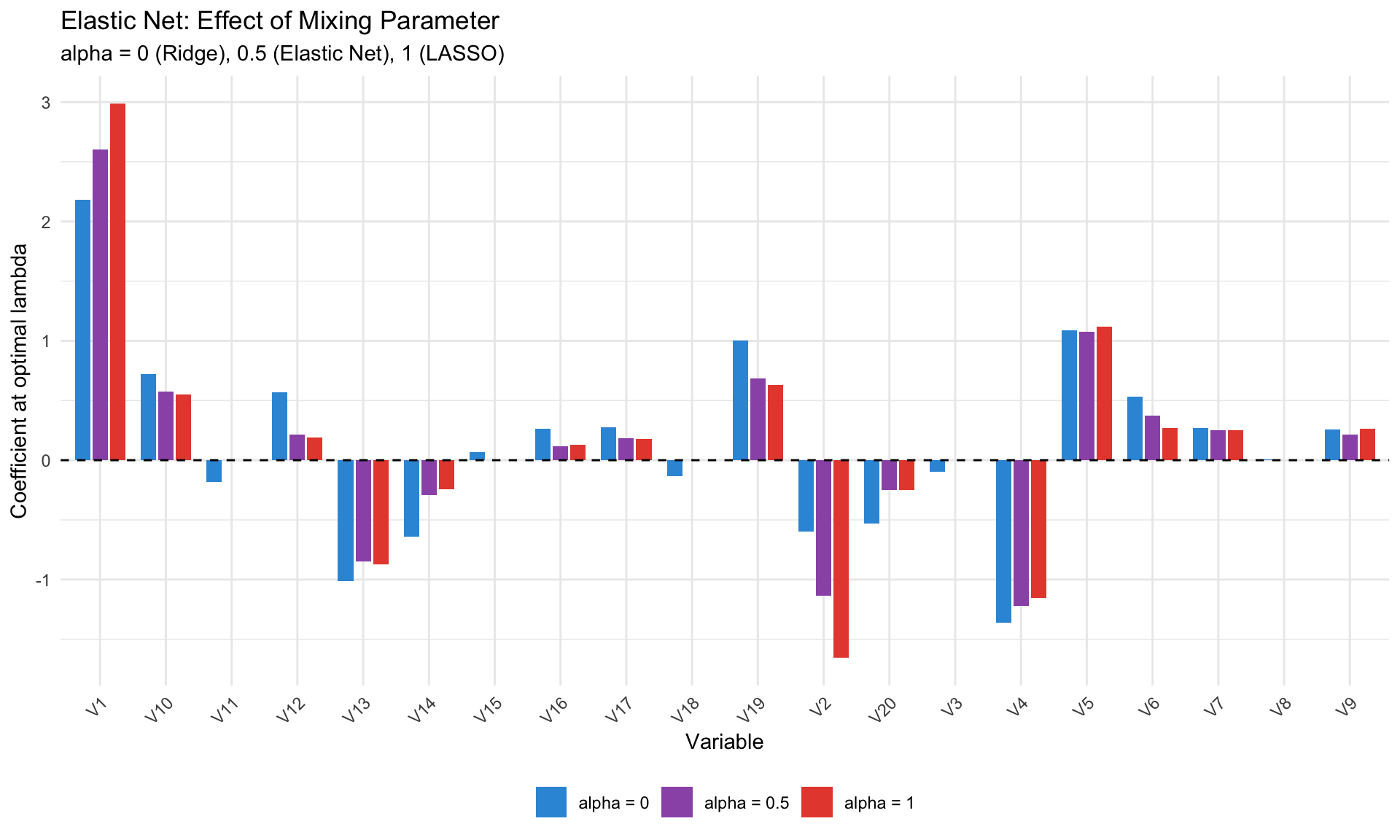

Elastic Net

Combining Ridge and LASSO

\[ \hat{\beta}^{\text{EN}} = \arg\min_\beta \left\{ \sum_{i=1}^n (y_i - x_i'\beta)^2 + \lambda \left[ \alpha \sum_j |\beta_j| + (1-\alpha) \sum_j \beta_j^2 \right] \right\} \]

| \(\alpha\) | Method |

|---|---|

| 0 | Ridge |

| 1 | LASSO |

| 0.5 | Elastic Net (balanced) |

When to Use Elastic Net

- Correlated predictors: LASSO arbitrarily selects one; Elastic Net keeps groups together

- \(p > n\): LASSO selects at most \(n\) variables; Elastic Net can select more

- Default in practice: Often use \(\alpha = 0.5\) as a robust choice

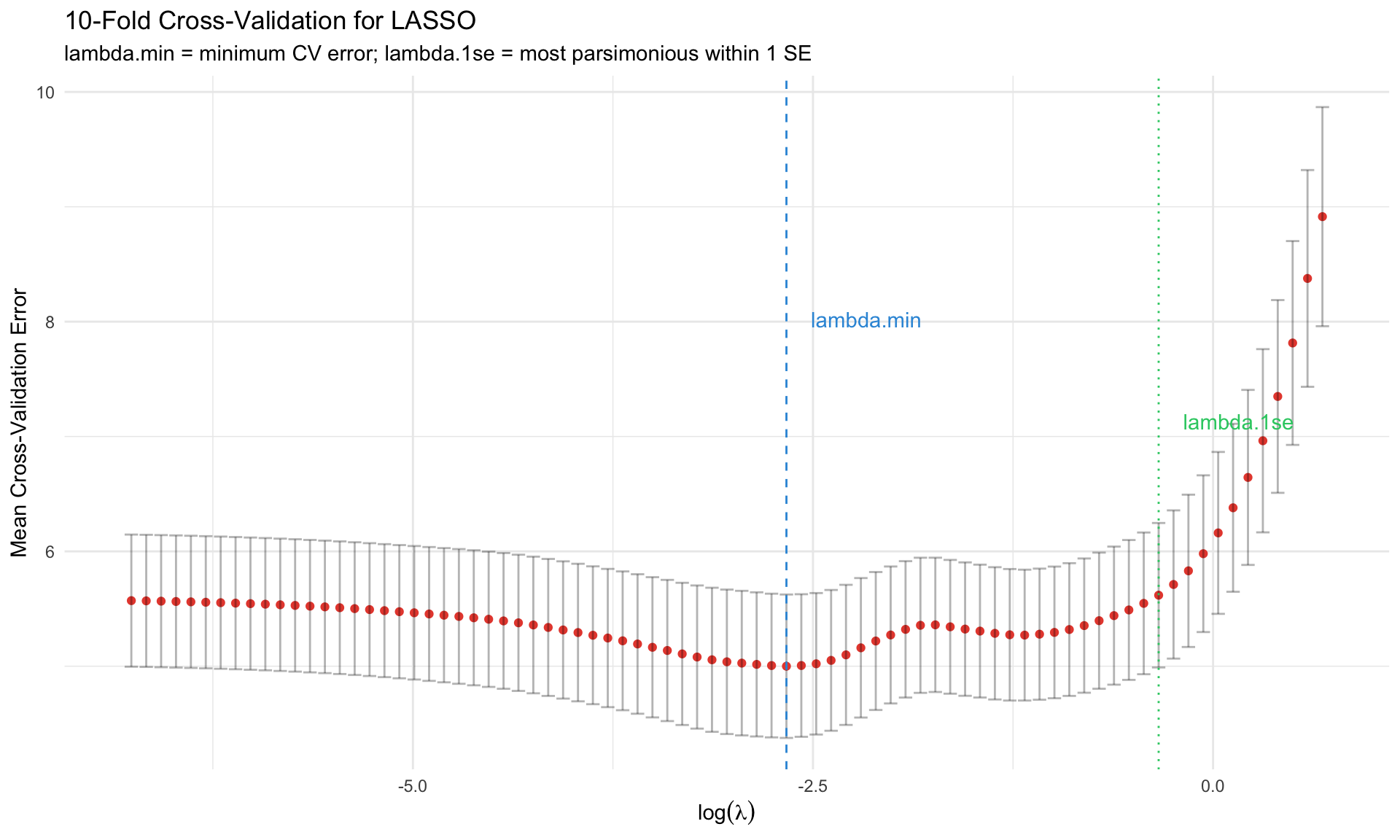

Choosing Lambda: Cross-Validation

K-Fold Cross-Validation

- Split data into K folds

- For each \(\lambda\):

- Train on K-1 folds, predict on held-out fold

- Repeat K times

- Average prediction error

- Choose \(\lambda\) that minimizes CV error

lambda.min vs lambda.1se

| Choice | Description | When to Use |

|---|---|---|

lambda.min |

Minimizes CV error | Maximum predictive power |

lambda.1se |

Largest \(\lambda\) within 1 SE of min | More parsimonious, often preferred |

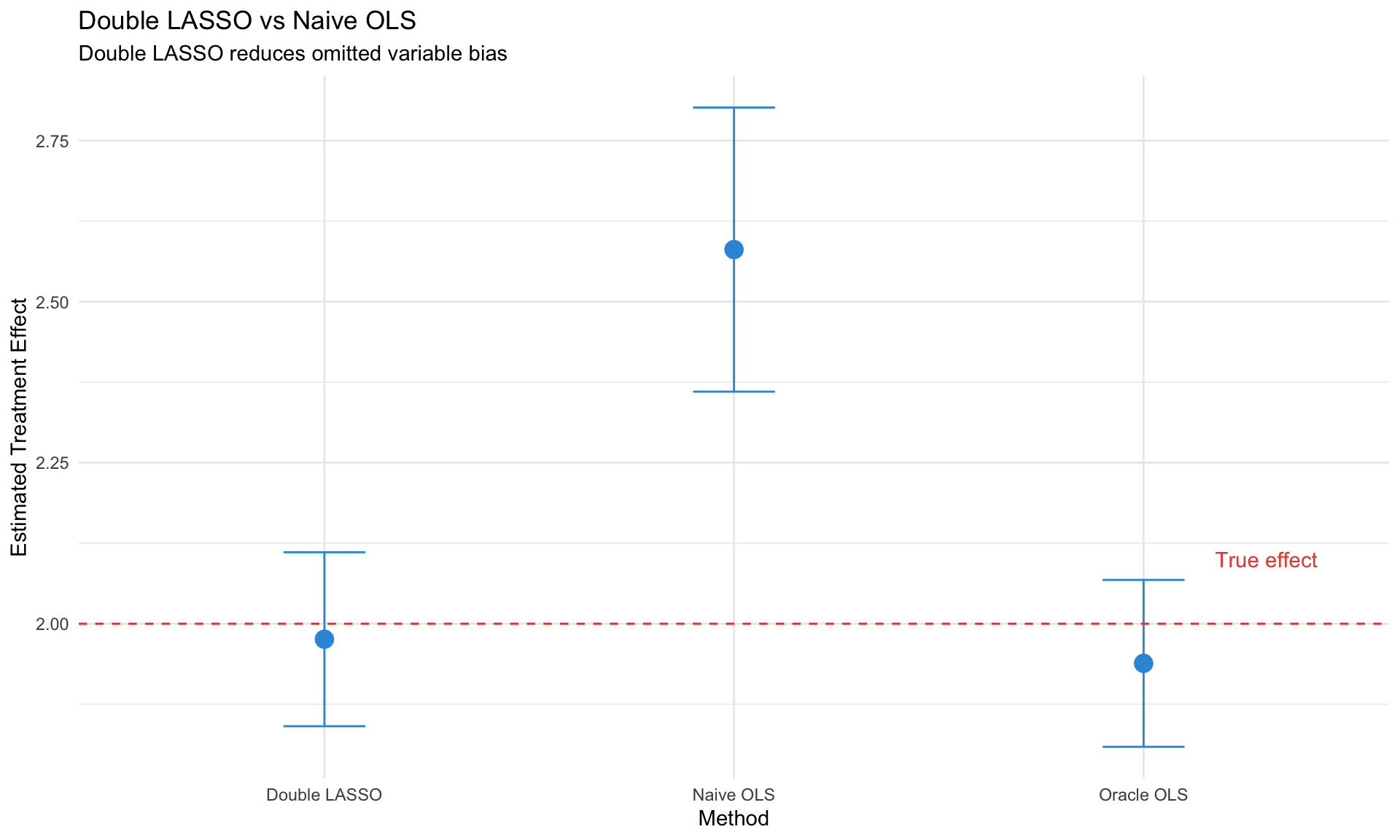

Double/Debiased LASSO

The Problem with Naive LASSO for Inference

LASSO gives biased estimates and invalid standard errors because:

- Regularization bias: Shrinkage toward zero

- Model selection uncertainty: Which variables are “truly” zero?

- No valid confidence intervals in the classical sense

The Solution: Double Selection

For causal effect of \(D\) on \(Y\) with high-dimensional controls \(X\):

Step 1: LASSO of \(Y\) on \(X\) → select controls \(\hat{S}_Y\)

Step 2: LASSO of \(D\) on \(X\) → select controls \(\hat{S}_D\)

Step 3: OLS of \(Y\) on \(D\) and \(\hat{S}_Y \cup \hat{S}_D\)

This is the Belloni, Chernozhukov, Hansen (2014) approach.

Naive OLS (biased): 2.581 Double LASSO: 1.976 True effect: 2 Selected variables: 4

The hdm Package in R

library(hdm)

# Double selection

ds_result <- rlassoEffect(x = X, y = Y, d = D, method = "double selection")

summary(ds_result)

# Partialling out

po_result <- rlassoEffect(x = X, y = Y, d = D, method = "partialling out")

summary(po_result)Applications in Macro

Large Bayesian VARs (Banbura, Giannone, Reichlin 2010)

Problem: K-variable VAR(p) has \(K^2 p\) parameters.

Solution: Tighter Minnesota prior as dimension grows

\[ \lambda_1^{\text{large}} = \lambda_1^{\text{small}} \times \frac{K_{\text{small}}}{K_{\text{large}}} \]

This is implicit Ridge regularization.

Factor-Augmented VAR (FAVAR)

Extract factors from large dataset, include in VAR:

\[ \begin{pmatrix} F_t \\ Y_t \end{pmatrix} = A \begin{pmatrix} F_{t-1} \\ Y_{t-1} \end{pmatrix} + u_t \]

where \(F_t\) are principal components of hundreds of macro series.

Sparse Granger Causality

Use LASSO to identify which variables Granger-cause others in high-dimensional settings.

Practical Implementation

The glmnet Workflow

library(glmnet)

# Standardize predictors (glmnet does this internally)

X <- scale(X)

# Ridge (alpha = 0)

ridge_fit <- glmnet(X, y, alpha = 0)

cv_ridge <- cv.glmnet(X, y, alpha = 0)

coef(cv_ridge, s = "lambda.min")

# LASSO (alpha = 1)

lasso_fit <- glmnet(X, y, alpha = 1)

cv_lasso <- cv.glmnet(X, y, alpha = 1)

coef(cv_lasso, s = "lambda.1se")

# Elastic Net (alpha = 0.5)

en_fit <- glmnet(X, y, alpha = 0.5)

cv_en <- cv.glmnet(X, y, alpha = 0.5)

# Predictions

predict(cv_lasso, newx = X_new, s = "lambda.min")Choosing Alpha

Use nested cross-validation:

# Grid search over alpha

alpha_grid <- seq(0, 1, 0.1)

cv_errors <- sapply(alpha_grid, function(a) {

cv_fit <- cv.glmnet(X, y, alpha = a)

min(cv_fit$cvm)

})

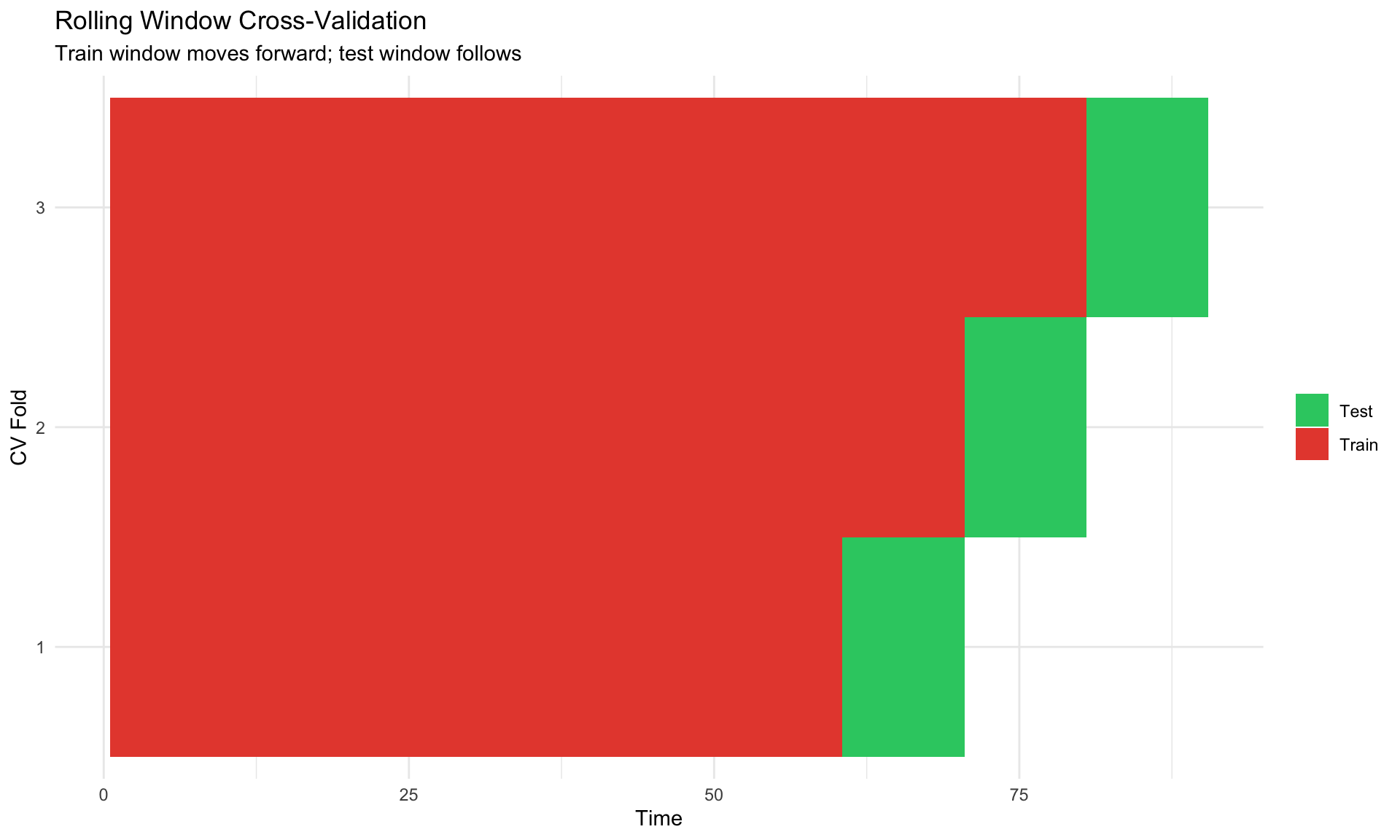

best_alpha <- alpha_grid[which.min(cv_errors)]Time Series Considerations

Standard CV is problematic for time series (breaks temporal structure).

Solutions:

- Rolling window CV: Train on \(t=1,\ldots,s\), test on \(s+1,\ldots,s+h\)

- Expanding window CV: Train on \(t=1,\ldots,s\), test on \(s+1\), then expand

- Block bootstrap: Resample blocks to preserve autocorrelation

Common Pitfalls

WarningWatch Out For

- Post-selection inference: Don’t report OLS standard errors after LASSO selection

- Standardization: Always standardize predictors for fair penalization

- Time series CV: Don’t use random splits for time series

- Interpretation: LASSO coefficients are shrunken—not the “true” effects

- Correlated predictors: LASSO picks arbitrarily; consider Elastic Net

- Oracle property: LASSO is consistent under stringent conditions (irrepresentable condition)

Summary

| Method | Penalty | Selection | When to Use |

|---|---|---|---|

| Ridge | \(\ell_2\) | No | Multicollinearity, all predictors matter |

| LASSO | \(\ell_1\) | Yes | Sparse truth, variable selection |

| Elastic Net | Both | Yes | Correlated predictors, \(p > n\) |

| Double LASSO | \(\ell_1\) | Yes | Causal inference with many controls |

TipFor Macro Applications

- Forecasting: LASSO/Ridge with rolling CV

- Large VARs: Minnesota prior (implicit Ridge)

- Causal inference: Double LASSO for high-dimensional controls

- Model selection: Elastic Net as robust default

Key References

Regularization Methods

- Tibshirani (1996) “Regression Shrinkage and Selection via the Lasso” JRSS-B

- Zou & Hastie (2005) “Regularization and Variable Selection via the Elastic Net” JRSS-B

- Hastie, Tibshirani & Wainwright (2015) Statistical Learning with Sparsity — Comprehensive textbook

High-Dimensional Inference

- Belloni, Chernozhukov & Hansen (2014) “Inference on Treatment Effects after Selection” RES — Double LASSO

- Chernozhukov et al. (2018) “Double/Debiased Machine Learning” Econometrics Journal

- Athey & Imbens (2019) “Machine Learning Methods That Economists Should Know About” Annual Review

Macro Applications

- Banbura, Giannone & Reichlin (2010) “Large Bayesian VARs” JAE

- Stock & Watson (2012) “Generalized Shrinkage Methods for Forecasting” JAE

- Giannone, Lenza & Primiceri (2021) “Economic Predictions with Big Data” JAE

Software

- glmnet: Friedman, Hastie & Tibshirani — R package for penalized regression

- hdm: Chernozhukov et al. — High-dimensional metrics in R